April 16, 2024

- Canada CPI rose 2.9% y/y compared to 2.8% in February-Loonie sinks

- Robust Treasury yields sinking stocks and boosting greenback.

- US dollar grinds higher overnight.

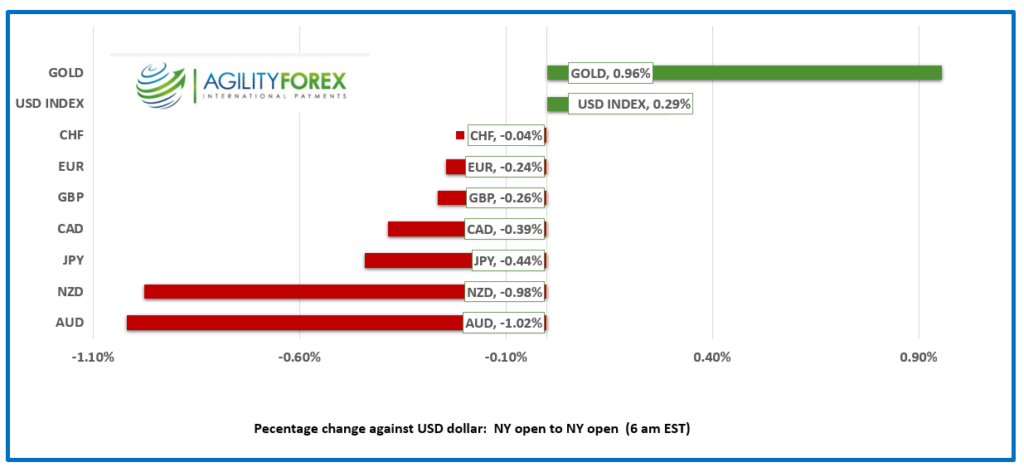

FX at a Glance

Source: IFXA/RP

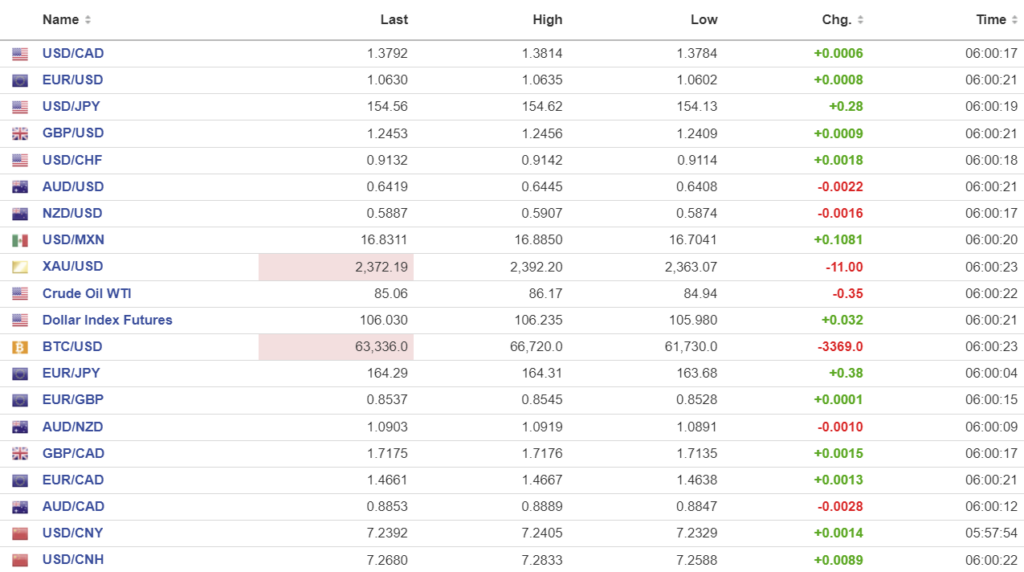

USDCAD Snapshot: open 1.3792, overnight range 1.3784-1.3823, close 1.3788.

USDCAD spiked to 1.3823 from 1.3787 on the heels of the Canadian inflation report. Statistics Canada reported that inflation rose 2.9% y/y from 2.8% in February mainly due to rising gas prices. But that’s ok, because the Bank of Canada’s CPI median metric only rose 2.8% compared to 3.1% in February.

Traders reacted like a June rate cut was now a sure thing. But is it?

The April 10 BoC statement said “While inflation is still too high and risks remain, CPI and core inflation have eased further in recent months. The Council will be looking for evidence that this downward momentum is sustained.” StatsCanada data suggests the downward momentum stalled, but the BoC data says otherwise. Which do you believe? The BoC with its admittedly inaccurate models or the Stats Canada data?

And why would the BoC feel the need to cut rates when the Federal government is on the verge of announcing a plans for massive fiscal stimulus. The Liberal budget which one pundit described as being written in “orange ink” is meant to appease NDP MP’s and keep the minority Liberal government in power.

Former Bank of Canada Governor David Dodge said “I think this is likely to be the worst budget since the Allan MacEachen budget of 1982, in the sense of pointing us in the wrong direction as to how we go about raising the incomes of Canadians and actually making Canadians feel better over the medium term.”

WTI oil prices remained steady in a 84.94-86.17 range and are sitting near the session low.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3730 and looking for a break above 1.3830 to target the 1.3850-60 area. A break below 1.3730 suggests a retest of 1.3680.

