Photo: CNN/IFXA

February 7, 2023

- Jerome Powell’s post-NFP speech at 9:40 am PT

- Hawkish RBA hikes 25 bps as expected.

- US dollar falls from best levels, AUD outperforms.

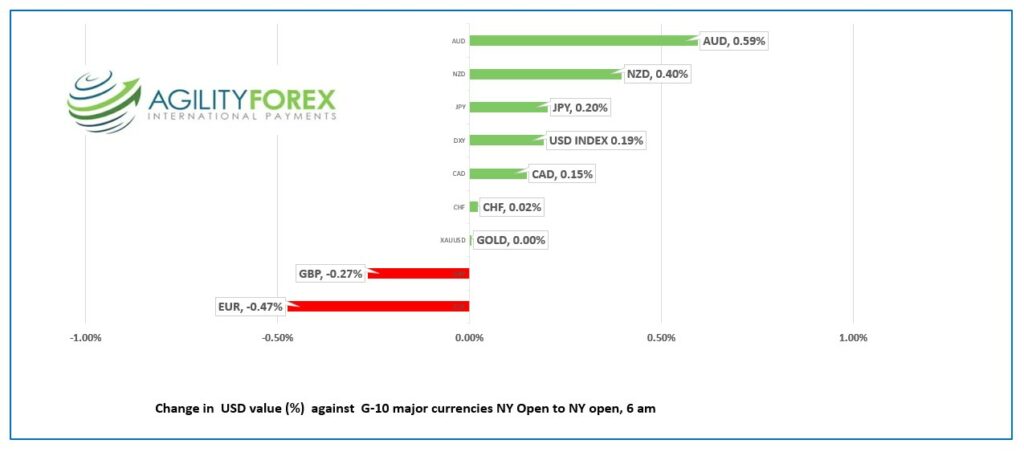

FX at a glance

Source: IFXA Ltd/RP

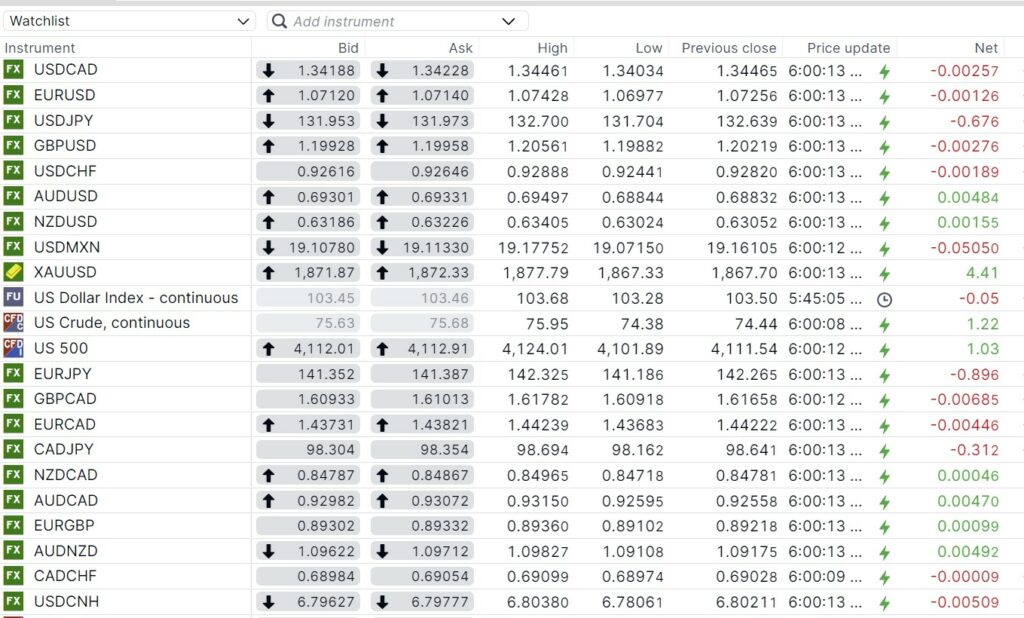

USDCAD Snapshot: open 1.3419-23, overnight range 1.3403-1.3450, close 1.3447

USDDCAD failed to break above downtrend resistance yesterday and overnight. The debate is whether Fed Powell’s comments today will be enough to take out the top, or if Bank of Canada Governor Tiff Macklem’s comments will help limit USDCAD gains. Traders are not sure if Mr Macklem is a data-dependent dove or hawk or if his message will change in light of the US employment data.

Oil prices remain in their week-long downtrend. WTI dropped from $82.16/b on January 27 to $72.23 yesterday before getting a boost after the earthquake in Turkey closed a major oil terminal. Prices are also underpinned by a report that Saudi Aramco raised the price for its Arab Light grade for Asian clients.

Canada’s trade balance was a 0.16 billion deficit in December, which was better than the $1.0 billion deficit expected.

USDCAD Technical Outlook

The intraday USDCAD technicals are modestly bullish, with the uptrend from February 2 intact while trading above the 1.3400-05 on an hourly chart.

Longer term, the uptrend line from August 17 is intact above 1.3260, while the downtrend line from mid-October sits at 1.3570. A break either side of those levels suggests a 0.0200-point move.

For today, USDCAD support is at 1.3380 and 1.3340. Resistance is at 1.3460 and 1.3490

Today’s range 1.3390-1.3460

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Traders are treading carefully ahead of Fed Chair Jerome Powell’s speech at the Economic Club of Washington. Mr Powell is expected to reiterate his hawkish comments from the post FOMC press conference, in the wake of the hotter than hot nonfarm payrolls report. He won’t jump up and down shouting “I told you so” but it will be implied.

