Photo:Bing AI

August 3, 2023

- Bank of England hikes rates 25 bps to 5.25%.

- BoJ intervenes in bond market.

- USD dollar extends gains due to risk aversion demand for dollars.

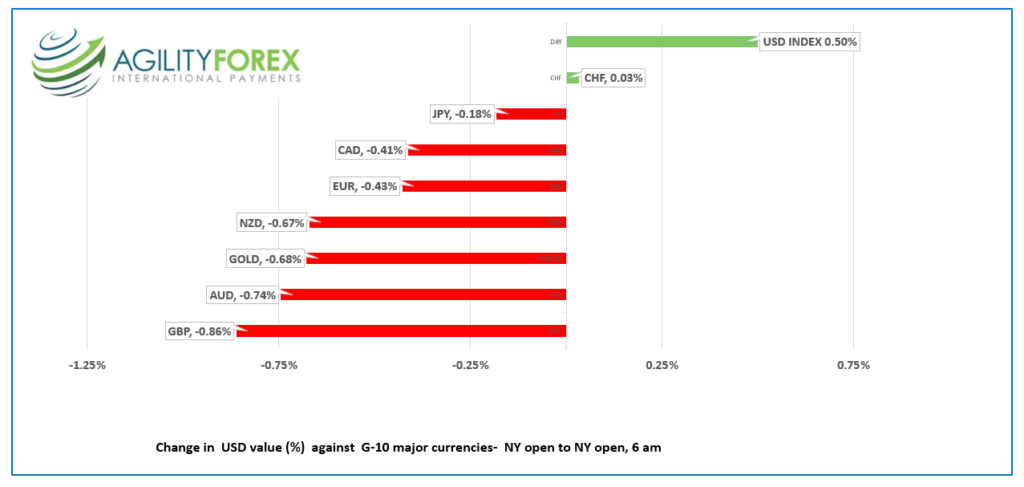

FX at a Glance

Source: IFXA/RP

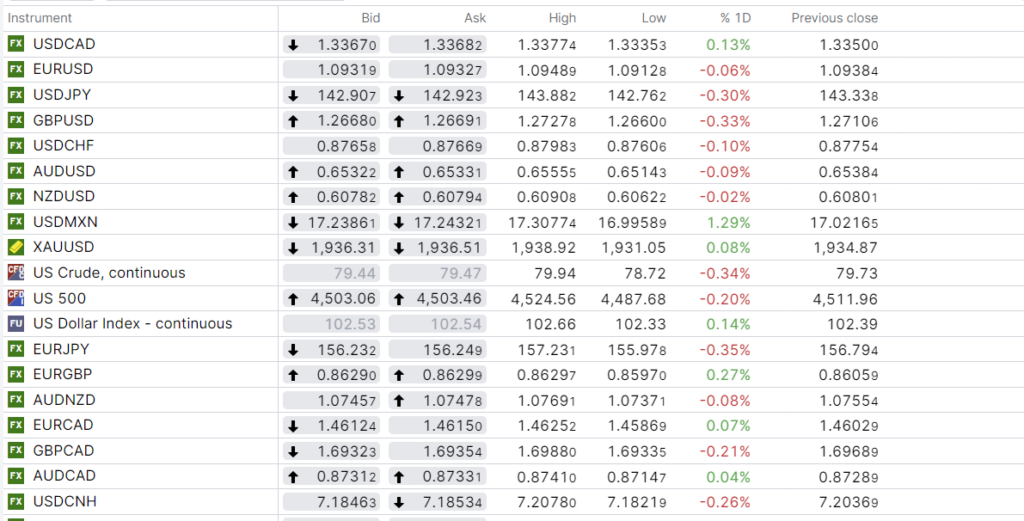

USDCAD Snapshot: open: 1.3366-70, overnight range 1.3335-1.3377, close 1.3350

USDCAD rallied further overnight due as risk aversion stemming from the Fitch downgrade of US debt, continued to ripple through markets. What happens in the US does not stay in the US.

USDCAD is also supported by the widening CAD/US interest rate differential, in favour of the US and by steady to firm WTI oil prices which are hovering around the $80.00/b level.

Even so, USDCAD direction is a US dollar story of rising Treasury yields and robust economic data.

Traders are looking ahead to tomorrows Canadian employment report which is expected to show Canada gained 21,100 jobs in July.

USDCAD Technicals

The intraday USDCAD technicals are bullish. The latest rally has taken out key resistance levels at 1.3260 and again at 1.3330, with a break above 1.3390, setting the stage for a test of the March downtrend line which comes into play at 1.3470.

Failure to break above 1.3390 and a subsequent drop below 1.3330 will extend losses to 1.3260 and suggest a short term top is in place.

