Photo: Creazilla.com/AnnaliseArt on Pixabay

May 23, 2023

- Markets going nowhere as debt talks drag on.

- Powell hints about June rate hike pause

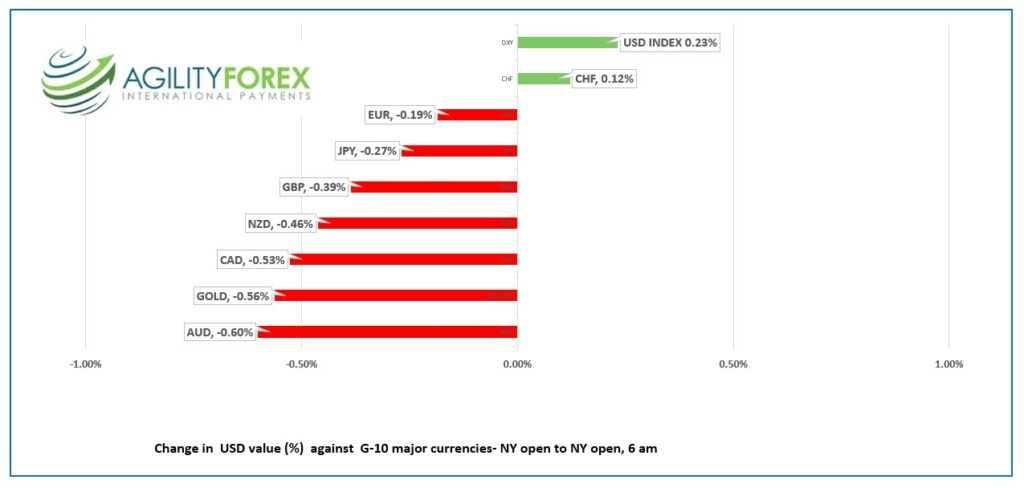

- US opens with gains except against CHF.

FX at a glance-Friday open to Tuesday open

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3542-46, range since Friday close 1.3483-1.3547, close Friday 1.3495, Monday 1.3506

USDCAD rallied on the back of broad US dollar strength due to uncertainty around the US debt crisis. Retail Sales fell 1.4% in March, as expected, but still further evidence that the domestic economy is slowing.

WTI climbed from $70.52/b on Monday to $72.75/b overnight. Saudi Arabian Energy Minister Prince Abdulaziz bin Salman is warning oil short-sellers to “watch-out.” He is feeling pretty smug after last months surprise production cut roiled markets, and another cut is a possibility as short sellers have returned.

Canada Industrial Product Price (IPPI)and Raw Materials Price (RMPI) indexes are heading in the right direction. IPPI fell 0.2% m/m and 3.5% y/y. RMPI fell 10.8% y/y.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3470 after breaking through the top of the symmetrical triangle pattern at 1.3520 overnight, and looking for a test of the 1.3580 area, which was previously support. A topside break targets 1.3660 while a move below 1.3470 puts 1.3410 in play.

For today, USDCAD support is at 1.3470 and 1.3430. Resistance is at 1.3570 and 1.3610.

Today’s range 1.3480-1.3570

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Canadians are returning from a long weekend to discover Alberta is still burning, Chinese authorities have no sense of humour, and Biden and McCarthy continue to play “silly-buggers” with the global financial market.

The G-7 meeting ended with the leaders very politely (and deferentially) telling China its claims to the south China Sea were bunk and to stop interfering with “our communities and democratic institutions.” They also voiced their support for Taiwan. China responded by throwing a comedian in jail for telling a joke about Xi Jinping’s policies.

A gaggle of Fed speakers have expressed contradictory messages since Friday. Even Jerome Powell got into the act.

He spent the past year saying that inflation is too high to justify rate hikes that took Fed funds from 0.25% in March 2022 to 5.25%. On Friday he said that rates are “far above” target, but hinted that a “pause” was possible.

Minneapolis Fed President Neel Kashkari and FOMC voters suggested that a pause on June 14 was a coin flip, but he thinks more rate hikes are appropriate.

Meanwhile, President Biden said he is optimistic about a debt ceiling deal and had a productive meeting with House Speaker McCarthy.

Asian equity indexes closed in negative territory with Japan’s Nikkei down 0.40% and Australia’s ASX 200 almost unchanged. European bourses are modestly lower except the UK FTSE 100 index which has gained 0.15%. S&P 500 futures are down 0.10%. The US 10-year Treasury yield ticked up to 3.746% as of 6:30 am EDT.

EURUSD churned in a 1.0771-1.0820 band with prices weighed down by firmer US Treasury yields. Eurozone PMI data was mixed. Manufacturing PMI fell to 44.6 (previous 45.8) while the Services PMI rose to 55.9 (previous 56.2). The EURUSD downtrend channel is intact between 1.0700 and 1.0840

GBPUSD traded with a bearish bias in a 1.2375-1.2470 range, undermined in part by disappointing UK PMI data.

The Chief Business Economist at S&P Global wrote: “The UK is therefore seeing a tale of two economies, with the divergence between manufacturing and services posing difficulties for policymakers. However, it’s the far larger service sector that will typically dictate policy, meaning these survey results are nothing but hawkish in suggesting the Bank of England has more work to do to quash stubbornly high inflationary pressures in the services economy. The intraday technicals are bearish below 1.2460, looking for a test of support at 1.2340.

USDJPY rose from 137.49 to 138.87, boosted by the US 10-year Treasury yield rising from yield from 3.65% yesterday to 3.75% this morning.

