Photo: Clipartmax.com

June 16, 2023

- BoJ stays the course-no changes or tweaks to policy.

- China reportedly plans new infrastructure spending.

- US dollar consolidating yesterday’s losses.

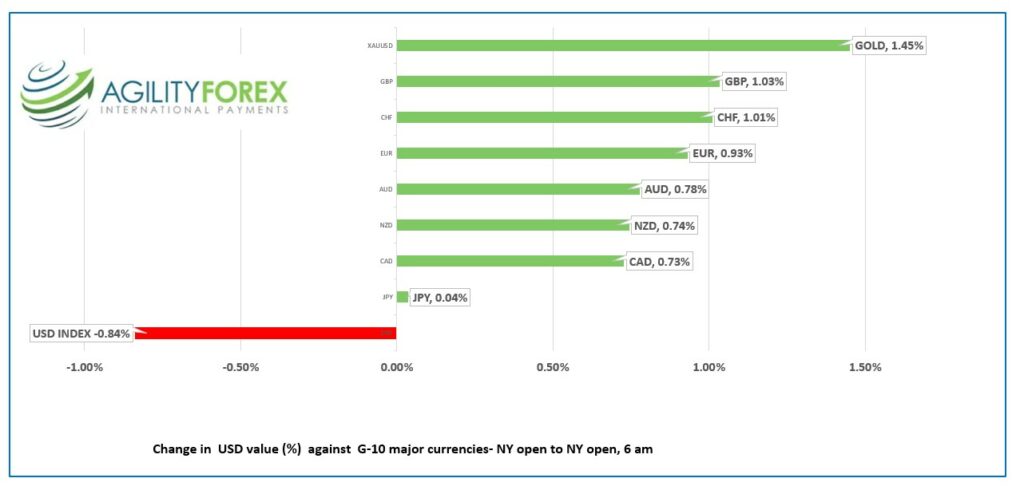

FX at a glance

Source: IFXA Ltd/

USDCAD Snapshot: open 1.3223-27, overnight range 1.3214-1.3238, close 1.3221

USDCAD traders are rushing to catch the 1.3000 express which is already inching out of the station today. USDCAD plunged from 1.3350 yesterday to 1.3212 as traders bailed out of long-dollar positions.

The Bank of Canada hiked rates on June 7 and indicated further hikes are in the pipeline due to robust data and the slow decline in inflation. The FOMC dot-plot was just as hawkish but weak US data suggested policymakers got it wrong.

WTI oil prices traded sideways in a $69.98-$70.83 range with prices supported Saudi Arabia’s unilateral production cut and by hopes the next Chinese stimulus plan boosts global demand.

USDCAD Technical Outlook

The USDCAD technicals are bearish following the decisive breach of 1.3270 support followed by the break of the 1.3220-30 support area. That sets the stage for further losses to 1.3140.

USDCAD does not have much support between 1.3210 and 1.3000 which may arrive in a hurry if speculators who are short Canada bail on their positions.(Commitment of Traders June 6 showed short CAD trades at 38,300 contracts-$3.8 billion)

The long term uptrend line at 1.2990, and psychological support at 1.3000 should halt the sell-off in the short term. If broken, it sets the stage for a test of 1.2760 ( 61.8 Fibonacci retracement of May 2021 -October 2022 range.

For today, USDCAD support is at 1.3210 and 1.3150. Resistance is at 1.3270 and 1.3320.

Today’s range 1.3150-1.3240

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The Fed has a credibility problem. The stewards of the American economy, supposedly men and women of high character embodying the virtues of integrity and unwavering moral fortitude, are not living up to the billing. Atlanta Fed President Raphael added his name to the long list of Fed officials (mostly former) who traded for their own account before an important FOMC meeting. He said he was unaware of the blackout restrictions, which raises concerns about his suitability as a Fed governor.

Fed Chair Powell’s credibility is another issue. The FOMC’s dot-plot projections suggested there would be two more rate hikes in 2023. Traders expected that when Powell talked about skipping a hike, it implied one would occur at the next meeting—in this case, July. However, Powell’s statement was ambiguous, saying, “We didn’t make a decision about July. I mean, of course, it came up in the meeting from time to time. But really, the focus was on what to do today.”

That comment contrasts sharply with ECB President Christine Lagarde’s remarks. She was discussing the decision to raise the benchmark rates by 25 basis points to 3.5% and confidently stated, “I can tell you that barring a material change to our baseline, it is very likely the case that we will continue to increase rates in July.”

The Bank of Japan’s monetary policy decision today lacked drama and excitement. Rates were left unchanged, and the statement was the usual boilerplate blather about the need to await sustainable inflation.

Yesterday’s US data was mixed. Retail Sales were better than expected, suggesting consumers are resilient, but weekly jobless claims rose. Traders focused on the jobless claims data and concluded that the Fed’s dot-plot forecast was incorrect, and only one more rate hike is likely.

The US dollar plunged, stocks soared, and the US 10-year yield dropped from 3.83% to 3.723% today.

