Photo: publicdomainvectors.org

- ECB hikes 50 bps, predicts more to follow

- Bank of England and Swiss National Bank hike rates 50 bps

- US dollar rallies in the post-FOMC world

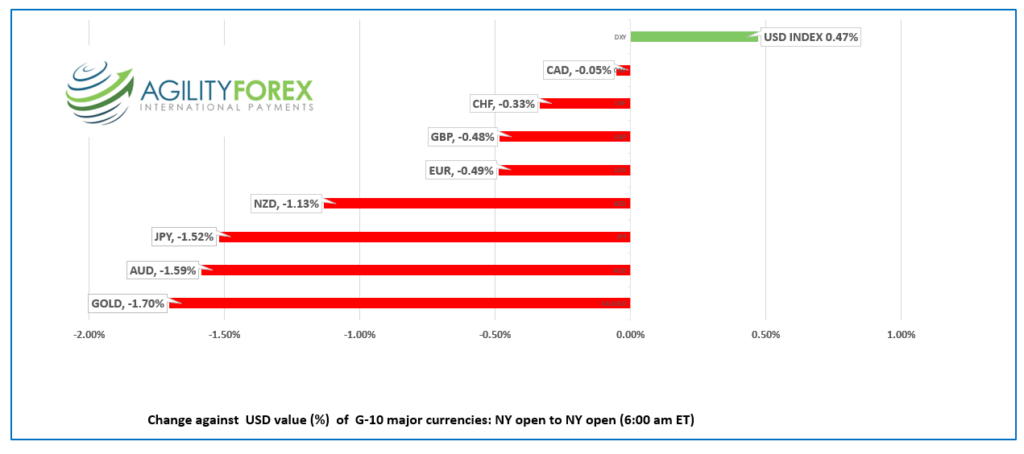

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3566-70, overnight range 1.3543-1.3631, close 1.3547

USDCAD soared and sank after the FOMC statement, Summary of Economic Projections (SEP) and Fed Chair Powell’s press conference.

When the dust had settled from all the drama and volatility, USDCAD opened today unchanged from yesterday while see-sawing in a very similar range to Wednesday’s overnight session. Bill Murray’s, Groundhog Day character understands.

The non-reaction is fading in NY trading today. USDCAD rallied to 1.3623 as S&P 500 futures dropped 1.60% (as of 5:30 am PT).

USDCAD is also supported by divergent Fed and BoC interest rate outlooks. The BoC indicated that they are pausing increases while the Fed said more hikes are in the pipeline.

WTI oil prices rallied from $70.25/barrel on Monday to $77.73/b overnight, a 10.6% gain which is helping to slow USDCAD gains. The renewed demand for oil is because of China’s accelerating reopening plans and the latest International Energy Agency (IEA) forecast suggesting that in 2023 prices will rise further do to lower Russian oil production.

US weekly jobless claims were 211,000, 19,000 lower than forecast which supported USDCAD.

USDCAD technical outlook.

The intraday USDCAD technicals flipped to bullish in early NY trading with the break above 1.3590 that sets the stage for a retest of the mid-October downtrend line at 1.3650. A break above that levels suggests further gains to 1.3790.

A break below 1.3510 targets the November uptrend line at 1.3380.

For today, USDCAD support is at 1.3570 and 1.3520. Resistance is at 1.3630 and 1.3660

Today’s range 1.3540-1.3630

Chart: USDCAD 4 hourly

Source: Saxo Bank

G-10 FX recap and outlook

The highly anticipated December 14 FOMC meeting proved to be as big a flop as the Christian Bale, Margot Robbie film Amsterdam, which cost $90 million to make and earned just $30 million. At least initially.

The Fed hike rates to 4.25% as expected, raised its 2023 inflation forecast, increased the dot-plot terminal rate guess to 5.1%, and said further rate hikes were likely.

Traders took the results with a grain of salt which suggests they do not accord this Jerome Powell Fed the same respect that his predecessors enjoyed. Or else it could just be that no one was around to care.

Asian markets seemed to take the Fed at face value. Hong Kong’s Hang Seng fell 1.55% and Australia’s ASX 200 dropped 0.64%., although those results may have had more to do with Chinese data then the Fed.

European bourses trade defensively with the German Dax down 1.64% after the ECB rate hike. Gold (XAUUSD) has lost $64.30 from where it closed while WTI oil is a touch firmer. The US 10-YEAR Treasury yield drifted down to 3.457%

US Retail Sales and Philadelphia Fed data were weaker than expected which increases the risk the US is heading for a recession. However, the weekly jobless claims report was robust which took some of the sing out of the news.

EURUSD is chopping about in a 1.0607-1.0683 band in NY. The ECB raised rates 50 bps and warned that they will have to rise further to reach levels that are restrictive. They believe inflation will fall to 6.3% in 2023, which is 0.8% higher than its previous estimate. EURUSD needs to break above 1.0750 or risk falling to 1.0200.

The Swiss National Bank (SNB) hiked rates 50 bps as expected and increased its medium-term inflation forecast, setting the stage for a similar result from today’s ECB meeting. Norway’s Norges Bank increased its benchmark rate by 25 bps, to 2.75%.and suggested rates would increase to 3.0% in 2023.Gdp growth was downgraded to 0.5% from 0.9% for 2023.

GBPUSD dropped from its post-FOMC peak of 1.2443 to 1.2289 in the wake of the widely expected 0.50% rate bump by the Bank of England but has since climbed to 1. 2322.

