Photo: Pixabay

March 10, 2023

- US nonfarm payrolls rise 311,000 (January 517,000)

- US Bank stock turmoil continues to weigh on equities.

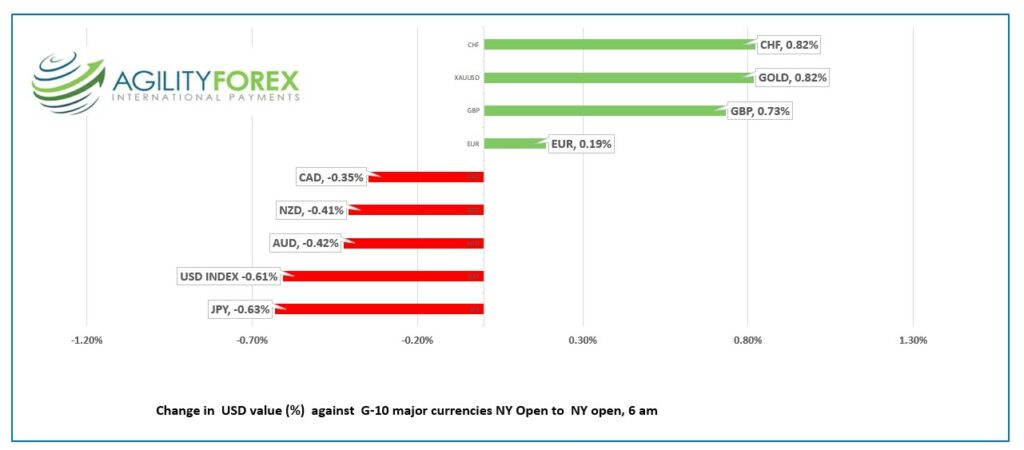

- US dollar opens mixed-commodity currencies underperform.

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3836-40, overnight range 1.3782-1.3860, close 1.3827

Canada gained 21,800 jobs in February, higher than the expected 10,000 increase but well below January’s 150,000. February employment report is expected to show a gain of 10,000 jobs, a steep drop from January’s 150,000 gain. The unemployment rate was unchanged at 5.0%.

USDCAD retreated on the news falling to 1.3782 in early trading.

Bank of Canada Senior Deputy Governor Carolyn Rogers didn’t do the Canadian dollar any favours. She channelled her inner-Stevie Nicks and sang about why the BoC can “go our own way.”

She justified the Bank’s decision to pause hiking rates by saying. “Canada, like other countries, has unique circumstances that will affect the path of the economy and inflation. But that’s the advantage of an independent monetary policy: We can get back to our inflation target of 2% in a way that makes sense for us, just as other central banks are doing for them.”

That may be true in theory but as former Prime Minister Pierre Trudeau once said about the US: “Living next to you is in some ways like sleeping with an elephant. No matter how friendly and even-tempered is the beast, if I can call it that, one is affected by every twitch and grunt.”

With the US responsible for over 73% of Canada’s trade, America’s inflation woes will cross the border as easily as illegal immigrants cross Roxham Road.

USDCAD rallied from 1.3755 to 1.3836 yesterday and peaked at 1.3660 post-data.

Ms Rogers remarks may have provided the currency pair with a modicum of support but the key factor behind the sharp gain was the S&P 500 index plunging 1.85% on US bank woes.

WTI oil prices dropped 4.0% from yesterday to just before NY opened due to the prospect of slower global growth and broad based US dollar demand.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3790, looking for a break above 1.3850 to extend gains to 1.3900, then 1.4000. A move below 1.3790 targets 1.3740. The 4 hour chart shows the uptrend line from February 14 intact above 1.3640 which is also previous resistance and contain a move on a break below 1.3740.

The daily charts indicate USDCAD is overbought based as Bollinger band and RSI studies are at extreme levels.

For today, USDCAD support is at 1.3760 and 1.3730. Resistance is at 1.3850 and 1.3900.

Today’s range 1.3770-1.3870

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

US nonfarm payrolls report surprised to the upside again, rising 311,000 compared to the 205,000 expected. The initial reaction saw the US dollar retreat because Average hourly earnings (4.6% y/y vs forecast 4.7%) and the unemployment rate (3.6% vs forecast 3.4%) were weaker. The US dollar retreated on speculation the data showed cracks in a still strong labour market which suggests the Fed may be less aggressive with hiking rates.

It may not have been a black swan event, but the graceful, long-necked bird swimming in the Sacramento River was a dark shade of gray. US bank stocks took it on the chin yesterday, and the fallout rippled across global equity markets overnight.

Silicon Valley Bank Financial Group (SVG) and Silvergate Capital plunged due to severe financial problems, and contagion from that event knocked all US bank stocks lower. The issue is accounting for bonds Available for Sale and bonds Held-to-Maturity (HTM). Losses (or gains) on HTM bonds are not reported in financial statements. It becomes a major issue when banks need to raise capital and the losses are exposed.

SVG stock fell further on Friday which suggests the post-NFP rebound in S&P futures (-.44%) may be short-lived.

