Photo:Bing AI

August 1, 2023

- RBA leaves rates unchanged

- China Manufacturing PMI weaker than expected.

- USD dollar rebounds after month-end sell-off.

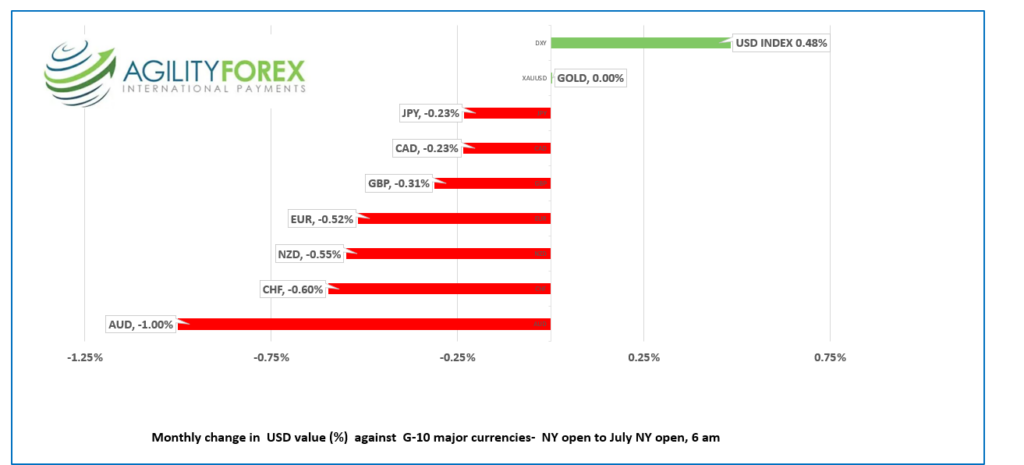

FX at a Glance

Source: IFXA/RP

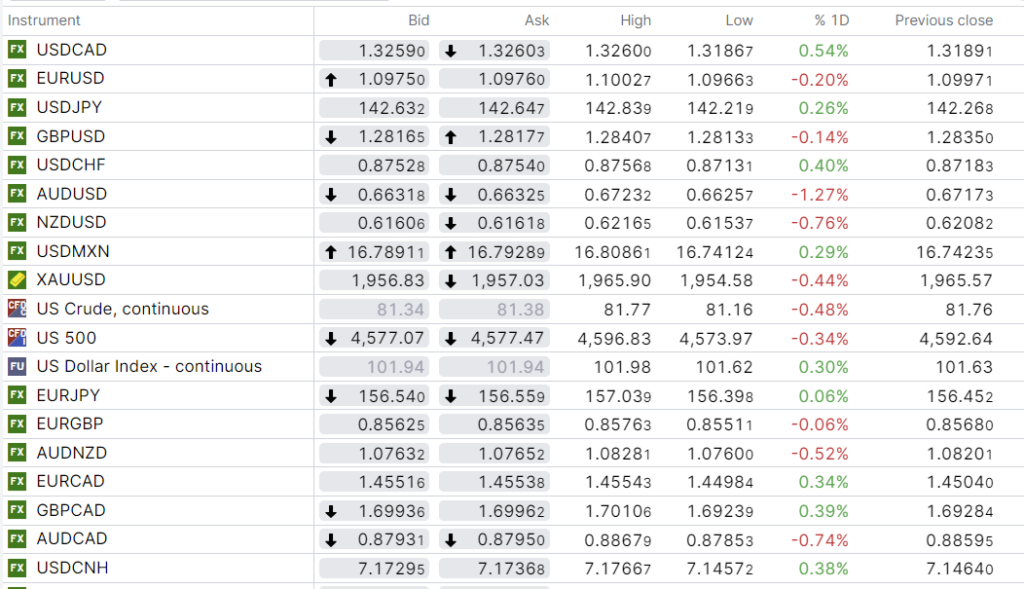

USDCAD Snapshot: open: 1.3258-62, overnight range 1.3187-1.3296, close 1.3189

USDCAD was sold aggressively yesterday due to month-end portfolio rebalancing requirements but support in the 1.3150 area held. Prices rebounded, then accelerated overnight with the break above 1.3230, targeting 1.3300.

Top-tier Canadian data is scarce until Friday’s unemployment report, leaving USDCAD direction at the mercy of global risk sentiment.

