Photo: Bing AI

September 21, 2023

- Norges bank and Riksbank hike, SNB pauses.

- Bank of England leaves rates unchanged.

- US dollar crushes everything in its path.

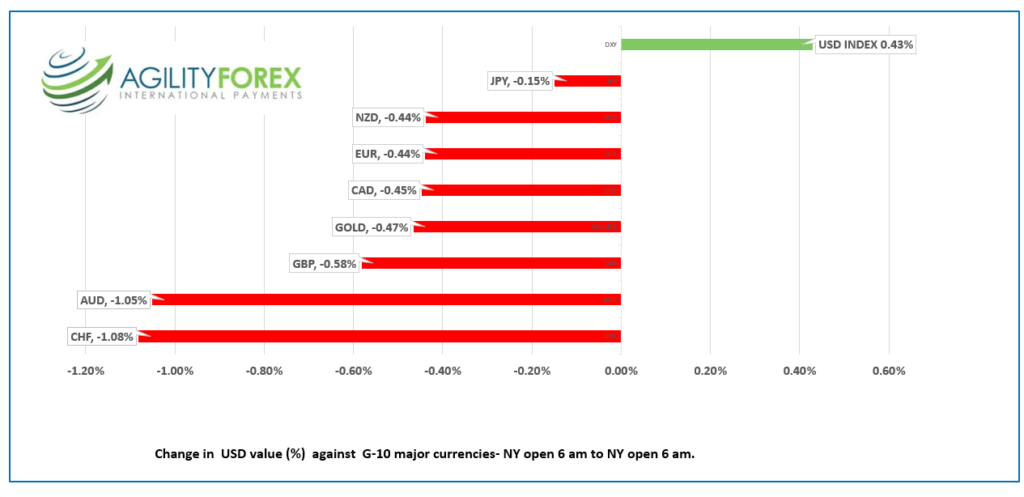

FX at a Glance

Source: IFXA/RP

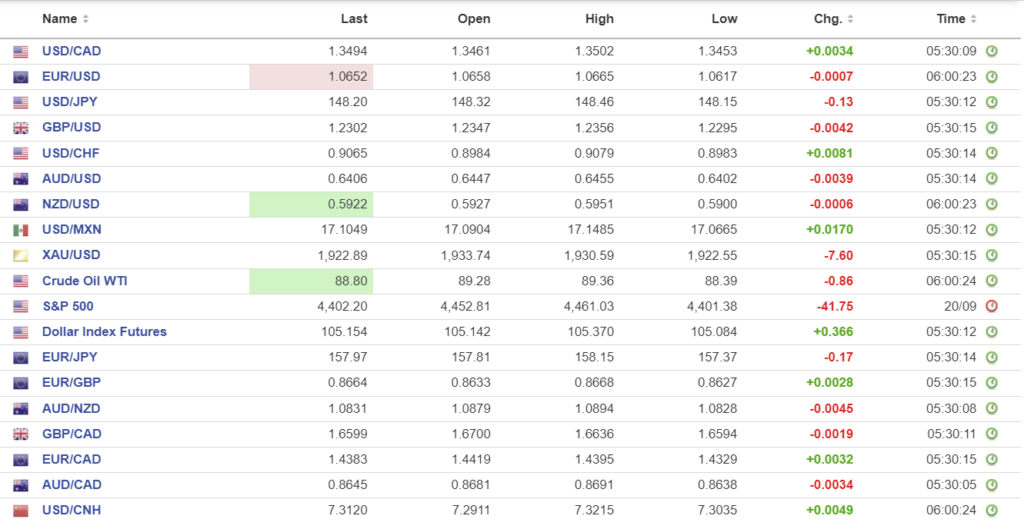

USDCAD Snapshot: open: 1.3492-96, overnight range: 1.3453-1.3520, close 1.3461.

USDCAD rallied due to broad-based US dollar demand after a more-hawkish-than-expected FOMC decision yesterday. The prospect of higher US rates for longer has traders forgetting Tuesday’s hot inflation data which suggested the Bank of Canada would hike rates in October.

The widening of the 10-year CAD/US interest yield differential in favour of the US is underpinning prices as is the drop in WTI oil prices below $90.00/b.

Canada Retail Sales data is due on Friday, but it will likely have minimal impact on USDCAD trading as the focus is entirely on the US interest rate outlook.

USDCAD Technicals

USDCAD turned bullish with yesterday’s break above resistance at 1.3440 and again at 1.3490. The latter move broke the downtrend from September 8 and further gains above 1.3550 will target 1.3660.

The RSI studies turned higher and suggest a neutral bias.

For today, USDCAD support is at 1.3480 and 1.3460. Resistance is at 1.3550 and 1.3590. Today’s range 1.3480-1.3550

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The greenback juggernaut is looking unstoppable as it rolls over the major G-10 currencies in the aftermath of hawkish central bank rate activity.

