Photo: Bing Image Creator

November 6, 2023

- RBA meets tomorrow-50/500 chance for hike.

- US data calendar is empty.

- US dollar remains on the defensive, GBP outperforms.

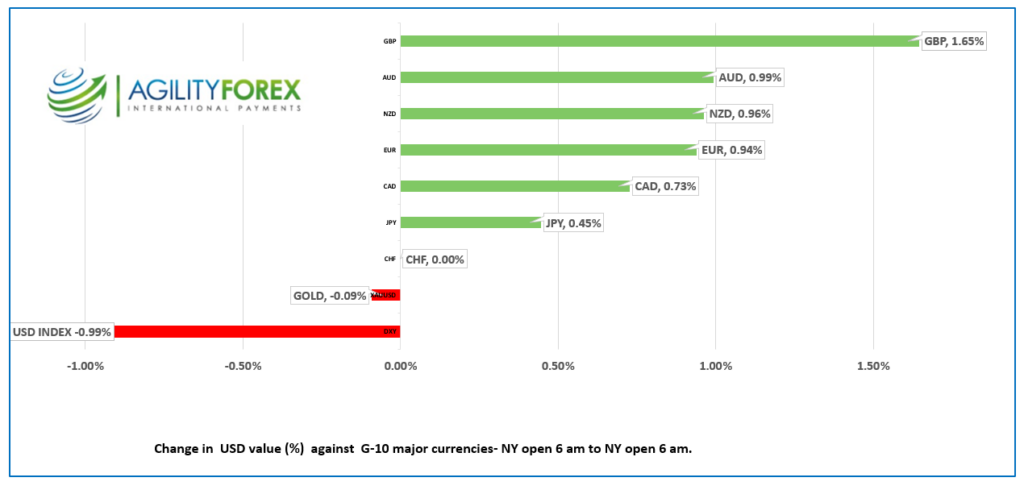

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3641-45, overnight range 1.3629-1.3667, close 1.3658

Are you feeling rested? An extra hours sleep does that. USDCAD is also feeling rested after freefalling from 1.3761 to 1.3662 on Friday. It drifted lower overnight, and traders are looking for fresh incentives to trade.

Arguably, the USDCAD drop was more of a correction than a trend change. The CAD-US 10-year yield spread is close to its widest level of the year at -81.7 bps and oil prices are close to September lows. WTI traded in a $80.67-$82.11/b range despite the risk of the Israel/Hamas war expanding to include Iran. Last week’s August GDP showed economic growth was stagnant and raised fears that Canada is heading into a recession.

The USDCAD decline is a US dollar story, and that tale is still being written. The Ivey PMI data is on tap today.

USDCAD Technicals:

The hourly and four hour USDCAD technicals are bearish following the break below the October uptrend line at 1.3720 and prices are in a downtrend while trading below 1.3660 (hourly) and 1.3710 (4hour) and looking for a break below 1.3610 to target 1.3560.

Longer term, USDCAD daily technicals are bullish with the July 17 uptrend line intact above while prices are above the 1.3540-60 area. A move below 1.3540 would negate the uptrend and suggest a retest of 1.3250.

For today, USDCAD support at 1.3610 and 1.3580. Resistance at 1.3680 and 1.3710. Today’s expected trading range is 1.3610-1.3710

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The greenback is on the ropes, and beleaguered US dollar bulls need to ask themselves, in their best Dirty Harry voice, “Do I feel lucky? Well, do ya, punk?”

It is a good question. Was last week’s US dollar sell-off a correction or a trend change? Those betting on a trend change point to last Wednesday’s FOMC meeting. That’s when Fed Chair Jerome Powell suggested that higher Treasury yields reduced the need for higher rates. Traders also pointed to the lower than expected Treasury refunding announcement. Then Friday’s nonfarm payrolls data was below the consensus, and the September numbers were revised lower. Dollar sellers are convinced the Fed’s tightening cycle is not only over but that the first rate cut will occur as soon as the May 1, 2024, meeting.

Those looking to buy US dollars on dips do not believe the Fed will be cutting rates any time soon and that the Fed hasn’t changed its tune about keeping rates high for longer. As Bloomberg’s John Authors points out, US unemployment is at 3.9%, which is a historically low level. In addition, when the Fed hinted that high yields might preclude a rate hike, the US 10-year Treasury yield was above 4.90%. It is 4.59% this morning.

