October 15, 2024

- Oil prices slide on soft 2025 oil demand forecast.

- Canada Inflation falls 0.4% m/m in September

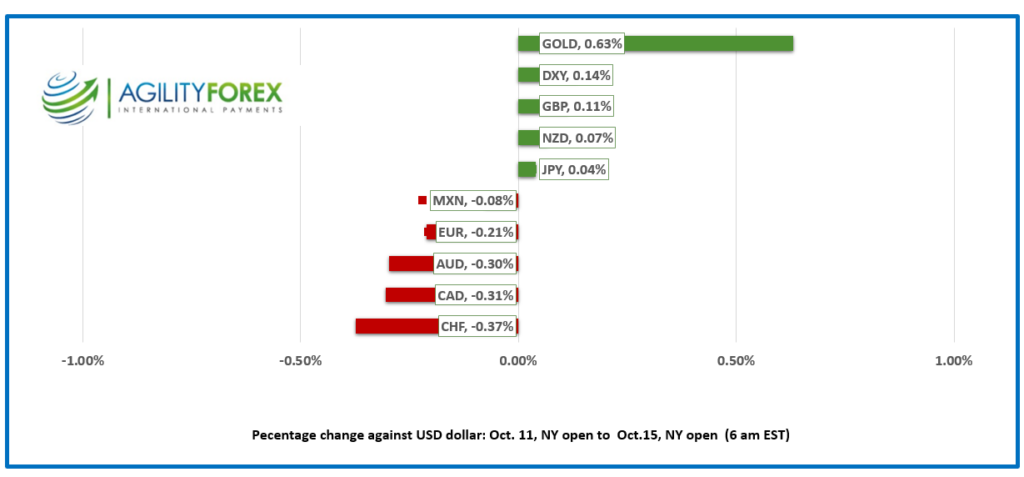

- US dollar opens mixed-CAD and CHF underperform

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3809, range since Mon. 1.3758-36, close Oct. 11, 1.3763. Oct. 14, 1.3797

USDCAD jumped from 1.3819 to 1.3836 after inflation cooled by 0.4% m/m in September (August -0.2%) and rose 1.6% compared to the forecast for a 1.8% increase and 2.0% y/y in August. This data combined with Friday’s labour force survey almost guarantees a 50 bps rate cut on October 23.

It’s handbags at dawn for Canadian and Indian politicians. Canada accused Indian diplomats of homicide, extortion, and other criminal acts. The Indian Prime Minister responded by saying they were “preposterous imputations.” It is a full-blown “roti fight.”

The Bank of Canada Business Outlook Survey released Friday painted a picture of weak demand and falling inflation pressures. CPI is expected to rise 1.8% y/y in September, compared to 2.0% in August.

USDCAD technicals

The intraday USDCAD are bullish with the uptrend channel from October 2 intact while prices are above 1.3750 and targeting further gains to 1.3850, then 1.3890. A break below 1.3750 risks a sell-off to 1.3650.

Longer term Fibonacci studies suggest that the convincing move above the 61.8% Fibonacci retracement level of 1.3400 (the April 2001-October 2007-monthly chart, suggests further gains to 1.4550 are in the cards.

For today, USDCAD support is at 1.3780 and 1.3750. Resistance is at 1.3850 and 1.3890

Today’s Range 1.3780-1.3880

Chart: USDCAD daily

Source: Investing.com

Risk of Oil Glut Rises

Oil traders are disappointed to learn that Israel’s expected retaliation against Iran’s October 1 missile barrage will not target oil infrastructure or nuclear facilities. At least, that’s what the WSJ says Israeli diplomats are telling the US. WTI fell 5.31% overnight and a total of 8.3% since Friday. WTI’s Friday-Monday weakness was due to news that OPEC cut its forecast for oil demand growth for 2024 and 2025, as Chinese crude imports fell 3% from January to August. The International Energy Agency (IEA) concurs—it’s predicting that oil supply will outpace oil demand in 2025.

Fed-speak Underpins Greenback

Slow and steady wins the race and sets the pace for lower US interest rates—at least, that’s what two Fed officials are suggesting. Governor Christopher Waller said, “I view the totality of the data as saying monetary policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting.” Cleveland Fed President Neel Kashkari is advocating further “modest reductions.” The greenback is bid due to the prospect of steady US rates and falling rates in Europe, the UK, and Canada.

Oil traders are disappointed to learn that Israel’s expected retaliation against Iran’s October 1 missile barrage will not target oil infrastructure or nuclear facilities. At least, that’s what the WSJ says Israeli diplomats are telling the US. WTI fell 5.31% overnight and a total of 8.3% since Friday. WTI’s Friday-Monday weakness was due to news that OPEC cut its forecast for oil demand growth for 2024 and 2025, as Chinese crude imports fell 3% from January to August. The International Energy Agency (IEA) concurs—it’s predicting that oil supply will outpace oil demand in 2025.

