June 3, 2024

- OPEC extends production cuts to the end of 2025.

- Eurozone PMI data proves to be a non-event

- US dollar opens with small gains compared to Friday’s close.

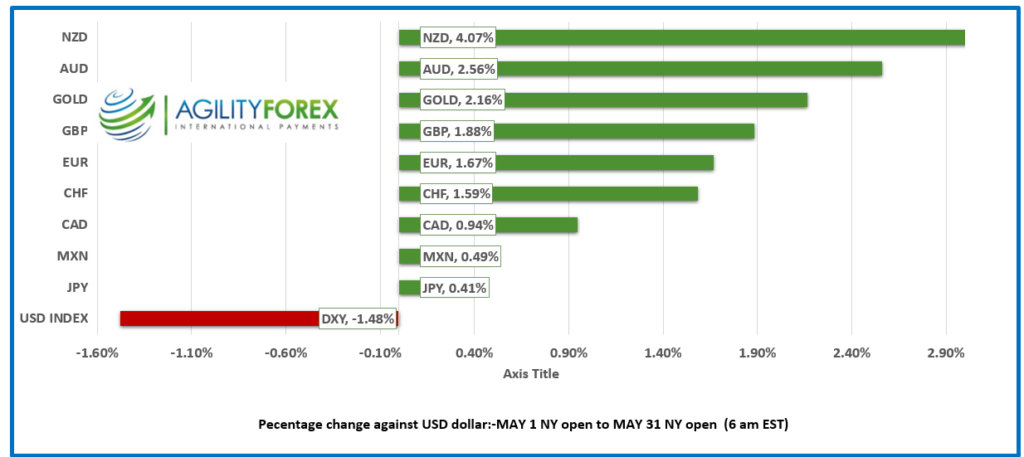

FX at a Glance-May 2024

Source: IFXA/RP

USDCAD open 1.3664, overnight range 1.3606-1.3669, close 1.3631

The Canadian dollar finished May with a 0.69% gain, which was hugely disappointing compared to the 4.07% gain notched by the New Zealand dollar and the 2.56% rally in the Australian dollar. The Canadian dollars poor performance is because of the likelihood that the BoC cuts rates on Wednesday, the RBNZ and RBA have not plans to lower rates this year.

WTI oil traded defensively in a 76.40-77.52 range despite OPEC deciding to extend its 3.6 m/bd production cuts until the end of 2025, a sign that the cartel believes global demand will rise this year.

USDCAD is also trading cautiously ahead of Wednesday’s BoC meeting. The recent spate of weak data including Friday’s poor GDP result have raised the odds for a rate cut on Wednesday, although that sentiment is far from unanimous. Either way, a June or July rate cut is a given, or else BoC Governor risks losing even more credibility.

Today’s US ISM Manufacturing PMI data will drive FX direction.

USDCAD Technicals

The intraday are unchanged from Friday. They are bearish below 1.3670 and looking for a break of support at 1.3610 to extend losses to 1.3550. A break above 1.3770 puts the focus back on 1.3750.

The longer term technicals are bullish with the January uptrend line is intact above 1.3590. In addition 100 day moving average support is at 1.3576 and the 200 day moving averages is at 1.3573.

For today, USDCAD support is in the 1.3510 and 1.3580. Resistance is at 1.3670 and 1.3710. Today’s range is 1.3590-1.3670..

Chart: USDCAD 4 hour

Source: DailyFX

Building to Nonfarm Payrolls

Trading got off to a slow start and even Eurozone and German PMI data didn’t garner much interest. The US interest rate story and the timing of the Fed’s first rate cut is the focus and Friday’s nonfarm payrolls data is expected to either encourage an earlier than expected move or support the “no change until November at the earliest” camp. Even OPEC’s decision to extend production cuts until the end of 2025 did not cause much of a stir. Friday’s close of 4.512% is

Equity Traders Happy Dancing

“Don’t worry, be happy (and long equities)” seems to be the theme in global stock markets. Asian equity indexes closed with solid gains led by the 1.13% rise in Japan’s Nikkei 225 index and the 0.77% gain in Australia’s ASX 200. Hong Kong’s Hang Seng index climbed 1.77%. European indexes followed suit led by a 0.79% jump in the German DAX index. S&P 500 futures are in positive territory and up 0.14%. A drop in the US 10-year Treasury yield to 4.473% from 4.512% is stoking the positive sentiment.

EURUSD

EURUSD traded weakly and dropped from 1.0860 to 1.0827 in NY. S&P Global noted: Eurozone Manufacturing PMI rose to 47.3 in May from 45.7 in April. While this was still below the 50.0 no-change threshold, it was the highest reading in the headline index since March 2023, indicating the slowest deterioration in the health of the euro area goods-producing sector for over a year. Traders are also cautious ahead of Thursday’s ECB meeting.

GBPUSD

GBPUSD erased Friday’s gains and is at the bottom of its 1.2694-1.2756 range. Traders will be jockeying for position for most of this week ahead of Friday’s US nonfarm payrolls report. UK Manufacturing PMI at 51.2 in May. S&P wrote: “May saw a solid revival of activity in the UK manufacturing sector, with levels of production and new business both rising at the quickest rates since early-2022.”

