April 26, 2024

- US Core PCE Price index unchanged, but above expectations.

- Yen tanks after dovish BoJ meeting.

- US dollar trades looking for direction following PCE data.

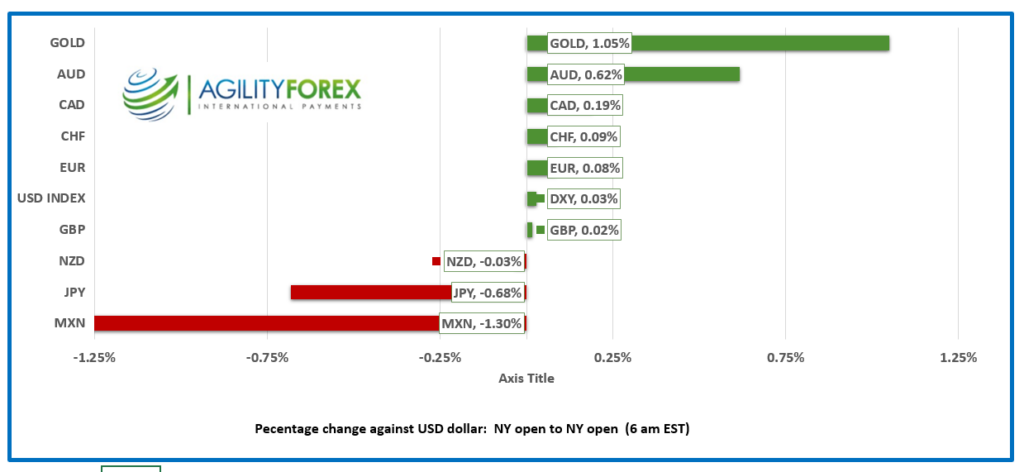

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3657, overnight range 1.3636-1.3663 close 1.3659.

USDCAD dropped to test support in the 1.3640 area which held but the subsequent bounce is of the dead-cat variety. USDCAD is being weighed down by improved risk sentiment stemming from a surge in equities, led by impressive earnings from the likes of Alphabet and Microsoft. But those are American companies. They may be global in scope, but they are benefitting from the resilience of the US economy and consumer.

Canada’s economy is a slug compared to the US and the federal government is fiscally challenged. The Federal and Ontario governments have committed over $33.billion to foreign -owned auto manufacturers to build EV battery and car plants in Ontario and Quebec that at the moment, no one wants. Ford’s EV unit just announced a Q1 loss of $1.3 billion or US$ 132,000 per car sold.

Meanwhile Canada is sitting 168 billion barrels of proven oil reserves worth US $14.12 trillion (WTI 84.00 )and the government wants to leave it untapped because China, India, Russia and Indonesia are pumping Co2into the atmosphere. With that kind of leadership, why would anyone want to sell USDCAD?

USDCAD dipped, post PCE Price index but the drop was not impressive, and traders appear reluctant to push prices lower.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3690, looking for a decisive breech of 1.3640 to extend losses to 1.3550. A move above 1.3610 shifts the focus to 1.3800.

USDCAD is in a descending channel on a 4 hour and daily chart, bound by 1.3700 at the top and 1.3590 at the bottom.

For today, USDCAD support is at 1.3640 and 1.3590. Resistance is at 1.3720 and 1.3760. Today’s range is 1.3610-1.3710.

Chart: USDCAD 4 hour

Source: Investing.com

I am Google, Hear me Roar

Alphabet, parent company of Google, saw its market cap top $2 trillion in after-hours trading today. It took the company 21 years to reach a valuation of $1.0 trillion and just 4 years to reach $2.0 trillion, a rather impressive (but useless) fact. And in keeping with the theme of useless facts, Venezuela has hired Rothschild & Co to help it restructure its $154 billion of defaulted debt. Now, if NDP Leader Jagmeet (make the rich pay) Singh was CEO of Alphabet, would he offer to donate just 2 quarters of earnings to erase Venezuela’s bond debt? Alphabet earned $80 billion in Q1 2024. He wouldn’t, because as a shareholder, it would be his money.

Those results helped boost global equity indexes overnight with S&P 500 futures up 0.70% as of 7:00 am EDT.

Inflation time-bomb is ticking.