Yesterday, the Fed left rates unchanged at 5.5%, upgraded economic growth, lowered its unemployment forecasts, and the dot-plot projected higher rates for longer. The more hawkish-than-expected outcome boosted the US dollar and knocked Wall Street lower.

That theme continued overnight and was underscored in Europe after Sweden’s Riksbank and Norway’s Norges Bank raised benchmark rates by 25 bps. The Norges Bank was the more hawkish of the two as it signaled another 25 bp hike is likely in December, while analysts suggest the odds for another Riksbank hike are about 50/50.

The Swiss National Bank surprised markets when it left its benchmark rate unchanged at 1.75%. SNB Chairman Thomas Jordan said an overvalued franc contributed to low inflation. The rate decision lifted USDCHF from 0.8983 to 0.9079.

Turkey President Recep Erdogan may have attended the same economics class as Justin Trudeau. The latter famously told reporters that he did not think about monetary policy as he racked up massive government debt. Mr. Erdogan boldly challenged the global consensus among economists, rejecting the idea that raising interest rates was the key to reducing inflation. However, the staggering 172% decline in the Turkish Lira’s value since last September appears to have prompted Erdogan to reconsider his stance. Reports suggest that he is now endorsing a 500 basis point rate hike by the Turkish central bank today.

Asian equity indexes finished deep in the red. Japan’s Nikkei 225 index fell 1.37%, while Australia’s ASX 200 lost 1.37%. European bourses opened in negative territory, and a 1.50% drop in the French CAC 40 index is leading the pack lower. S&P 500 futures are down 0.64%. The US 10-year Treasury yield surged from 4.347% at yesterday’s close to 4.431% in NY today.

The Fed’s hawkish outlook received mixed justification this morning. Weekly jobless claims fell by 20,000 to 201,000 while the Philadelphia Manufacturing Survey showed activity in the area declined. The key diffusion index returned to negative territory falling from 12.0 in August to -13.5 in September.

EURUSD is looking for direction in a 1.0617-1.0665 range, with prices weighed down by the hawkish FOMC outcome. ECB officials have been jawboning that interest rates need to remain restrictive for some time.

GBPUSD plunged from an overnight peak of 1.2356 to 1.2243 after the Bank of England disappointed half of the market by leaving its overnight rate unchanged at 5.25%. The decision was not unanimous. The debate as to whether this is the peak for UK rates has already started.

USDJPY traders are nervous. The currency pair climbed to 148.46 in early Asia then retreated to 147.74 in NY on fear of Bank of Japan intervention, although the downside was supported by the spike in the US 10-year Treasury yield.

AUDUSD traded negatively in a 0.6401-0.6455 range due to broad US dollar demand following the FOMC decision.

NZDUSD outperformed its Aussie cousin while trading in a 0.5900-0.5951 range, with prices supported by higher than expected Q2 GDP (actual 0.9% q/q vs. forecast 0.2%).

FX high, low, open

Source: Investing.com

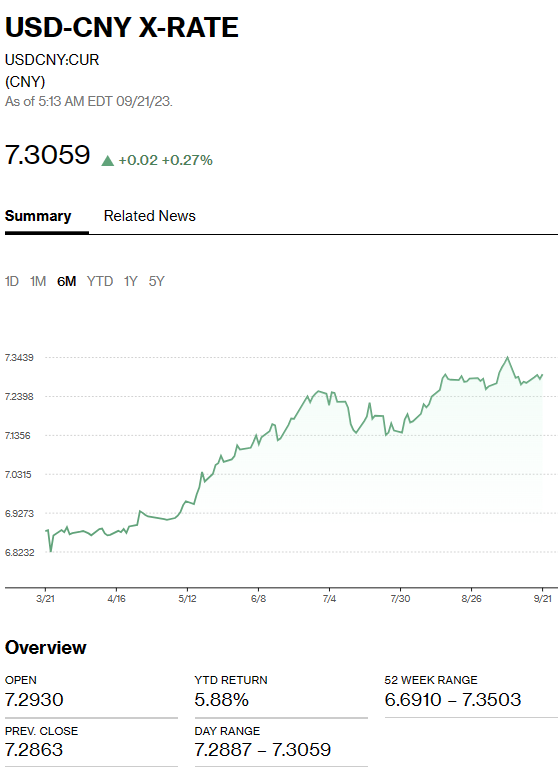

China Snapshot

Bank of China Fix: today 7.1730, expected 7.3052, previous 7.1732

Shanghai Shenzhen CSI 300 fell 0.40% to 3705.69.

PboC economist Zhou Xiaochuan said they will pay more attention to yuan changes vs a basket of currencies and will resolutely correct one-side behaviour in the exchange rate.

Chart: USDCNY 1 month

Source: Bloomberg