Photo: The Hungry Caterpillar-Eric Carle

April 24, 2023

- Australia/New Zealand closed for Anzac Day

- German IFO Business Climate Index improves slightly.

- US dollar opens steady after narrow range trading overnight.

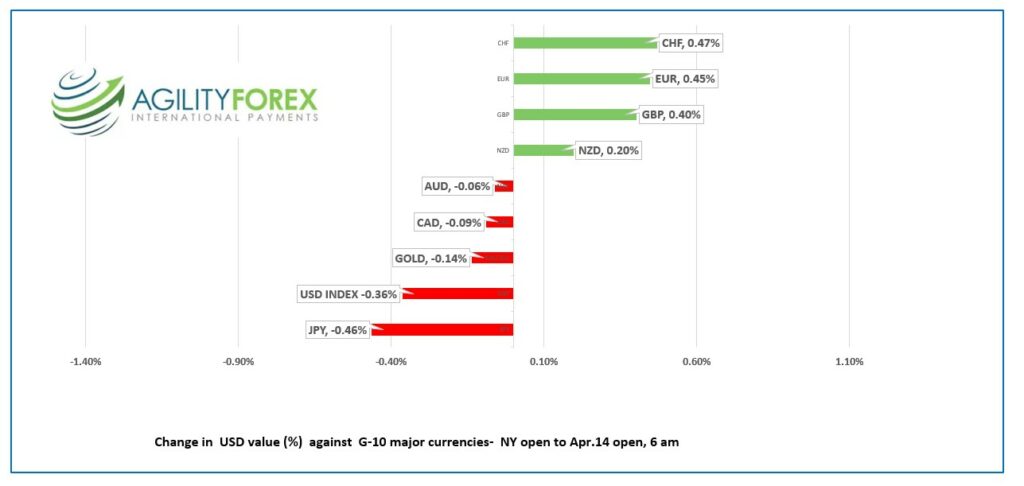

FX at a glance

Source: IFXA Ltd/RP

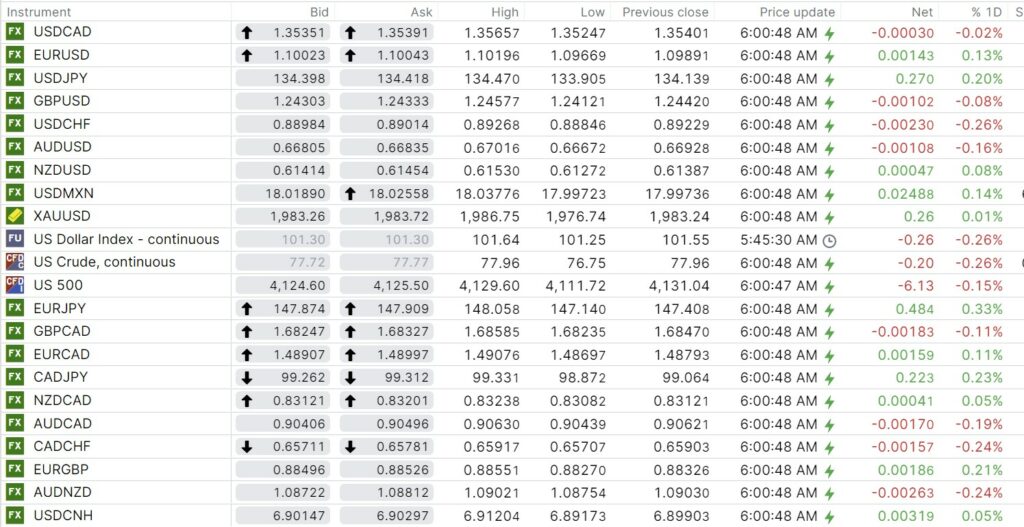

USDCAD Snapshot: open 1.3535-39, overnight range 1.3525-1.3565, close 1.3540

USDCAD traded sideways, albeit with a bit of a bid due to soft oil prices and expectations for higher US interest rates. In addition, economists are warning that domestic growth may slow if the Public service strike is prolonged. CIBC economists suggest a month-long strike could knock 0.7% off of GDP growth.

WTI oil prices slipped to $76.75/b in Asia, then rallied to $77.96/b just before NY opened. Oil is seeing selling pressure from the prospect of higher US interest rates and technical selling in an effort to “fill-the-gap” from the start of the month.

Canada February GDP data is released Friday while the Summary of Deliberations from the April 12 meeting are released on Wednesday.

USDCAD direction is at the mercy of key US data which includes Q1 GDP Thursday and PCE Price index Friday.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3510, looking for a break above 1.3570 to the test 1.3640-50 area.

The four-hour chart suggests that while USDCAD is above 1.3460, with a top-side break of the 1.3570 level extending gains to 1.3800.

The RSI and Bollinger Band indicators suggest USDCAD is extremely overbought.

