Photo: BingAI

July 28, 2023

- BoJ tweaks YCC, roils FX markets.

- US data supports dovish Fed.

- USD rallies with a vengeance.

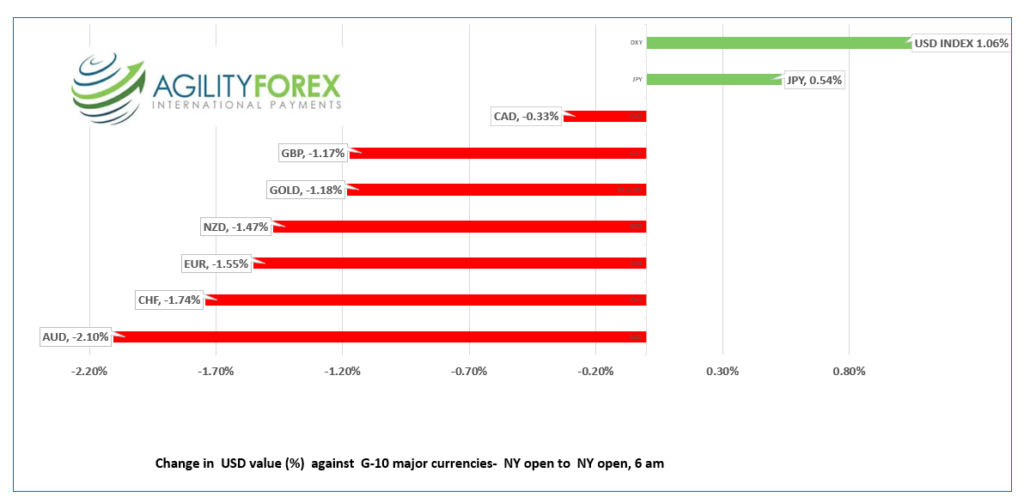

FX at a Glance

Source: IFXA/RP

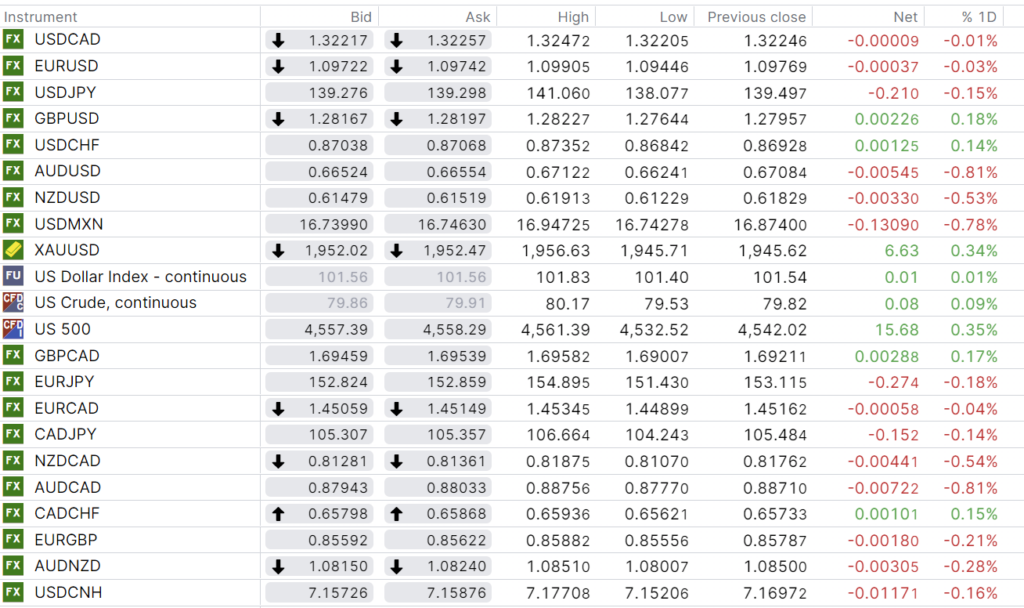

USDCAD Snapshot: open: 1.3222-26, overnight range 1.3203-1.3247, close 1.3225

USDCAD rallied on the back of broad US dollar demand, but the currency pair underperformed compared to the Australian and New Zealand dollars, thanks to steady, but firm oil prices.

Yesterday, WTI rallied to $80.55/b before settling into a $79.53/b-$80.17/b range overnight. Analysts continue to forecast higher crude prices due to hopes for renewed Chinese demand even as Opec and Russian lower production.

Canada May GDP data is expected to show strong growth with the consensus forecast at 0.3% m/m compared to 0 in April. The result is even more impressive when you consider the negative impact from Alberta wildfires and the Federal employees strike.

A perfect storm of soft US ECI and PCE data along with stronger than expected domestic GDP would drive USDCAD down to 1.3150 again.

USDCAD Technical Outlook

The USDCAD technicals flipped to bullish with the move above 1.3200 yesterday. However, the failure to break above the 1.3250-60 resistance area suggests that a breach of the 1.3210 will extend losses to 1.3150.

