Photo: HDClipartAll.com

January 4, 2023

- FOMC minutes released this afternoon

- China making nice with Australia

- US dollar gives back yesterday’s gains

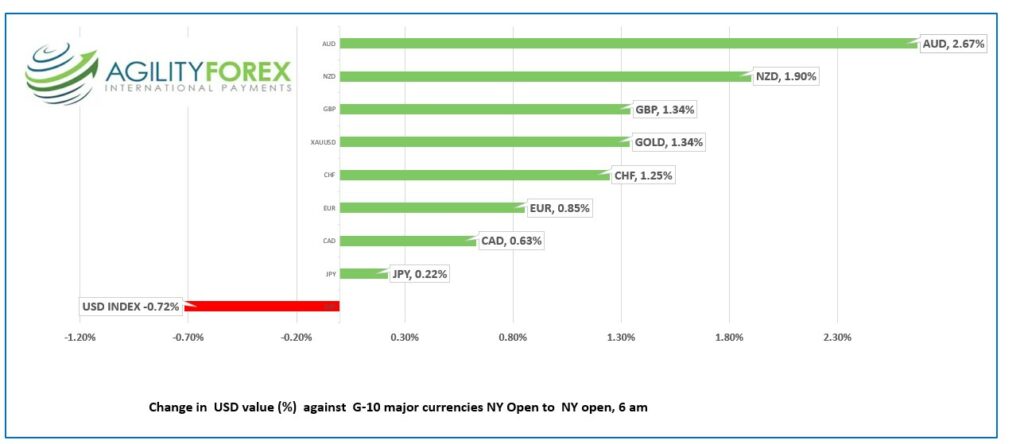

FX at a glance

Source: IFXA Ltd/RP

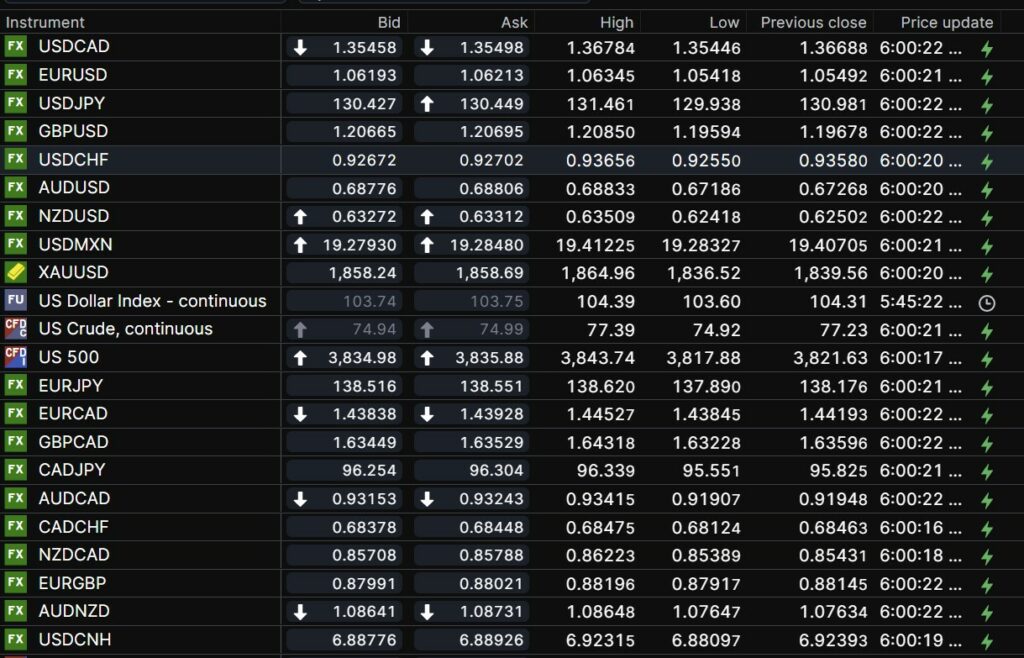

USDCAD Snapshot: open 1.3546-50, overnight range 1.3527-1.3678, close 1.3669

USDCAD gave back nearly all of yesterday’s gains overnight and added to them in early NY trading. That was primarily due to a steep rebound in the antipodean currencies after China appeared to discuss resuming imports of Australian coal.

USDCAD continues to track broad US dollar moves but downside losses may be contained by the prospect of divergent Bank of Canada and Fed monetary policy. BoC Governor Tiff Macklem hinted that he is close to hitting the brakes on rate hikes, while Fed Chair Powell merely downshifted from third to second gear.

Oil prices are struggling to maintain upward momentum despite Russian sanctions, and Opec production cuts. WTI fell from $81.46/barrel yesterday to $74.90/b in early NY due to covid fears in China. Beijing lifted its strict coronavirus protocols in late December just as another massive outbreak is occurring. Official estimates suggest there are 4,000 new cases per day, but some scientists suggest its more like 1 million /day.

USDCAD direction will be determined by S&P 500 price action.

USDCAD technical outlook.

