Photo: Bing Image Creator

September 7, 2023

- German Industrial Prices fall 0.8% in July moving country closer to recession.

- UK August House prices tumble 4.6% y/y and 1.9% m/m

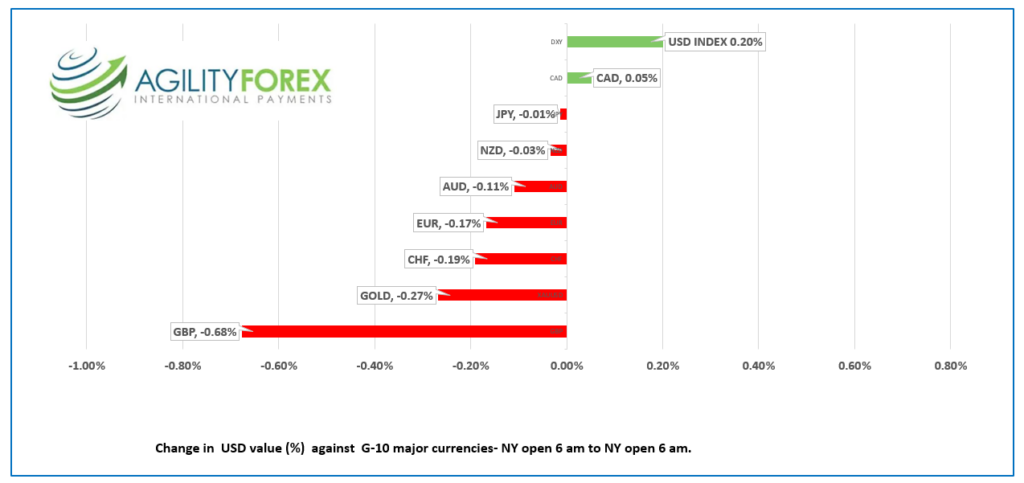

- US dollar opens with gains except against CAD.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3646-50, overnight range: 1.3632-1.3665, close 1.3635

USDCAD did not react to yesterday’s Bank of Canada interest rate decision. The BoC left interest rates on hold, which was almost a given and failed to provide much in the way of forward guidance. The statement noted that the economy is weakening but expressed unhappiness with the slow pace of the inflation decline.

USDCAD bounced inside yesterday’s range in an uneventful overnight session, with the focus on BoC Governor Tiff Macklem delivering an “Economic Progress Report” at 2:10 pm today and the Canadian unemployment report on Friday.

USDCAD gains were slowed by higher oil prices. WTI oil rallied to $88.07/b yesterday, then consolidated the gains in a $86.76-$87.75/b range overnight. Saudi and Russian production cut extensions are underpinning prices.

Today’s lower-than-expected US jobless claims data will stoke the “higher rates for longer” outlook and support USDCAD.

USDCAD Technicals

The intraday USDCAD technicals are bullish while trading above 1.3620 and looking for a break above the 1.3680-90 area to target 1.3750. A break below 1.3620 suggests further losses to 1.3560.

Longer term, the USDCAD uptrend is intact while prices are above 1.3550, looking for a decisive break above 1.3690 to target 1.4000.

For today, USDCAD support is at 1.3620 and 1.3570. Resistance is at 1.3680 and 1.3720. Today’s range 1.3620-1.3710

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Vroom, Vroom. The US dollar is the leader of the pack in overnight trading and since the start of this week. The greenback rally is being fueled by US economic outperformance measured against the major G-10 economies and by disappointing Chinese economic growth. Chinese President Xi Jinping deliberately hid Covid from the world, totally bungled his own country’s response to the pandemic, scared away foreign investment by his ham-fisted crackdown on the tech industry, while allowing property developers to drown in a sea of red ink.

US economic outperformance was on full display yesterday after the August ISM Services PMI index expanded to 54.5 rather than dip to 52.5 from July’s 52.7 level. Analysts concluded that the data was further evidence that the Fed would keep rates at elevated levels and for longer than previously expected.