WTI oil prices remained firm, trading in a $81.16-$81.77/barrel range which is helping to slow USDCAD gains.

The US and Canada 10-year interest rate spreads have narrowed slightly in Canada’s favour and as long as the market expects the Fed to pause while a BoC rate hike is a strong possibility, USDCAD gains may be limited.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish following the break above 1.3220 and are looking for a break above 1.3305 to extend gains to 1.3360. A move below 1.3220 will negate the short term upside pressure and target 1.3150, again.

The 1.3100-1.3305 range has contained price action for the past three-weeks and is likely to hold until Friday’s US and Canadian employment reports are released.

For today, USDCAD support is at 1.3230 and 1.3170. Resistance is at 1.3305 and 1.3360. Today’s range 1.3210-1.3305.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

The S&P 500 is close to its 2023 peak, and investors are bullish. However, Fed Chair Jerome Powell is saying, “I know you are, but what am I?” Pee-wee Herman never got an answer, but maybe things are different this time.

The Fed’s “pause, hike” debate will rage throughout August with every major data release, and today, traders are keying in on the June JOLTS job openings report and ISM Manufacturing PMI.

EURUSD is at the bottom of its 1.0959-1.1003 band due to a bout of negative risk sentiment sparked by weak China Manufacturing PMI. Eurozone data was mixed. The unemployment rate fell to 6.4% y/y from 6.5% in June. Manufacturing PMI was a soft 42.7 but as expected.

GBPUSD dropped to 1.2765 from 1.2840 due to rising recession fears after S&P Global Manufacturing PMI fell to 45.3, which the statement said was “the lowest reading for the year and the weakest since May 2020.” UK Housing prices fell 3.8% y/y.

USDJPY rallied from 142.21 to 142.84 overnight and extended the gains to 143.18 in NY trading, coinciding with the US 10-year Treasury yield rising to 4.013% from 3.97% at yesterday’s close. The gains are also supported by Bank of Japan officials stressing that last Friday’s YCC tweak was merely “meant to increase the sustainability of monetary easing and not a shift in policy.” Bloomberg reported that a recent poll suggested the BoJ will leave monetary policy unchanged until April 2024.

AUDUSD sank to 0.6611 from an overnight peak of 0.6723. The sell-off started when the RBA left interest rates unchanged at 4.1%, surprising half of the market, and was exacerbated by the Chinese PMI report. The RBA statement said that further tightening may be required.

FX high, low, previous close

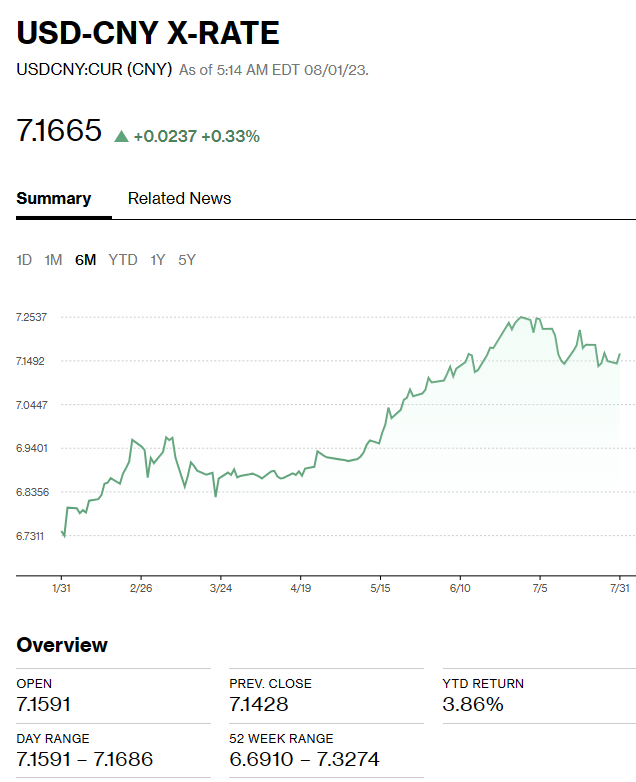

China Snapshot

Bank of China Fix: 7.1283 , forecast 7.1495, previous 7.1305.

Shanghai Shenzhen CSI 300 fell 0.41% to 3998.00.

Caixin Manufacturing PMI dipped into contraction territory in July, falling to 49.2 from 50.5 in June.

Chart: USDCNY 6 month

Source: Bloomberg