For today, USDCAD support is at 1.3510 and 1.3470. Resistance is at 1.3570 and 1.3590

Today’s range 1.3490-1.3580.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

There is a lot going on, but none of it is inspiring traders. There are plenty of top-tier quarterly earnings reports later in the week, particularly from Alphabet, Microsoft, Meta, and Amazone, which will set the tone for equity markets.

Fed Governor (and voter) Lisa Cooked summed up the Fed’s dilemma in a speech in Friday. She said, “If tighter financing conditions are a significant headwind on the economy, the appropriate path of the federal funds rate may be lower than it would be in their absence. But if data show continued strength in the economy and slower disinflation, we may have more work to do.”

European equity markets are trading with a slight negative bias around unchanged, while S&P 500 futures are modestly lower. The US 10-year yield dipped from 3.572% at Friday’s close to 3.54% in early NY trading. Gold and WTI oil prices are a tad lower, as well.

EURUSD bounced from 1.0967 to 1.1020, getting a lift from German Ifo data. The Business Climate Index rose to 93.6 from 93.2, which suggests the outlook for the economy has improved, although the current situation is a tad worse. The ECB is expected to raise rates next week and have a hawkish bias.

GBPUSD is in the middle of its 1.2412-1.2458 range. GBPUSD is modestly bid following last week’s data which suggested the BoE will hike rates next month which has squeezed short-GBP positions. House prices rose a mere 0.2%, but traders were unconcerned.

USDJPY traded in a 133.91—134.47 range. The currency pair is supported by traders lowering expectations for a dovish BoJ monetary policy tweak at Friday’s meeting. Governor Kazuo Ueda may have tipped his hand when he said the BoJ must maintain monetary policy easing as trend inflation is below 2.0%.

AUDUSD traded quietly in a 0.6667-0.6702 range due to the Anzac Day holiday. Prices are supported by expectations for a 0.25% rate hike in May. Traders are looking ahead to Australian CPI data, due Wednesday.

There are no notable US economic reports today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

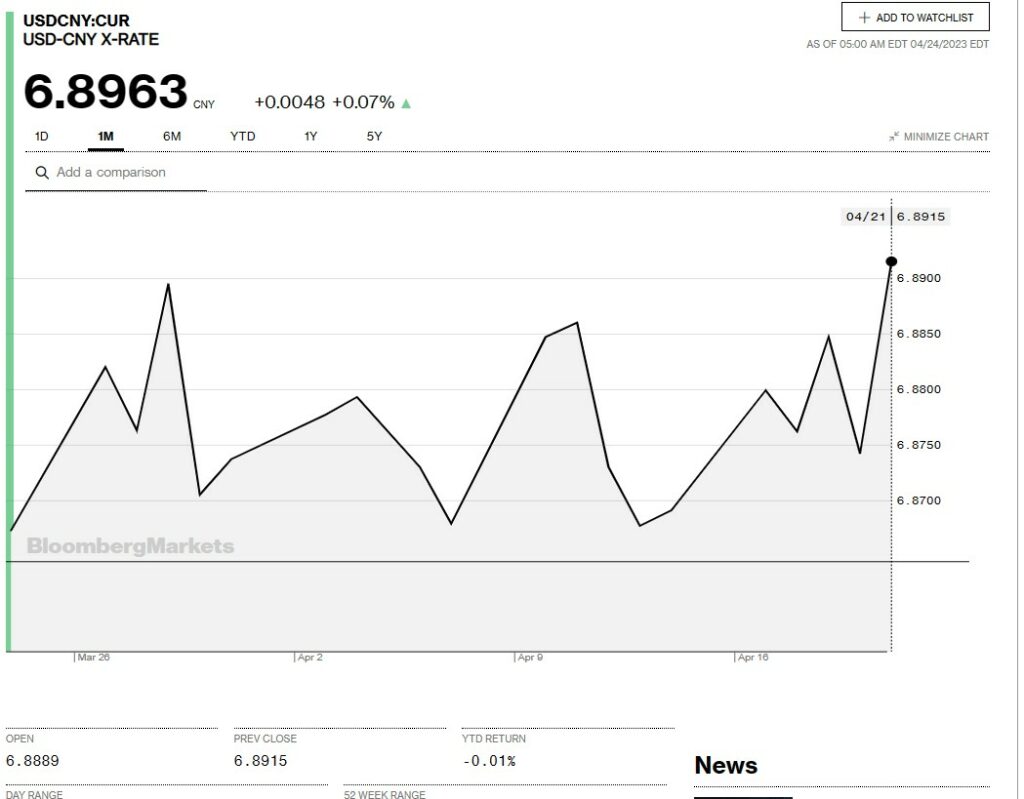

China Snapshot

Bank of China Fix: 6.8835, Previous: 6.8752

Shanghai Shenzhen CSI 300 fell 1.24% to 3982.64.

Chart: USDCNY 1 month

Source: Bloomberg