For today, USDCAD support is at 1.3330 and 1.3260 Resistance is at 1.3390 and 1.3450. Today’s range 1.3310-1.3410

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

The Fitch downgrade of US debt continues to have reverberations, even though many on Wall Street downplay the action. JPMorgan Chase Chairman Jamie Dimon finds the idea of the US being rated lower than countries like Germany, Sweden, and Denmark “ridiculous,” attributing their stability to the USA and its military. Meanwhile, Goldman Sachs analysts dismiss the downgrade, stating it doesn’t offer any new information.

Traders appear to disagree. They bought US dollars and sold stocks and bonds. The Australian dollar is the worst performing G-10 currency, losing 1.73% since Tuesday’s NY open, while the Japanese yen is the best performer, as it only lost 0.15%. The S&P 500 closed at 4588.96 on Monday and 4513.39 on Wednesday for a loss of 1.16%. The US 10-year Treasury yield closed Monday at 3.969% and it is 4.147% today.

The price action may be because traders think it is a sign of things to come, or it may just be an over-reaction in a thin summer market ahead of key US employment data on Friday. Once again, the stronger than expected ADP jobs data has traders thinking Friday’s NFP may see a similar result.

Asian equity markets were busy. The Japanese Nikkei 225 index fell 1.68%, despite the weaker yen, while Australia’s ASX 200 lost 0.50%. European bourses opened negatively and the 2.18% loss in the French CAC is leading the rest lower. S&P 500 futures are down 0.36%, while gold and WTI prices are lower.

EURUSD traded in a 1.0913-1.0949 range overnight and is trading near the top of that band in NY. Nevertheless, the single currency has lost more than half of the gains that occurred between June 1 and July 17, and the short-term technicals are bearish while prices are below 1.0990. The ongoing Fitch-inspired turmoil overshadowed Eurozone data, which included Services PMI (actual, fo.9 vs forecast 51.1).

GBPUSD traded with a negative bias in a 1.2671-1.2728 band then tumbled to 1.2625 in the after math of the Bank of England decision. The BoE raised its benchmark rate to 5.25% but the decision was far from unanimous. Six member voted to hike, three members wanted to leave rates unchanged and two members wanted to hike rates by 50 bps. The BoE wants to ensure that rates are restrictive enough to ensure inflation keeps falling.

USDJPY rallied to 143.88 in Asia, then crashed to 142.77 in Europe, just before NY opened. The Bank of Japan intervened in the bond market to cap the latest rise in JGB yields, by offering to buy an “unlimited” amount of 5 and 10-year bonds.

AUDUSD is trading close to the bottom of its 0.6514-0.6556 range with selling pressure due to broad US dollar demand. AUDUSD support from the news that Australia’s trade surplus widened was offset by data showing Retail Sales fell 0.5% q/q in Q2 and Services PMI ticked down to 47.9 from 48.

Today’s US data includes initial jobless claims, ISM Services PMI, and factory orders.

FX high, low, previous close

China Snapshot

Bank of China Fix: 7.1495 , forecast 7.1933, previous 7.1368.

Shanghai Shenzhen CSI 300 rose 0.88% to 4004.98.

Some analysts are predicting that the PboC may cut the reserve requirement ratio (RRR) this month.

Caixin July Services PMI (actual 54.1, forecast 52.5, June 53.9) The Caixin data shows Services PMI exceeding expectations, while Monday’s NBS Services official services data was lower than the June result. The Survey noted that the results pointed to an expansion oof business activity across the service economy for the seventh straight month, although it was softer than seen in the first half of the year.

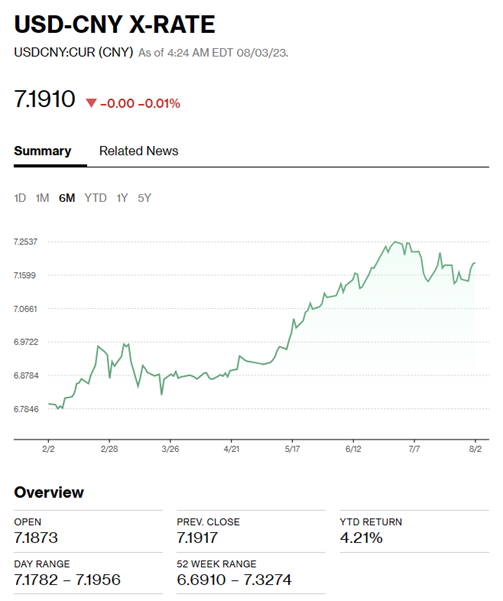

Chart: USDCNY 6 month

Source: Bloomberg