The intraday technicals flipped to bearish with yesterday’s failure to break above the downtrend resistance line at 1.3680. Further losses below 1.3540 will target 1.3480 then 1.3440.

Fibonacci retracement projections of the August-December range suggest that a break below 1.3405 will extend losses to the 50% Fibonacci level of 1.3235.

For today, USDCAD support is at 1.3510 and 1.3470. Resistance is at 1.3590 and 1.3660

Today’s range 1.3490-1.3580

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar rallied hard yesterday and then gave back most, if not all, its gains overnight. There was no specific catalyst for either the rally or the retreat.

The release of the FOMC minutes from December 14 will reignite the debate about the level of the Fed’s terminal rate and whether the Committee is as hawkish as what Chair Powell’s press conference suggested.

Asian equity traders ignored the weak close on Wall Street and bought stocks. Australia’s ASX 200 index finished with a 1.63% gain, thanks to surging gold prices. Hong Kong’s Hang Seng Index soared 3.22% on rumours of more support for property developers.

European bourses climbed steadily with the German Dax gaining 1.64% helped by improving Eurozone Services PMI data. S&P 500 futures have gained 0.63% underpinned by the slide in the US 10-year Treasury yield from 3.754% at yesterdays close to 3.673% today.

EURUSD climbed steadily overnight, rising from 1.0542 to 1.0635 in Europe after Eurozone and German Services PMI data was better than expected. The signs that economic weakness was dissipating combined with yesterday’s lower than expected German inflation report underpinned prices. The EURUSD technicals are bullish above 1.0500 and looking for a break above 1.0700 to extend gains to 1.0810.

GBPUSD followed EURUSD higher, rising from 1.1959 to 1.2086. The poor outlook for the UK economy combined with bearish technicals while prices are below 1.2340 suggest the latest rally is merely a correction.

USDJPY peaked at 131.46 in Asia then dropped steadily to 129.94 in Europe before bouncing to 130.38 in NY. Prices are undermined by the drop in the US 10-year Treasury yield and rising expectations that the BoJ will end its ultra-low monetary policy in the coming months. BoJ Governor Kuroda contradicted that view. He said the BoJ will continue monetary easing to achieve price targets.

AUDUSD saw a coal-fueled rally, jumping to 0.6885 from 0.6719 after Bloomberg reported Chinese bureaucrats were discussing plans to resume some imports of Australian coal. President Xi Jinping banned imports of Aussie coal two-years ago after Australia demanded an inquiry into the coronavirus.

Today’s US data includes JOLTS job openings, ISM Manufacturing PMI and the FOMC meeting minutes.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

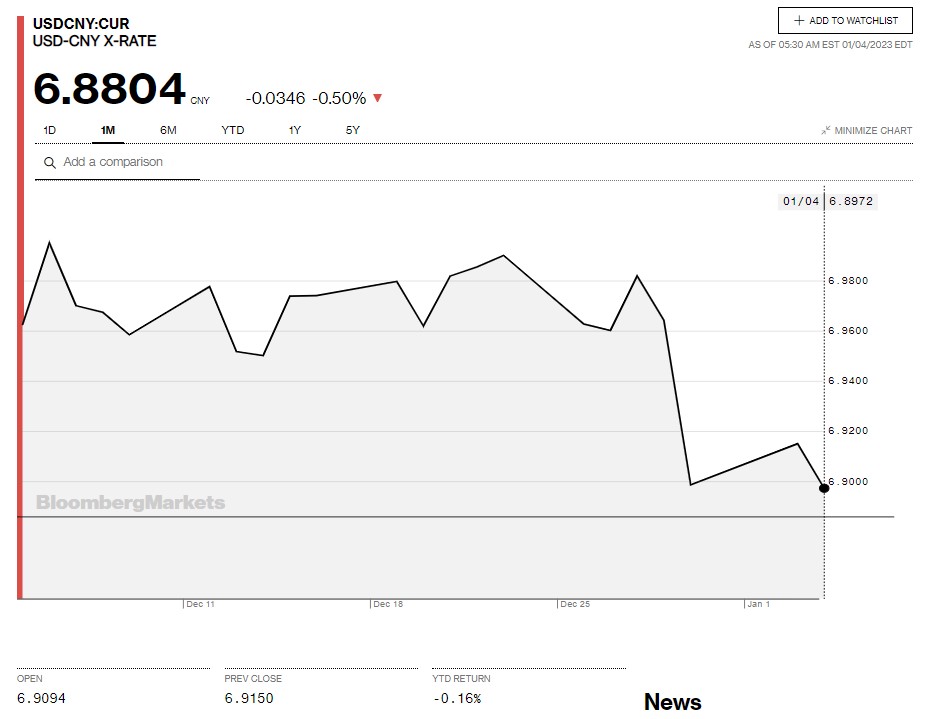

China Snapshot

Today’s Bank of China Fix: 6.9131, previous 6.9475

Shanghai Shenzhen CSI 300 rose 0.13% to 3892.95

China may be planning another $145 billion in industry incentives as well as more support for big developers.

Chart: USDCNY one month

Source: Bloomberg