Longer term, the USDCAD uptrend line from January 1 is intact while prices are above 1.3510 and it is being guarded by previous resistance, (now support) at 1.3620. A break above 1.3860 targets 1.4000.

For today, USDCAD support is at 1.3750 and 1.3710. Resistance is at 1.3830 and 1.3860. Today’s range is 1.3760-1.3840

Chart: USDCAD daily

Source: DailyFX

Higher US interest rates equals higher US dollar.

The correlation ratio is nearly perfect. As US Treasury yields rise, so does the US dollar and that makes the US dollar the Energizer bunny of foreign exchange. The US 10-year yield has risen from 3.875% at the beginning of February to 4.65% today. The US dollar index climbed from 102.87 on February 1, to 106.07 in early NY. The Fed is in no hurry to cut rates while analysts expect the ECB and BoE to start easing as early as June.

Iran, Iran, Iran.

The angry Ayatollahs of Iran are looking rather foolish after their attack on Israel failed spectacularly thanks to the superiority of Israeli weapons and cooperation from other Arab nations. Iran is hoping to scare the Israelis from retaliating by threatening another attack with 10 times the missiles. That was enough to keep traders looking for safe havens and the US dollar was a prime destination.

Equities

Asian equity indexes followed Wall Street’s lead and closed with losses led by a 1.94% plunge in Japan’s Nikkei 225 index followed by a 1.81% drop in Australia’s ASX 200 index. European bourses are deep in the red. The German Dax and UK FTSE 100 indices are neck and neck, both falling 1.32%. S&P 500 futures are flat to slightly negative. Gold prices surged to 2,392.20 before sliding back to 2372.56 in NY.

EURUSD

EURUSD inched higher in a 1.0602-1.0654 range, but the topside may be limited by widening ECB/Fed interest rate differentials. and Fed interest rate policies. Analysts are forecasting at least 75 bps of ECB rate cuts in 2024, while the Fed may only cut once.

GBPUSD

GBPUSD climbed from 1.2409 to 1.24721 on a bit of profit taking after yesterday’s losses. The UK unemployment rate rose from 3.9% to 4.2% which was seen as evidence that high rates were having an impact on hiring.

USDJPY

USDJPY rallied from 154.13 to 154.63 in tandem with the US 10-year Treasury yield rising from 4.52% yesterday to 4.65% today. There is talk that the BoJ will intervene when USDJPY reaches 155.00 but take that with a grain of salt. Policymakers may prefer to wait until USDJPY rises high enough to trigger stop-loss buying of USDJPY to punish speculators and only intervene after the stops have been run.

AUDUSD and NZDUSD

AUDUSD traded poorly in a 0.6408-0.6445 range, extending yesterday’s losses due to a wave of risk aversion sentiment from higher US rates and Middle East tensions. A rising USDCNY is also putting pressure on AUD.

NZDUSD dropped again, falling to 0.5874 from 0.5907, which is a new 2024 low for the currency. NZDUSD is being crushed by broad US dollar strength from higher Treasury yields and China’s decision to let CNY slide.

USDMXN

USDMXN rallied hard, rising from 16.7041 to 18.8850 overnight and it has gained 3.8% since April 9. The gains are due to the strength of the latest US data which has pushed Fed rate cut hopes out to December.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1028 vs exp. 7.2475 (prev. 7.0979).

Shanghai Shenzhen CSI 300 rose 2.11% to 3549.08.

China GDP rose 5.3% y/y in Q1, while March Industrial Production rose 4.5% y/y (forecast 5.4%, previous 7.0%) and Retail Sales rose 3.1% (forecast 4.5%, previous 5.5%). The results are sketchy and likely more of an indication of Xi Jinping’s wishes, then performance.

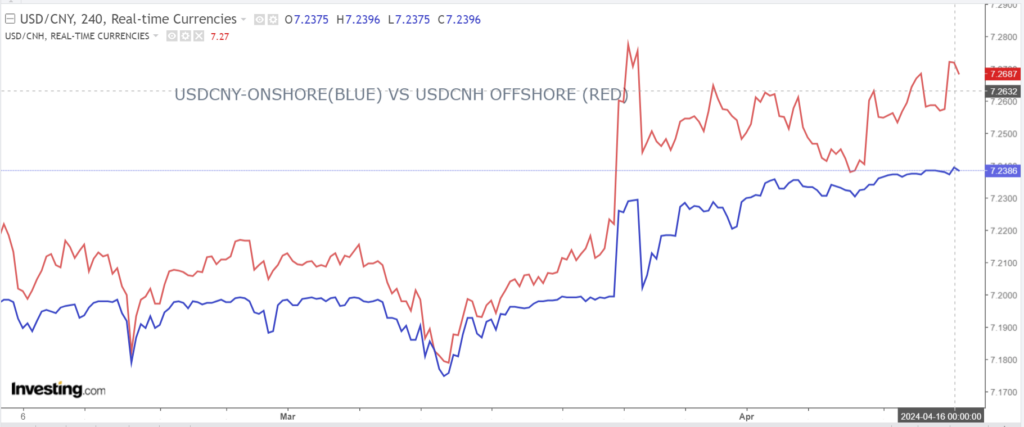

CNY is sinking steadily, and many believe it has the tacit blessing of Chinese authorities. Reuters reports that exporters expect the weakening trend to continue and are reluctant to sell dollars, for yuan, exacerbating the CNY slide.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com