August 20, 2024

- Bank of Canada Core-CPI rises 1.7% y/y (June 1.9%)

- Oil slides on ceasefire chatter.

- US dollar reeling as dovish Fed talk heats up.

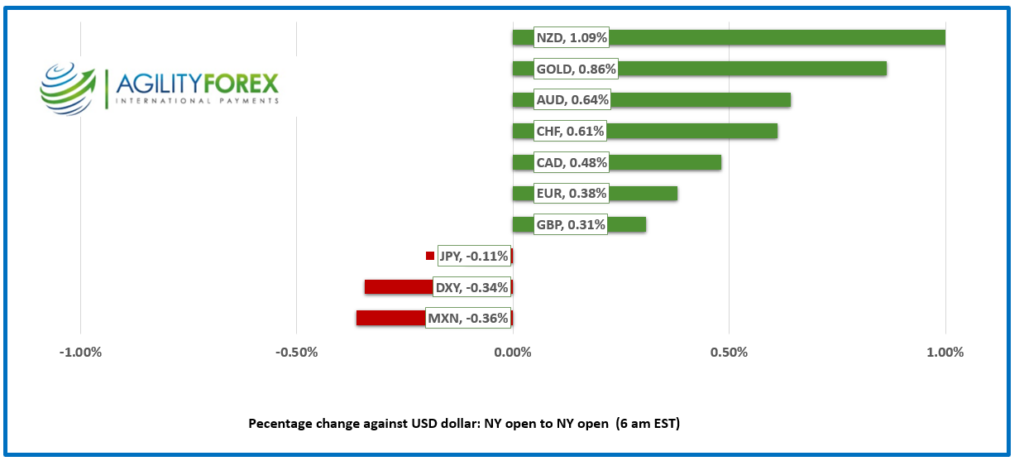

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3615, overnight range 1.3605-1.3642, previous close 1.3633

USDCAD is trading lower as the greenback comes under pressure worldwide, with traders embracing hopes that the Fed will cut rates faster and deeper. However, the sell-off is looking overdone, at least for USDCAD.

The CAD/US 10-year interest rate spread is 80.9 basis points in favor of the US. It has been as wide as 96.2 on June 9 and as narrow as 44.3 in October 2023. The Bank of Canada is already expected to cut rates three times before year-end, and three Fed rate cuts are priced in as well. So, there’s not much support from narrowing spreads in the near term.

Canada is facing a nationwide rail strike, which, if it occurs on Thursday, risks massive supply chain disruptions, backlogs, and higher prices. Hardly a recipe for economic growth.

Oil prices are falling, with WTI trading in a 72.96-73.97 range overnight on talk that Hamas terrorists and Israel will agree to a US-brokered ceasefire. If so, the risk of a supply disruption from the Middle East abates, and the focus shifts to slowing Chinese crude demand, even as OPEC ramps up production.

The Bank of Canada’s measure of Core inflation rose just 1.7% m/m which is below the 1.9% seen in June and guaranteeing a 25 bps rate cut in September. USDCAD ticked higher as the results were not a surprise and a rate cut is already baked into the price.

The US economic calendar is empty.

USDCAD technicals

The intraday USDCAD technicals are bearish below 1.3660 and looking for a test of support in the 1.3590-1.3600 area. If broken it will extend losses to 1.3550, levels last seen in April.

Longer term, USDCAD appears oversold. Bollinger bands are approaching 3 standard deviations and the RSI is extremely oversold. In addition, there is support from the 1.3590 200 day moving average.

For today, USDCAD support is at 1.3590 and 1.3560. Resistance is at 1.3660 and 1.3690. Today’s Range 1.3590-1.3660

Chart: USDCAD daily

Source: DailyFX

“I’m Melting”

Those were the last words of the Wicked Witch of the East in The Wizard of Oz, and they are being echoed by the US dollar. The US Dollar Index (DXY) has fallen 3.8% since July 1 due to increased speculation of faster and deeper Fed rate cuts. Analysts are getting themselves into a lather ahead of Fed Chair Jerome Powell’s Jackson Hole speech. Many are convinced he will announce a major policy shift that raises the odds for a 50 bps rate cut on September 18. Equity traders are on board and have boosted the S&P 500 to its eighth consecutive gain. We’ve seen this movie before. All it would take is one disappointing data point, or an errant missile in the Middle East or Russia, and the rally will become a rout.

EURUSD

EURUSD traded firmer in a 1.1072-1.1089 range due to widespread US dollar selling and renewed hopes for dovish remarks from Fed Chair Powell. The Eurozone HICP inflation data for July was as expected and a non-event, as was the German Producer Prices data. Sweden’s Riksbank cut its benchmark rate by 25 bps to 3.5% and hinted at three further rate cuts this year.