The rate decision was not unanimous. Governor Bailey and five colleagues voted for the 50 bp move, two were against hiking rates at all, and one wanted a 75bp hike. Policymakers also suggested further rate hikes were needed.

USDJPY traders seemed to be the only ones taking the Fed’s forecast to heart. Prices rose from 134.85 yesterday afternoon to 136.92 in Europe.

AUDUSD fell from 0.6869 to 0.6752. Prices traded sideways in early Asia underpinned by strong than expected employment data. Australia gained 64,000 jobs (forecast 19,000) and the October results were revised 11,000 higher to 43,100. AUDUSD dropped following weaker than expected Chinese data and broad US dollar strength.

NZDUSD is at the bottom of its 0.6363-0.6462 range due to renewed US dollar strength, after stronger than expected Q3 GDP growth (actual 6.4% vs forecast 5.5%) was ignored.

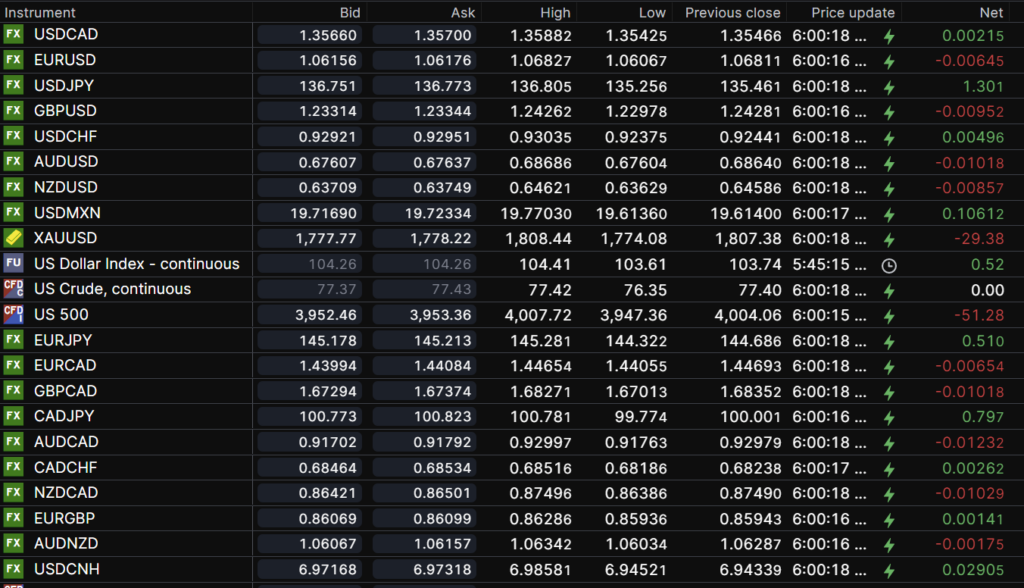

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

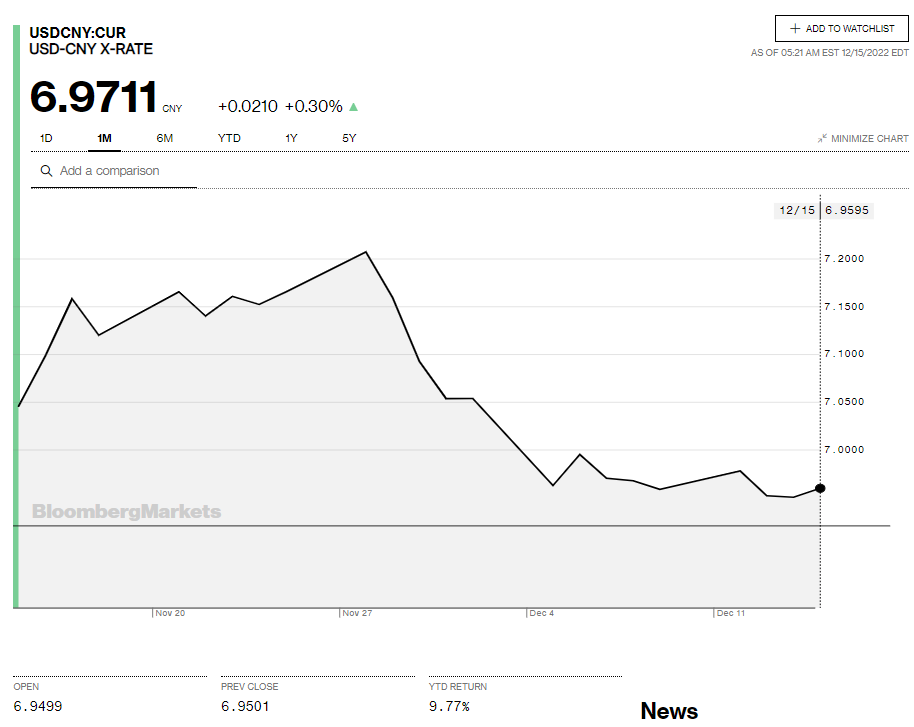

China Snapshot

Today’s Bank of China Fix: 6.9343, previous 6.9535

Shanghai Shenzhen CSI 300 fell 0.07%%% to 3951.99

China’s economic woes continue. November Retail Sales fell 5.9% (forecast -3.6%, previous -0.5%) largely due to the covid outbreak. Industrial Production fell to 2.2% from %.0% for the same reason.

Chart: USDCNY 1 month

Source: Bloomberg