Wall Street closed sharply higher, setting a positive tone for Asian markets. The major indices closed with strong gains. The Nikkei 225 index rose 0.66% thanks to the Bank of Japan’s inaction, while Hong Kong’s Hang Seng rose 1.07% on rumors of China stimulus.

European bourses opened with gains and gradually climbed, with the French CAC 40 index leading the way, and S&P 500 futures rise 0.20% Gold prices climbed to $1965.83 while WTI are steady at $70.87/b.

EURUSD is currently consolidating yesterday’s gains, as prices rose from a pre-ECB meeting level of 1.0804 to 1.0970 in New York today. The rally is being supported by the perceived risk of rising ECB rates, especially as the market believes the Fed’s hiking cycle is nearing completion. Eurozone inflation in May, which stood at 5.3% as expected, has not been a significant factor. The technical outlook for EURUSD remains bullish as long as prices stay above 1.0810, although momentum and Bollinger band studies suggest that the recent gains may be overdone.

GBPUSD is extending its gains from yesterday, climbing from 1.2770 in Asia to 1.2848 in New York trading. The upward movement is fueled by broad weakness in the US dollar and anticipation of a hawkish Bank of England meeting next week.

USDJPY traded erratically within a range of 139.86 and 141.40. Prices initially rallied when the Bank of Japan failed to make adjustments to the yield curve control (YCC) cap, and they were also influenced by widespread selling of the US dollar. However, prices dropped as US Treasury yields fell.

AUDUSD traded within a range of 0.6869 and 0.6898, with prices supported by expectations of further rate increases by the Reserve Bank of Australia (RBA) and rumors of potential fiscal stimulus in China.

The US Michigan Consumer Sentiment report is on the agenda, with a forecast of 60 compared to the previous reading of 59.2.

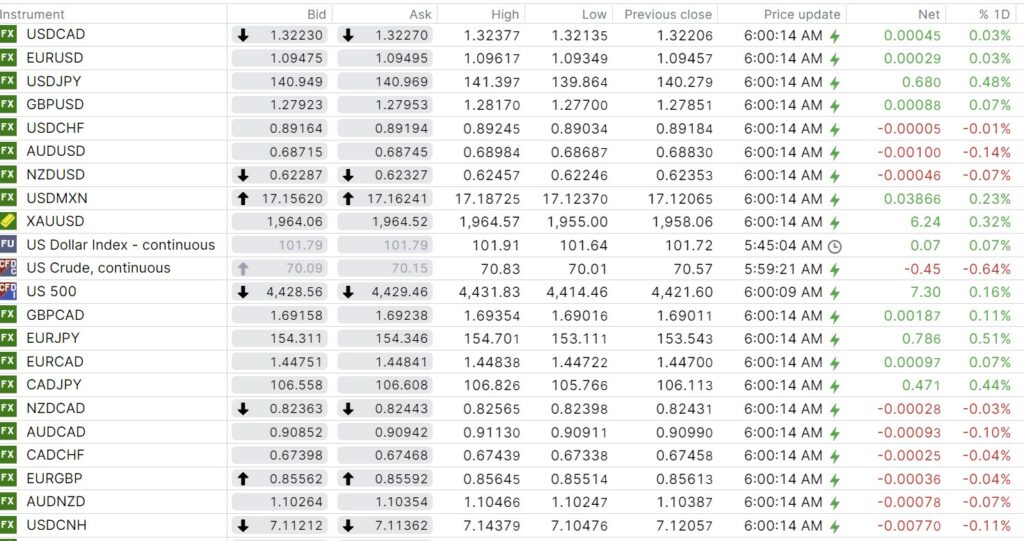

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

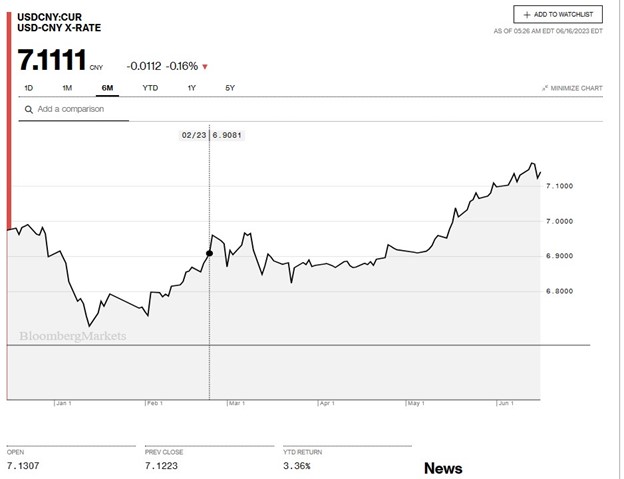

China Snapshot

Bank of China Fix: 7.1289, previous 7.1489

Shanghai Shenzhen CSI 300 rose 0.96% to 3963.35

National Development and Reform Commission (NDRC) says China will accelerate policies to increase spending.

Chart: USDCNY 6 month

Source: Bloomberg