AUDUSD traded with a negative bias in a 0.6612-0.6660 range due bearish risk sentiment.

NZDUSD traded in a 0.6236-0.6301 range overnight with traders awaiting the RBNZ monetary policy decision. Economists are predicting a 25 bp bump and a hawkish statement.

The US data (New Home Sales, Redbook Index and S&P Global PMI) will not be a factor for traders as they are fixated on debt ceiling news.

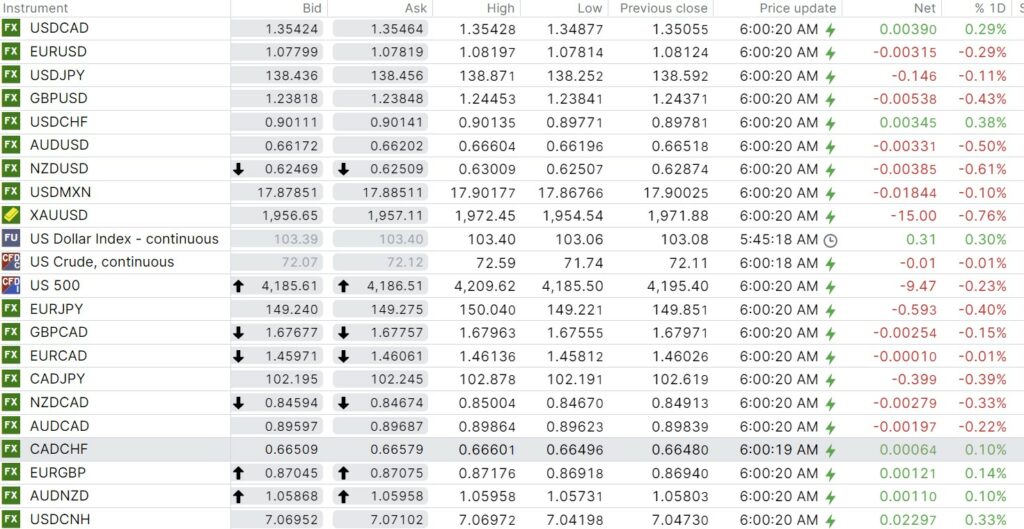

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

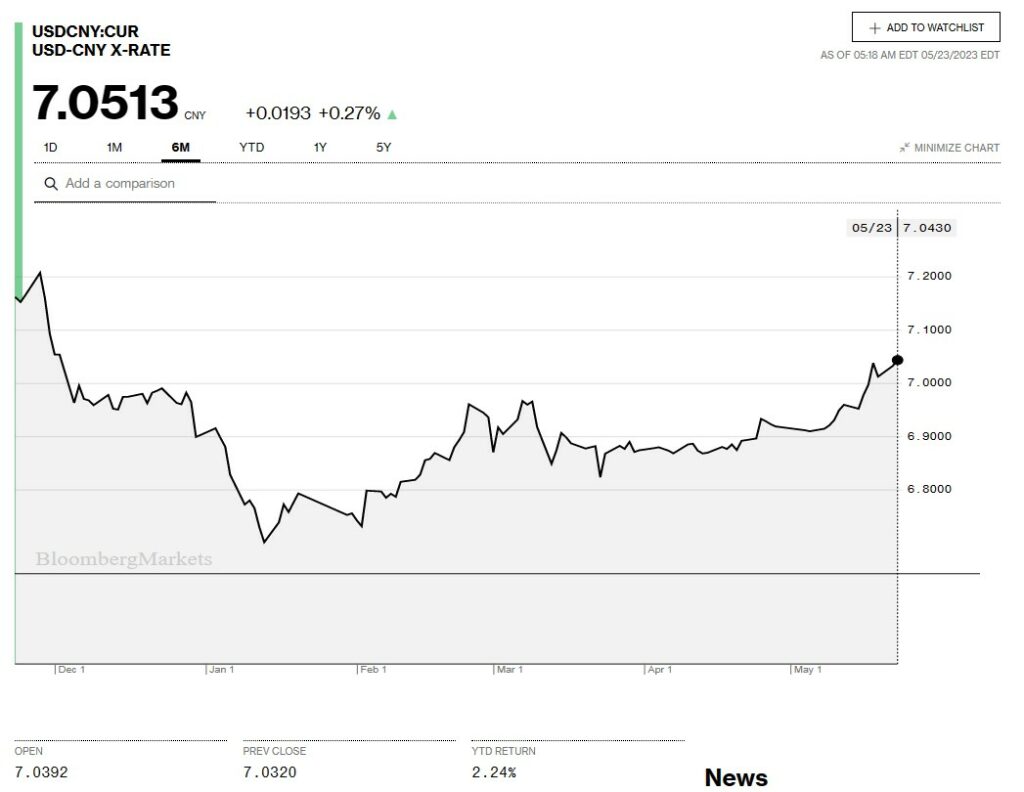

China Snapshot

Bank of China Fix: 7.0326, (Monday 7.0157, Friday 7.0356)

Shanghai Shenzhen CSI 300 fell 1.41% to 3913.19. (Monday close 3969.33

PBoC leaves rates unchanged.

1-Year Loan Prime Rate (May) 3.65% vs. Exp. 3.65% (Prev. 3.65%)

5-Year Loan Prime Rate (May) 4.30% vs. Exp. 4.30% (Prev. 4.30%)

Chart: USDCNY 1 month

Source: Bloomberg