The USDCAD, two-week uptrend line is at 1.3160 and a move below that level suggests a retest of the 1.23090-1.3100 area.

For today, USDCAD support is at 1.3210-nd 1.3160. Resistance is at 1.3250 and 1.3290. Today’s range 1.3160-1.3250

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

Extreme heat, high humidity, robust US economic data, and central bank verbiage combined to roil markets yesterday afternoon and overnight. We could see more of the same today.

This morning the data-dependent Fed saw more favourable data. Today’s Employment Cost Index (actual 1.0%, forecast 1.1%, previous 1.2%)%, and Core Personal Consumption Expenditures Price Index (actual 4.1% forecast 4.2%, previous 4.6%) are exactly the kind of data they want to see if they do not want to raise rates.Traders liked the news. The US dollar sank, stocks gained, and the US 10-year Treasury yield inched down to 3.968%.

Yesterday, the higher-than-expected US Q2 GDP (actual 2.4% vs. forecast 1.8%), alongside Durable Goods Orders and weekly jobless claims, which were stronger than expected, boosted the US 10-year Treasury yield from 3.869% to 4.023%. This knocked equities down and fueled a US dollar rally. At the same time, ECB President Christine Lagarde was explaining why the risk of a September rate hike was diminishing, which encouraged EURUSD selling.

The overnight session wasn’t as lively, except for USDJPY and yen-crosses. The Bank of Japan got things rolling after its actions confirmed the Thursday afternoon article in the Japanese Nikkei.

USDJPY traded erratically and viciously in a 138.08-141.06 range and is just below the midpoint of that band in early NY trading. The Bank of Japan is to blame for the move. Governor Kazuo Ueda continuously assured markets of the need to maintain its ultra-easy monetary policy and implied it would remain unchanged until the policy review was completed in early 2024. “Liar, liar, pants on fire.”

The BoJ left its benchmark rate unchanged at -0.1% but announced a tweak to its Yield Curve Control (YCC) policy. The 10-year JGB yield cap remains at 0.5% but is now allowed to fluctuate in a +/- band of 1.0%.

EURJPY rode a roller coaster, rising and falling in a 151.03-154.90 range as investors scrambled to unwind carry trades.

Elsewhere, EURUSD consolidated Thursday’s losses in a 1.0945-1.0991 range, and then climbed to 1.01033 post-US data. ECB President Christine Lagarde was far less hawkish than she was at the June 15 meeting. When asked about a September rate hike, she said words to the effect of maybe yes, maybe no. Many analysts are suggesting that Eurozone rates are very close to peaking.

GBPUSD suffered from broad US dollar strength and dropped from 1.2992 yesterday, pre-US data, to an Asian low of 1.2764 before grinding out gains to 1.2886 in NY trading. The recent central bank surprises have GBPUSD traders cautiously awaiting next Thursday’s Bank of England monetary policy meeting.

AUDUSD suffered from broad US dollar strength and dropped from 0.06712 to 0.6624 before rebounding to 0.6665 in NY. Weaker than expected Retail Sales (actual -0.8 vs. forecast -0.1%) didn’t help sentiment.

FX high, low, previous close

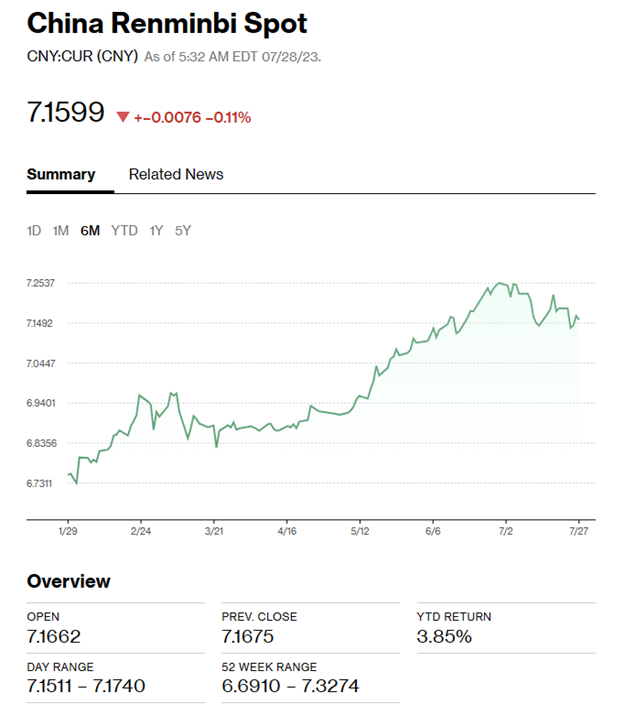

China Snapshot

Bank of China Fix: 7.1338 , forecast 7.1665, previous 7.1265.

Shanghai Shenzhen CSI 300 rose 2.32% to 3992.74.

Stocks rally as investors start to believe in the governments stimulus plans.

PboC official says China plans to create a high-yield bond market to serve needs of small tech firms.

China declares large “No-Sail” zone in South China Sea for military exercises from July 29-August 2.

.Chart: USDCNY 6 month

Source: Bloomberg