Photo: Bing Image Creator

November 7, 2023

- RBA hikes rates by 25 bps to 4.35%

- Weak Chinese export data sours risk sentiment.

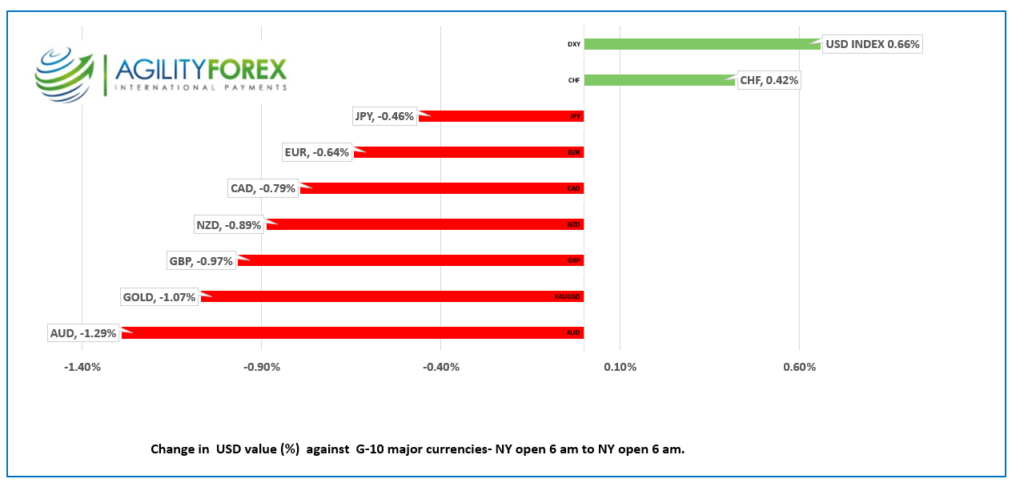

- US dollar recoups losses from Friday-CHF outperforms.

FX at a Glance

Source: IFXA/RP

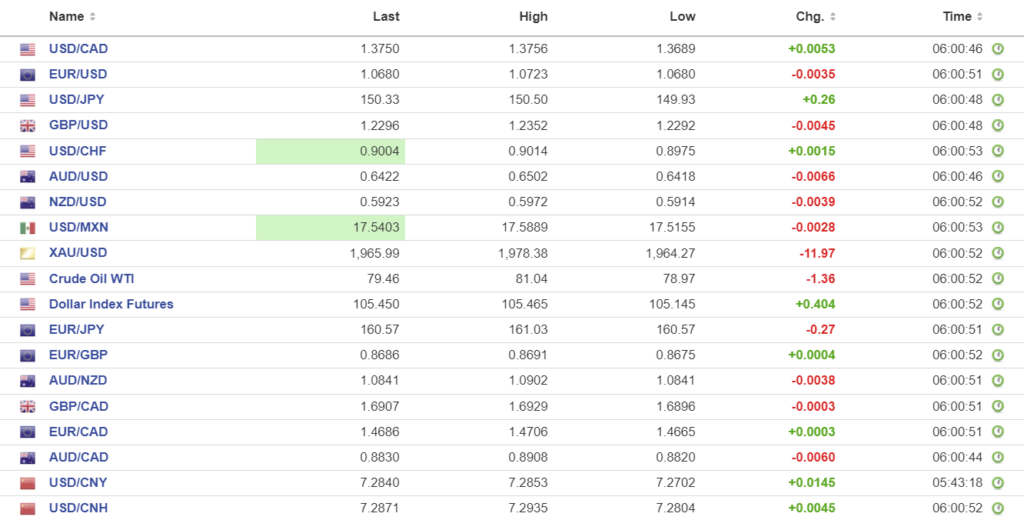

USDCAD Snapshot: open 1.3748-52, overnight range 1.3689-1.3760, close 1.3700

Yesterday, traders were quickly disabused of the notion that it was okay to ignore falling oil prices and softer than expected employment data amidst ongoing geopolitical tensions. USDCAD fully recovered all of Friday’s US and Canadian employment report losses in the face of higher Treasury yields and hawkish comments from Fed officials.