The most compelling argument to suggest that the recent US dollar weakness is merely a correction is the IMM positioning data. Traders went into the FOMC meeting long dollars, and the recent FX action suggests those positions were being cut aggressively.

The ongoing strife in Ukraine and Gaza should provide some safe-haven support for the US dollar, although recent price action suggests traders are ignoring those risks.

Asian equity indexes followed Wall Street’s lead and closed with strong gains, led by a 2.37% surge in Japan’s Nikkei 225 index. The Australian ASX 200 underperformed and only rose 0.24%. European equity indexes opened flat then traded lower, with the German DAX falling 0.22%. S&P 500 futures are up a mere 0.18%.

EURUSD consolidated last week’s gains in a 1.0722-1.0756 range due to a short squeeze as stop losses were triggered on the break above 1.0660 on Friday. German and US 10-year yield spreads narrowed from -210 bps on October 31 to -191.0 today, which supported the move, but also suggest the gains are not sustainable. Eurozone data was mildly EURUSD positive as German factory orders were a tad better than expected, while Eurozone Services PMI was as forecast. The intraday EURUSD technicals are bullish above 1.0620, looking for a break above 1.0770 to extend gains to 1.0840.

GBPUSD is at the top of its 1.2365-1.2424 range, with the gains occurring on the back of the broadly bearish US dollar sentiment and the unwinding of stretched short-GBPUSD positions. Traders ignored the UK Construction PMI, which was 45.6 in October (September 45.0) but also the second-lowest reading since May 2020. The GBPUSD downtrend from July was snapped with the move above 1.2240. A break above 1.2440 targets 1.2560.

USDJPY was steady in a 147.32-147.74 range, with prices weighed down by soft US Treasury yields. Bank of Japan Governor Kazuo Ueda suggested it would be unlikely that they would have enough data to end negative rates this year.

AUDUSD traded with a bid in a 0.6503-0.6524 range, with Aussie traders focused on Tuesday’s Reserve Bank of Australia (RBA) meeting. The odds are evenly split as to whether an RBA rate hike will occur or not. Those believing a hike is likely point to recent stronger than expected data (CPI, Retail Sales), while those believing rates will remain unchanged point to the somewhat dovish Fed outlook.

The US data calendar is empty.

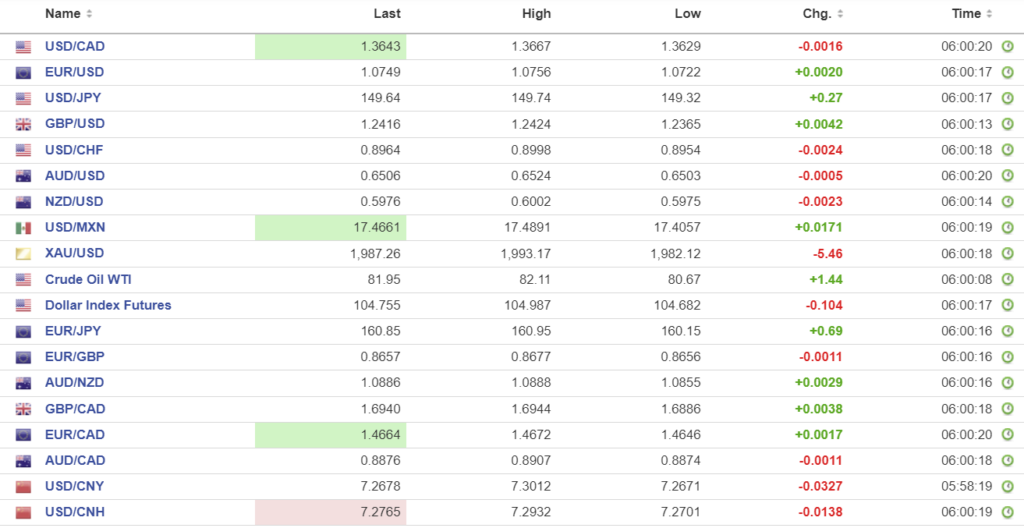

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1780, expected 7.2868, previous 7.1796.

Shanghai Shenzhen CSI 300 rose 1.35% to 3632.61.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com