Source: Wikipedia

Rapid spread of delta COVID-19 variant a risk to global recovery

Euro area data a tad firmer than forecast

US dollar opens on firm footing due to risk off sentiment

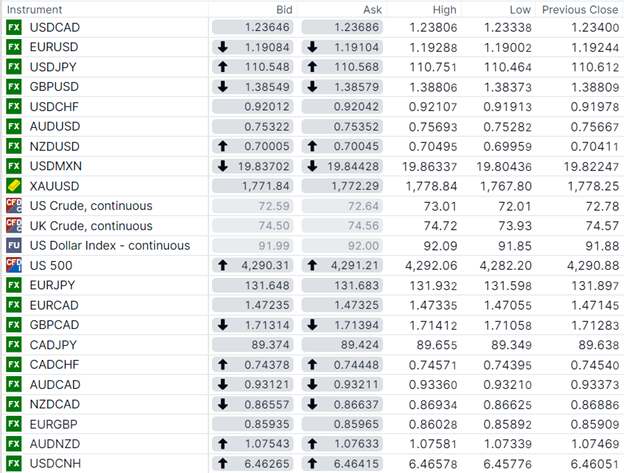

USDCAD open 1.2365-69, Overnight range 1.2334-1.2381, Previous close 1.2340

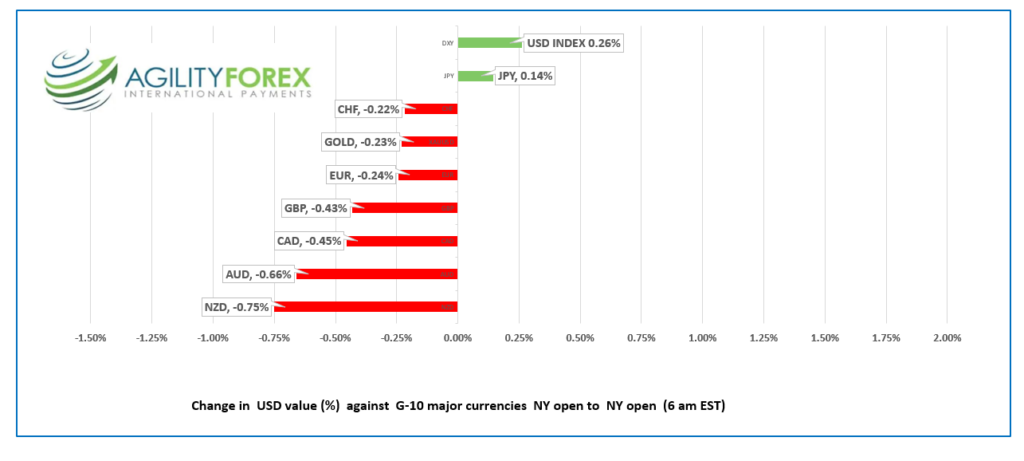

FX at a Glance

FX Recap and outlook

Wall Street may have closed with an upbeat note, but that wasn’t the case in Asia. Japan’s Nikkei 225 index and Hong Kong’s Hang Seng index closed down 0.81% and 0.94%, while Australia’s ASX 200 index finished almost flat.

European equity indexes are far perkier, with the German DAX leading the charge higher. S&P 500 futures are flat, and oil and gold prices are lower. USD 10-year yields slipped to 1.482% from 1.57% in Asia.

The delta variant of Covid-19 has forced the reimposition of lockdown measures in major regions of many countries, including Australia, Malaysia, and sparked fears of another mass outbreak derailing the global recovery.

The greenback is also bid on renewed taper talk. The WSJ reported the FOMC discussed tapering mortgage-backed securities purchases as they may be helping to fuel the housing boom. Taper-Lite, perhaps.

EURUSD dropped from 1.1929 to 1.1884 in NY. German HiCP inflation dipped to 2.1% y/y in June, compared to 2.4% in May, but the result was expected. Eurozone Economic Sentiment Index (actual 117.9 vs May 114.5) and Services Sentiment (actual 17.9 vs May 11.2) were firmer than expected. Nevertheless, US dollar demand from negative risk sentiment along with month-end, quarter-end, and half-year end flows are weighing on prices. The move below 1.1900 targets 1.1840.

GBPUSD mirrored EURUSD price action, falling from 1.3881 in Asia to 1.3824 in NY. The UK Nationwide Housing Price Index jumped to 13.4% from 10.9%, y/y in June. Rising numbers of new COVID-19 cases weighed on prices. The intraday technicals are bearish below 1.3870.

USDJPY traded in a 110.46-110.75 band, with prices weighed down by softer US 10-year Treasury yields and mild risk aversion sentiment. Japan’s unemployment rate rose to 3.0% from 2.9% in April, and Retail trade was 8.2% y/y in April, compared to 11.9% in March.

AUDUSD and NZDUSD traded with a negative bias due to negative risk sentiment. AUDUSD also suffered from its latest COVID-19 lockdown measures. Traders are hoping that China NBS Manufacturing PMI and ANZ Business Confidence data tomorrow provide some direction.

USDCAD climbed on the back of broad US dollar demand. The drop in WTI from $74.36/b to $72.40/b today, but have since rebounded to $73.50/b which may be acting as a drag on USDCAD gains.

The Canadian economic calendar is empty, and the US calendar is light. Case-Shiller Home Price Index (forecast 14.5 vs previous 13.3) and Consumer Confidence are due.

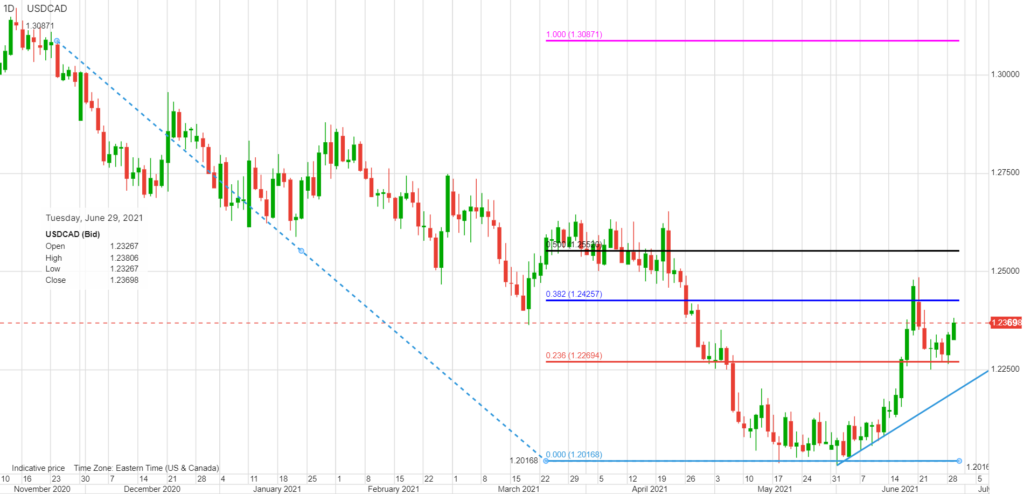

USDCAD technical outlook

The intraday USDCAD technicals are bullish above 1.2310, looking for a break above 1.2400 to extend gains to 1.2460, which is downtrend line resistance from the end of November. A break below 1.2190 would negate the uptrend and put the focus on 1.2000. Fibonacci retracement projects further gains to 1.2425. For today, USDCAD support is at 1.2340 and 1.2310. Resistance is at 1.2400 and 1.2440. Today’s range 1.2340-1.2440.

Chart USDCAD daily

Source: Saxo Bank

FX open, high, low, previous close

Source: Saxo Bank