Minneapolis Fed President and FOMC voter Neal Kashkari said the Fed has not made enough progress on inflation and is sticking with his rate outlook. This morning he said ““We need to raise rates aggressively to put a ceiling on inflation, then let monetary policy work its way through the economy.”

The annual Congress Calisthenics ball is tonight. That’s when President Biden delivers the annual State of the Union address tonight and Democrats rise to clap, sit, then do it all again for the entirety of Biden’s remarks.

Asian equity indexes closed on a mixed note. China’s CSI 300 index and Hong Kong’s Hang Seng Index posted gains while Japan’s Nikkei 225 and Australia’s ASX 200 indexes were flat to down.

European bourses are trading close to flat except the UK FTSE 100 index which is 0.67% higher. S&P 500 futures are also unchanged. The US 10-year Treasury yield is steady at 3.642%.

EURUSD traded in a 1.06878-1.0743 range with the low seen in early NY. Traders are more worried about hawkish remarks from Mr Powell this morning which is hawkish statements from ECB officials earlier. EURUSD is also weighed down by soft German Industrial Production data which fell 3.1% m/m and 3.9% y/y in December. ING economists said, “This is a simply horrible report.”

GBPUSD fell to 1.1963 in NY after peaking at 1.2056 range in Asia. Traders ignored better than expected January Halifax House Price Index data (actual 1.9% y/y 3m, forecast 0.3% decline) and worried about the tone of Mr Powell’s upcoming speech.

USDJPY traded in a 131.70-132.70 range and sits at 132.00 in NY. Sharply higher December Labour Cash Earnings data (actual 4.8% y/y, forecast for a 0.9% y/y) and talk about the appointment of another dovish BoJ governor more than offset the impact of the US 10-year Treasury yield at 3.653%.

AUDUSD got a boost from a hawkish RBA result, which lifted AUDUSD from 0.6884 to 0.6950, before prices retreated to 0.6905 in NY. As widely expected, the RBA hiked rates 25 bps to 3.35%. The statement was hawkish and suggested rates would continue to move higher, with one analyst now predicting a terminal rate above 4.0%.

The US trade deficit widened slightly to $67.4 billion from $61.5 billion in November.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

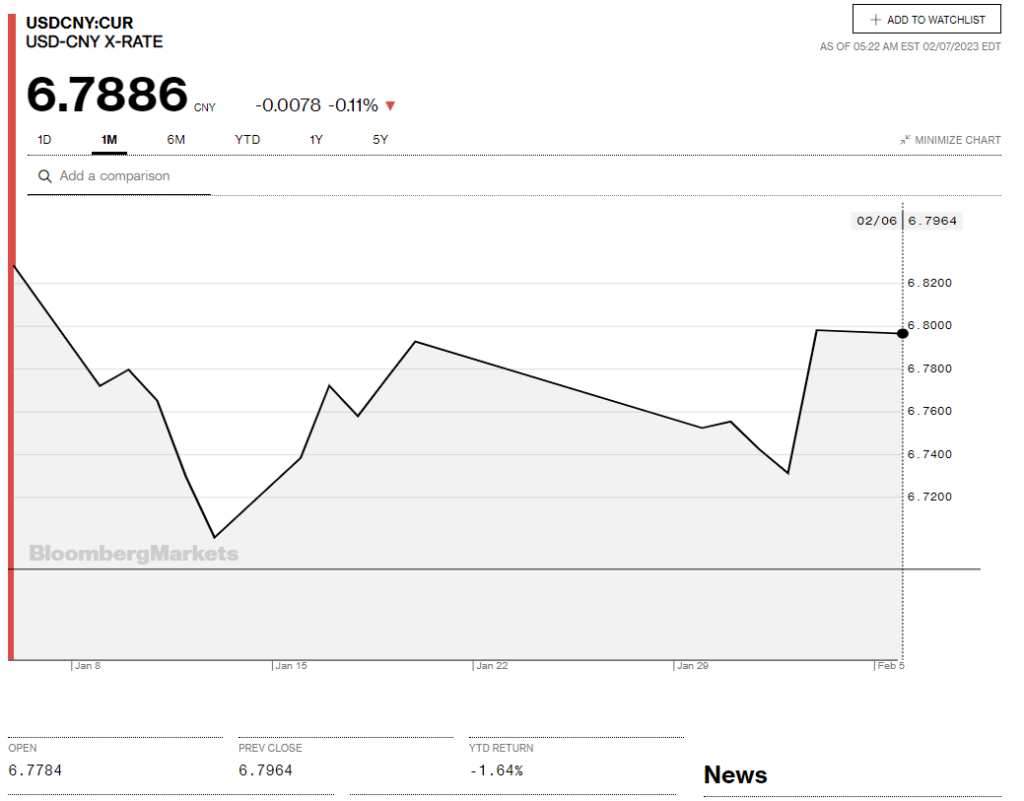

China Snapshot

Bank of China Fix: 6.7967, Previous: 6.7737

Shanghai Shenzhen CSI 300 fell 1.39% % to 4094.23.

China January FX Reserves rose by $56.8 billion to #.184 trillion, more than expected due to a mix of a weakening US dollar and capital inflows.

Chart: USDCNY 1 month

Source: Bloomberg