EURUSD traded sideways in a 1.0575 to 1.0606 range then climbed to 1.0643, post-nfp.. German HICP inflation was 9.3% y/y in February, as expected. Traders are cautious ahead of today’s US data and next week’s ECB meeting.

GBPUSD had a good day, rising from 1.1909 to 1.2008 then to 1.2043 after the US data. GBPUSD is also supported by UK January GDP which rose 0.3% m/m, compared to the 0.1% increase expected and the 0.5% drop in December. The results mean a technical recession may be avoided.

USDJPY traded in a 135.83-136.99 range. Some of the gains were because the Bank of Japan left rates and the yield curve control cap unchanged at negative 0.1% and 0.50%, respectively.

AUDUSD traded in a 0.6566-0.6632 range with the peak occurring following the US NFP report.

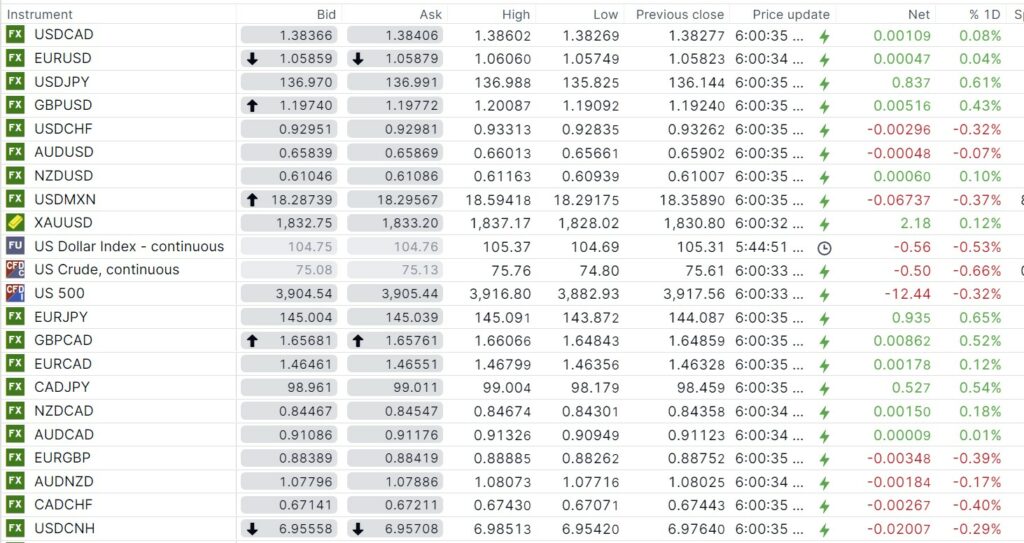

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

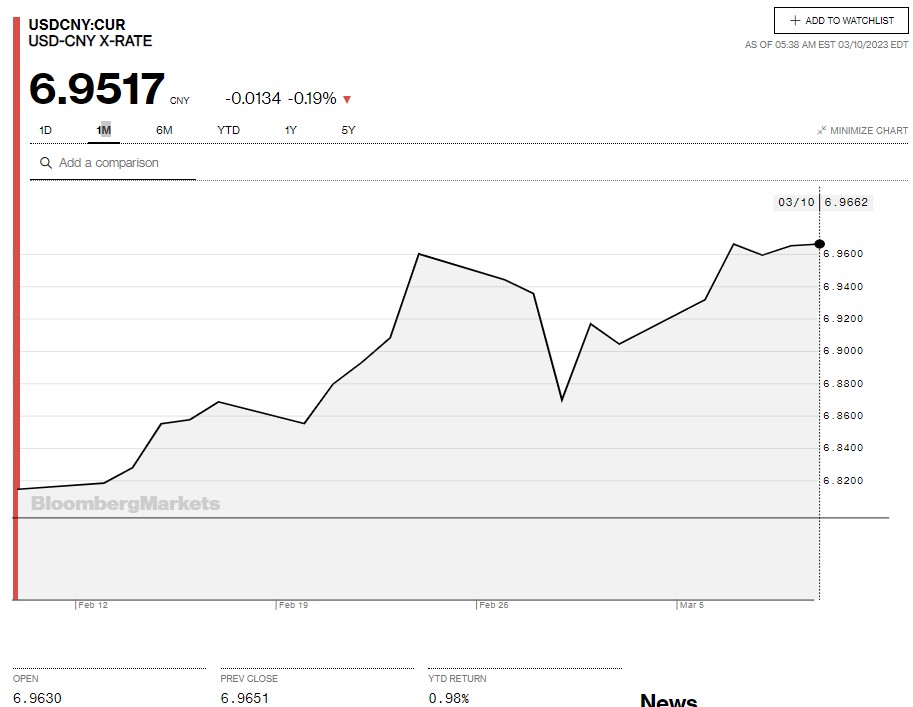

China Snapshot

Bank of China Fix: 6.9655, Previous: 6.9666

Shanghai Shenzhen CSI 300 fell 1.31% to 3967.14.

Xi Jinping was elected (ordained) as State Chairman for a third term, which was a foregone conclusion as there was no opposition that was still alive.

Chart: USDCNY 1 month

Source: Bloomberg