EURUSD

EURUSD climbed from 1.0885 to 1.0917 overnight after dropping from 1.0937 yesterday. The prospect of a US “soft landing” and a slow pace of Fed rate cuts is weighing on the single currency ahead of an expected 25 bp rate cut by the ECB on Thursday. ZEW Survey results show that the economic situation in Germany worsened, falling to 86.9 from 84.5. EURUSD technicals are bearish and looking for a break below 1.0870 to extend losses to 1.0770.

GBPUSD

GBPUSD traded in a 1.3035-1.3087 range and is at the top of that band in early NY. Prices drifted sideways since Friday’s close until today’s UK employment report when GBPUSD caught a bid. The UK unemployment rate rose 4.0%, compared to expectations for a 4.1% increase, while average earnings fell. The GBPUSD rally may be temporary as the BoE is expected to cut rates in November and December.

USDJPY

USDJPY rallied to 149.84 then retreated steadily, mostly because the US 10-year Treasury yield fell from 4.14% yesterday to 4.07% today. Analysts are split as to whether the BoJ raises rates before year-end.

AUDUSD & NZDUSD

AUDUSD traded sideways and negatively in a 0.6715-0.6762 range. Prices were pressured following disappointment after China’s Finance Ministry failed to announce stimulus measures and by general US dollar strength. NZDUSD traded in a 0.6073-0.6097 range ahead of NZ inflation data tomorrow.

USDMXN

USDMXN climbed steadily, rising from 19.3683 to 19.5325 due to falling Mexican consumer confidence and fallout from China’s failure to announce fresh stimulus measures. The prospect of a slower pace of Fed rate cuts is also supporting USDMXN.

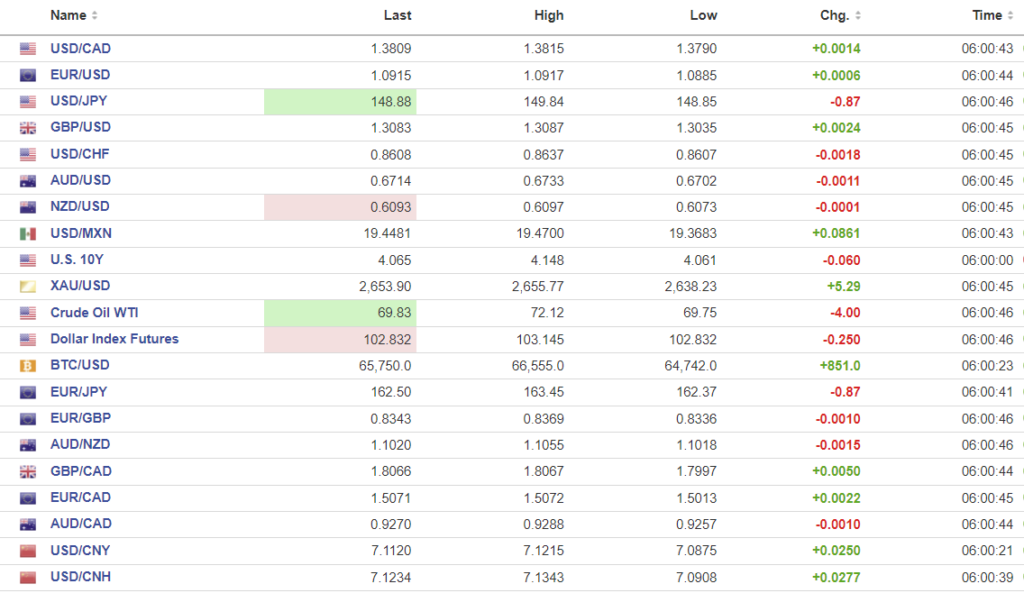

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: Monday 7.0723 vs exp. 7.0722 (prev. 7.0731

Tuesday 7.0830 vs exp. 7.0840 (prev. 7.0723)

Shanghai Shenzhen CSI 300 fell 2.66% to 3855.99

China’s Trade surplus shrinks to $81.71 billion from $91.02B due to lower exports. Exports rose 2.4%, compared to 8.7% in August. CPI rose 0.4% y/y in September compared to 0.6% in August, while PPI fell 2.8%.

Saturday’s Finance Ministry briefing failed to live up to expectations. Authorities did not provide a dollar amount for any of the planned “supports” and investors were disappointed.

Xi Jinping ordered the Chinese Defense Minister to launch a ”mock invasion” of Taiwan. Chinese warships circled the island and the air force sent 125 planes into Taiwan airspace.

Chart: USDCNY and USDCNH

Source: Investing.com