The Bank of Canada’s Q3 Market Participants Survey (results are from 30 market participants) may have encouraged USDCAD buying. The survey predicted the first BoC rate cut would occur in April 2024, which is at least three months earlier than market expectations for a Fed rate cut. All respondents believe that rates have peaked at 5.0% for this cycle.

Oil prices are choppy with WTI bouncing in a $78.97-81.04/b range overnight mainly due to the rise in the US dollar.

Canada’s trade surplus widened to $2.04 billion from $0.95 billion in August.

USDCAD Technicals:

The hourly technicals flipped to bullish with the break above 1.3680 yesterday and are looking for a decisive break above 1.3770 to extend gains to 1.3860. A break below 1.3720 suggests further weakness to 1.3680.

The uptrend line from the middle of July remains intact while prices are above 1.3570, a level guarded by support in the 1.3640-60 zone.

For today, USDCAD support at 1.3720 and 1.3680. Resistance at 1.3770 and 1.3820. Today’s expected trading range is 1.3710-1.3790

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The greenback pulled itself off the ropes yesterday and laid a beating on dollar bears. The rally looks to be confirmation that Friday’s post-NFP US dollar sell-off was mostly an overdue correction rather than a trend change.

Yesterday, Fed Governor Lisa Cook injected a note of caution to markets when she warned that “Vulnerabilities at certain NBFIs could play a key role in amplifying stress associated with tightening financial conditions and slowing economic activity.” Traders may have taken her comments to mean the US economy wasn’t all sunshine and unicorns. Her colleague, Minneapolis Fed President Neel Kashkari, warned that it was too early to think that the inflation fight was over. He said, “Before we declare that ‘we’re absolutely done, we’ve solved the problem,’ let’s get more data and see how the economy evolves.”

Overnight, weaker than expected Chinese export data suggests that a Chinese-led, global economic rebound may be delayed further.

Japan’s Nikkei 225 index led Asian equity indexes lower, and it closed down 1.34%. European bourses are trading in negative territory except for the UK FTSE 100, which is flat. S&P 500 futures are down 0.22% as of 5:30 am PT

EURUSD dropped from 1.0758 yesterday to 1.0665 in NY as traders decided that the Friday-Monday rally had gone too far, too fast. Weaker than expected German industrial data (-1.4% vs forecast -0.1% in September) and Euro area producer prices, which were down 12.4%, were largely ignored by traders.

GBPUSD peaked at 1.2427 yesterday, dropped to 1.2342 by the close, then added to the losses overnight, and opened at the bottom of the 1.2275-1.2354 range. The steep drop may be partly in reaction to Bank of England Chief Economist Huw Pill’s comments yesterday. He seemed to agree with market pricing that predicts a rate cut in August 2024, saying the forecast “doesn’t seem totally unreasonable, at least to me.” Halifax House Prices rose 1.1% m/m in October (forecast -0.3%).

USDJPY climbed steadily, rising from 149.93 to 150.65 on the back of the rebound in US 10-year Treasury yields from 4.58% at Friday’s close to 4.637% by the end of yesterday, then ignored the retreat to 4.591% in NY today. Prices also rallied in tandem with broad-based US dollar demand.

AUDUSD is near the bottom of its overnight 0.6409-0.6502 despite the RBA hiking rates by 25 bps to 4.35%. The odds for such a move were 50/50, but it would appear traders were long AUDUSD going into the RBA meeting as the reaction is a classic “buy-the-rumor, sell-the-fact” move.

Analysts are divided as to whether the statement was hawkish or dovish. Those picking “dovish” point to the line “whether further tightening of monetary policy is required will depend upon the data and the evolving assessment of risks.”

The hawkish camp points to the RBA’s expressed concerns about the slow pace of inflation declines and to the sentence “Whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks.”

The US trade deficit widened to $61.5 billion from $58.78 billion.

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1776, expected 7.2854, previous 7.1780.

Shanghai Shenzhen CSI 300 fell 0.36% to 3619.76.

China October Trade Balance: $56.53 billion vs forecast $81.95 and $77.71 billion in September.

Exports fell 6.4% (forecast -3.1%) while imports rose 3.0% (forecast -6.2%).

IMF raises China 2023 GDP growth forecast to 5.4% from 5.0% predicted in October and 4.6% in 2024, up from 4.2%. Slow growth in 2024 will be due to ongoing property developer risks.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com