USDJPY

USDJPY traded choppily in a 156.82-157.48 range and is at the bottom of that band in NY. Japan Manufacturing PMI was little changed at 50.4 compared to 50.5 in April while Capex rose 6.8% (forecast 12.2%).

AUDUSD and NZDUSD

AUDUSD danced inside Friday’s range, trading in a 0.6633-0.6665 band. Prices mostly ignored TD Inflation results which saw May inflation rise 3.1% y/y (previous 3.7%) and 0.3% m/m (previous 0.1%). Judo Bank Manufacturing PMI ticked up to 49.7 from 49.6. The improvement in China manufacturing PMI underpinned prices.

NZDUSD rallied Friday and then consolidated the gains in a 0.6133-0.6159 range overnight. Trading was subdued as New Zealand markets were closed today.

USDMXN

USDMXN soared from 16.9179 to 17.3214 as investors showed their displeasure with the Mexican election results. Presidential candidate Claudia Sheinbaum won by over 30% which was expected but markets were spooked by the size of the win of her Morena party, which has won a “super majority.” Investors fear the left-wing party will pass non-market friendly legislation. Time will tell.

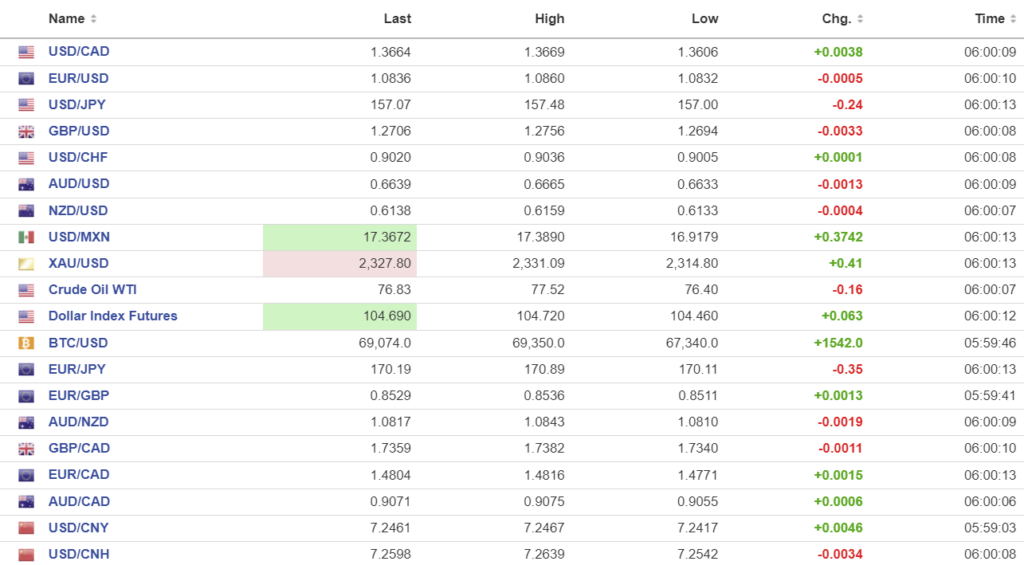

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

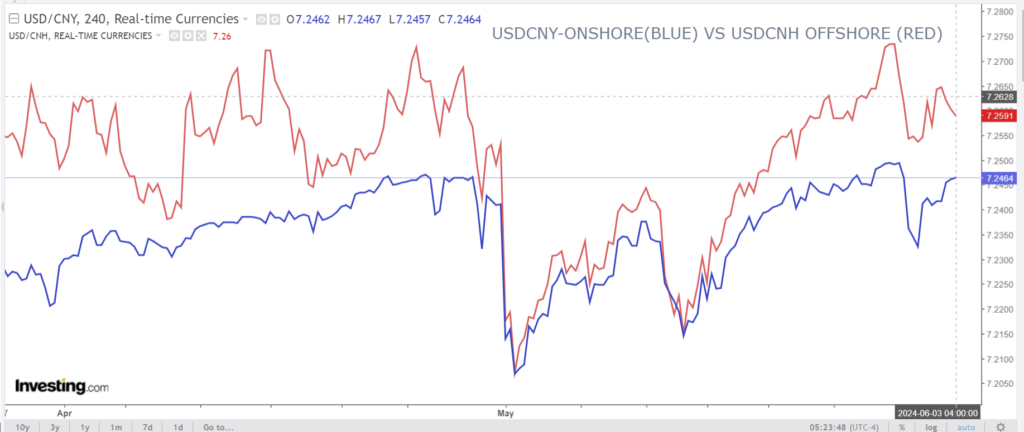

China Snapshot

PBoC fix: 7.1086 vs exp. 7.2378 (prev. 7.1111).

Shanghai Shenzhen CSI 300 rose 0.25% to 3588.75

Caixin May Manufacturing PMI 51.7 (forecast 51.5, previously 51.4).

Moody’s raises China GDP forecast for 2024 to 4.5% from 4.5%

Chart: USDCNY and USDCNH

Source: Investing.com