Source: Pixabay

European equity indexes and S&P 500 futures rebounding

Fed-speak in focus this week

US dollar consolidating Friday gains, opens with an offered tone

USDCAD open 1.2423-27, Overnight range 1.2410-1.2485 Previous close 1.2468

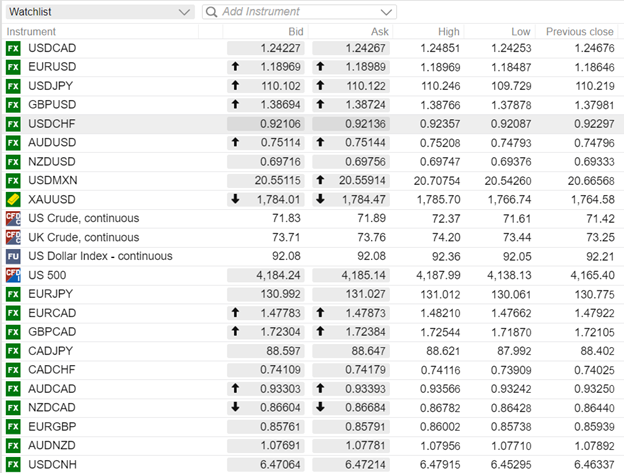

FX at a Glance

FX Recap and outlook

It’s not that Fed Chair Jerome Powell is a liar, it’s just that traders in all the markets don’t believe his view of “transitory inflation” and low interest rates for a substantial period. At the post-FOMC press conference, Powell said that the dot-plot forecast of two rate hikes in 2023 should be taken with a “big grain of salt.” Friday St Louis Fed President James Bullard spiced up the rate debate when he predicted a rate hike in 2022.

Mr Powell gets a chance for a rebuttal on Tuesday when he testifies to the Senate Coronavirus committee.

FX markets begin the week digesting the implications of the prospect of a tapering announcement as early as the Aug 26-28 Jackson Hole Fed gab-fest and sooner than expected rate hikes amidst the backdrop of global commodity price weakness, uncertain equity market sentiment.

Asia equity indexes were hammered in sympathy with Friday’s weak close on Wall Street. Japan’s Nikkei 225 dropped 3.29%, while Australia’s ASX 200 index fell 1.81%. Profit-taking lifted European stocks are into positive territory, and DJIA and S&P 500 futures are posting gains. Oil and gold prices are higher.

EURUSD chopped about in Asia. Attempts to rally were thwarted until Europe opened, and the single currency climbed from 1.1849 to 1.1899 in early NY. Germany’s Bundesbank warned that special factors such as the phasing out of a temporary vat cut could boost inflation over 4.0% y/y. The increase is expected to be “transitory.” EURUSD technicals are bearish below 1.1925 and looking for a drop to 1.1700.

GBPUSD dropped from 1.3942 in Asia on Friday to close at 1.3798 but has clawed back a good chunk of those losses overnight, rising from 1.3788 to 1.3882 in NY. UK Rightmove House Price data showed an increase of 0.8% compared to 1.8% previously, but the data was ignored. FITCH ratings increase the UK debt rating to AA-Stable, from AA-Negative.

USDJPY dropped from 110.22 at Friday’s close to 109.73 in Asia on the back of safe-haven demand for yen and JPY demand against EUR and GBP. Prices have since bounce, and USDJPY recouped all its losses as NY opened.

AUDUSD is at the top of its overnight range, rising from 0.7479 to 0.7520. Weaker than expected, May Retail Sales (actual 0.1% vs forecast 0.7%) were dismissed as a coronavirus-related decline. Australia is launching a formal WTO complaint about Chinese duties on Aussie wine.

USDCAD rallied fiercely following the Fed’s hawkish twist, rising from 1.2150 pre-Fed, to 1.2487 overnight. The dot-plot forecast of two hikes in 2023, and concerns about QE tapering beginning in September, sank commodity and equity prices, boosted risk aversion sentiment, and severely squeezed short USDCAD positions.

However, it is a USD dollar move. The Canadian dollar is collateral damage. The Bank of Canada was first off the mark in predicting an earlier than expected rate hike. Canada inflation gains are likely to mirror those of the US, so if rising inflation is worth two rate increases in the US, Canada is likely to follow suit. In addition, the global economic recovery is expected to keep oil prices at current levels, which also supports the Canadian dollar.

The economic data calendar is empty, leaving US dollar direction determined by Wall Street.

USDCAD technical outlook

The intraday USDCAD technicals snapped the steep uptrend line from June 16 with the break below 1.2460The downtrend that began in November with the move below 1.3000 is intact while prices are below the 1.2500-05 area. For today, USDCAD support is at 1.2400 and 1.2350. Resistance is at 1.2370 and 1.2520. Today’s range 1.2370–1.2460.

Chart USDCAD daily

Source: Saxo Bank

FX open, high, low, previous close

Source: Saxo Bank