GBPUSD

GBPUSD continued to rally, rising from 1.2974 to 1.3013, with traders looking for a test of the 1.3034, 2024 peak. The gains were all due to US dollar weakness. GBPUSD continues to benefit from last week’s better-than-expected GDP numbers and falling unemployment rate, which lessened the need for the Bank of England tocut interest rates in the near term. A break above 1.3050 targets the 2023 peak of 1.3140.

USDJPY

USDJPY bopped and weaved in a 145.84-147.35 range in Asia, then drifted down from the peak to 146.44 by the NY open. Ongoing chatter about carry-trade unwinding and hopes of a dovish policy announcement from Powell this week are roiling markets. USDJPY experienced volatility, with prices rising to 148.05 at the Asia open before plunging to 145.19 just before Europe opened. Prices have since rallied to 146.41 in New York. The outlook for higher Japanese and lower U.S. interest rates, combined with intervention fears and carry trade unwinding, is roiling markets.

AUDUSD and NZDUSD

AUDUSD drifted higher on the back of broad US dollar weakness, rising from 0.6714 to 0.6729. The RBA minutes did not offer anything new. The board considered hiking rates and thinks rates need to remain elevated for an extended period. That’s basically what Governor Michele Bullock has been telling audiences since the meeting.

NZDUSD traded higher in a 0.6108-0.6141 range. New Zealand’s trade deficit narrowed to $9.29 billion from $9.5 billion, but it wasn’t a factor for FX markets.

USDMXN

USDMXN rallied to 18.8398 yesterday and then consolidated the gains in an 18.6562-18.7537 range overnight. Prices are supported by speculation that the popular MXN/everything else carry trade is being unwound. Sure, some positions are being cut, but Banxico’s benchmark rate of 10.75% is substantially higher than that of any G-10 country, so it is hard to believe that the carry trade is dead and buried. Mexican Retail Sales disappointed, falling 3.9% y/y compared to tthe forecast for a 1.8% decline.

Bitcoin (BTCUSD)

BTCUSD caught a bid and climbed from 57,936 to 61,472 before sliding to 60,950 in early NY. Cryptocurrency traders are hoping for dovish remarks from Powell this week. A failure to break above 62,000 risks a retest of 55,000.

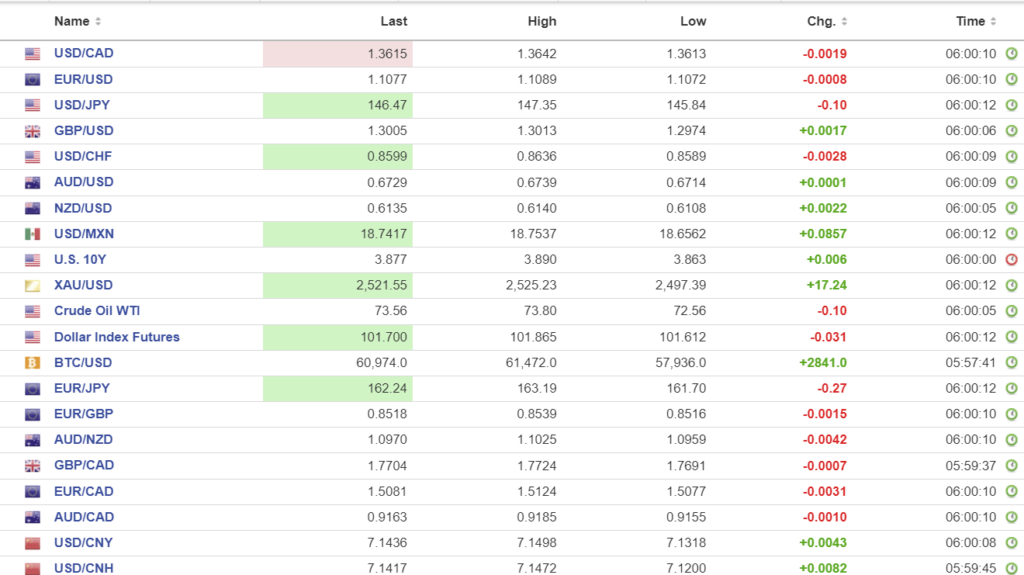

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1325 vs exp. 7.1317 (prev. 7.1415).

Shanghai Shenzhen CSI 300 fell 0.72% to 3332.70

PBoC leaves 1-year and 5-year Loan Prime Rate unchanged at 3.35% and 3.85% respectively.

China allows some developers to slash housing prices on unsold inventory. Bloomberg reports that at least 10 cities have relaxed or scrapped ne-home price guidance.

Chart: USDCNY and USDCNH

Source: Investing.com