The US economic outperformance view was further reinforced overnight after China’s Trade balance was weaker than expected, German Industrial Production fell, and UK Housing prices tumbled sharply. That theme was reinforced again after today’s US weekly jobless claims dropped from 229,000 last week to 216,000 today.

The major Asian equity indexes closed deep in the red, led by a 1.19% drop in Australia’s ASX 200, while the weaker yen helped hold Nikkei 225 index losses to 0.75%. European bourses are digesting weak economic data and are mixed around unchanged. S&P 500 futures are down 0.32%, and the US 10-year yield is steady at 4.276%.

EURUSD is trading with a negative bias and is at the bottom of its 1.0688-1.0732 range following today’s US data. More weak data from Germany and the Eurozone is also weighing on prices. Q2 GDP was 0.5% (forecast 0.6% y/y), while Eurozone employment only rose 1.3% (forecast 1.5%). German Industrial Production disappointed (actual -0.8% m/m in July vs. forecast -0.5%), which also weighed on prices.

GBPUSD is sinking in a 1.2447-1.2511 range, with prices suffering from the drop in the Halifax House Price index to a 14-year low and widespread US dollar demand.

USDJPY bounced around in a 147.22-147.88 range with demand from higher US Treasury yields offset by yesterday’s verbal intervention from policymakers.

AUDUSD traded in a 0.6362-0.6393 range. Prices got a bit of a lift following news that Prime Minister Anthony Albanese chatted with Chinese President Xi Jinping in Jakarta. Outgoing RBA Governor Phillip Lowe’s last speech was more of a whine about how he was treated in the press than it was about monetary policy.

Philadelphia Fed President Patrick Harker, Chicago Fed President Austan Goolsbee, and NY Fed boss John Williams are speaking today.

Top of Form

FX high, low, open

Source: Investing.com

China Snapshot

Bank of China Fix: today 7.1986, expected 7.3121, previous 7.1969.

Shanghai Shenzhen CSI 300 fell 1.40% to 3758.47.

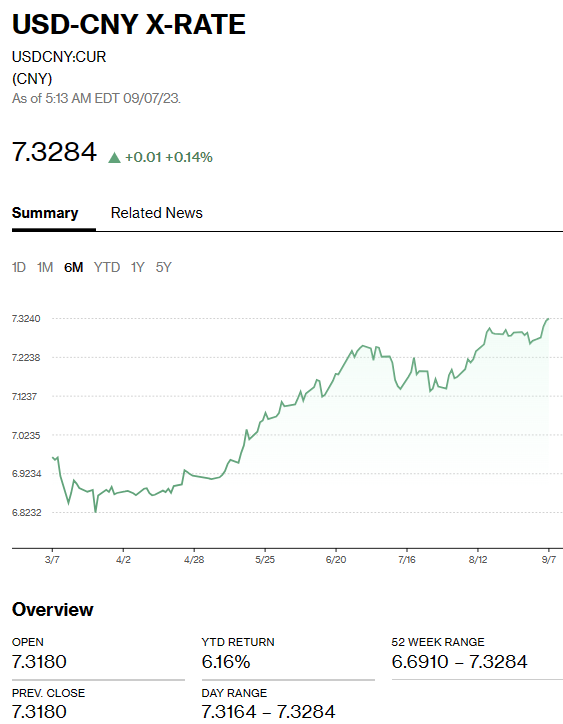

USDCNY is trading at levels last seen in 2008 as the currency pays the price for Xi Jinping’s economic mismanagement.

China August Trade surplus falls to $68.36 billion (forecast $73.9 bio, July $80.68 bio.).

Exports -8.8% y/y (forecast -9.5%, July -14.5%) Imports -7.3% (forecast -9.4%, July-12.4%)

Chart: USDCNY 1 month

Source: Bloomberg