There wasn’t any drama following today’s PCE Price index data. Headline PCE rose 2.7%, unchanged from February but higher than expected (forecast 2.6%). Core PCE rose 2.8% (forecast 2.6% and it was also unchanged. The results did not change the outlook for the Fed. Rate cuts will not occur until lates 2024. Equity traders were unfazed. S&P 500 futures extended overnight gains and are up 1.05% (as of 8:40 am EDT). US 10-year Treasury yields inched down to 4.665% from 4.686% where they started the day.

The US dollar is on the defensive, but the selling pressure may not last. The Fed is in no hurry to cut rates while other central bankers could start cutting as early as June. At some point equity traders will wake up to the reality of high yielding bonds having “no-risk” while equities are merely a Middle Eastern missile or a Chinese invasion of Taiwan from a collapse.

EURUSD

EURUSD inched up to 1.0753 from 1.0718 due to improving Eurozone data recently and because the ECB/Fed rate divergence story is stale and barely budged after today’s US data. The EURUSD technicals are bullish above 1.0710, looking for a break above 1.0760 to extend gains to 1.0820. A break below 1.0710 puts 1.0600 in play.

GBPUSD

GBPUSD is little changed after PCE and is in the middle of its 1.2494-1.2541 range after recouping its post-US data losses on Thursday. Traders are mulling over recent comments from Bank of England officials that suggest rate cuts are not “slam dunks” and that UK rates could remain elevated for longer. The hourly GBPUSD technicals are bullish above 1.2480, looking for a break above 1.2550 to extend gains to 1.2710.

USDJPY

USDJPY had a topsy-turvy few minutes around the BoJ meeting. USDJPY plunged from 156.82 to 155.00, then rallied steadily reaching 156.93 in NY, post PCE. The BoJ left its benchmark interest rates unchanged at 0.0-0.1%. The BoJ’s quarterly report showed policymakers expect inflation to tick higher, but Japanese GDP was downgraded to 0.8% from 1.2% for 2024. Traders were unimpressed with the continuation of JGP purchases and Governor Ueda’s tame comments on the yen. Higher US Treasury yields fueled the USDJPY rise.

AUDUSD and NZDUSD

AUDUSD rallied from 0.6517 to 0.6554 on the back of higher than expected Q1 PPI (actual 4.3% y/y vs previous 4.1%) which more than offset soft import export price data. The data reduces the odds of an RBA rate cut. NZDUSD tracked AUDUSD and rose from 0.5940 to 0.5969.

USDMXN

USDMXN climbed to 17.2820 from 17.1630 in the wake of rising US interest rates. The surge in the 10-year Treasury yield from 4.619% to 4.739% fueled the rally.

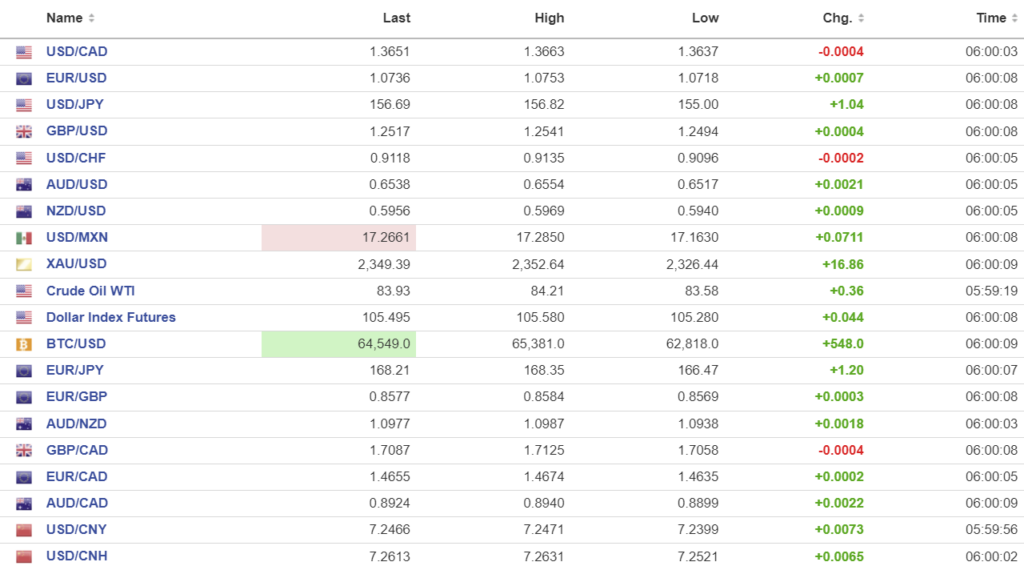

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

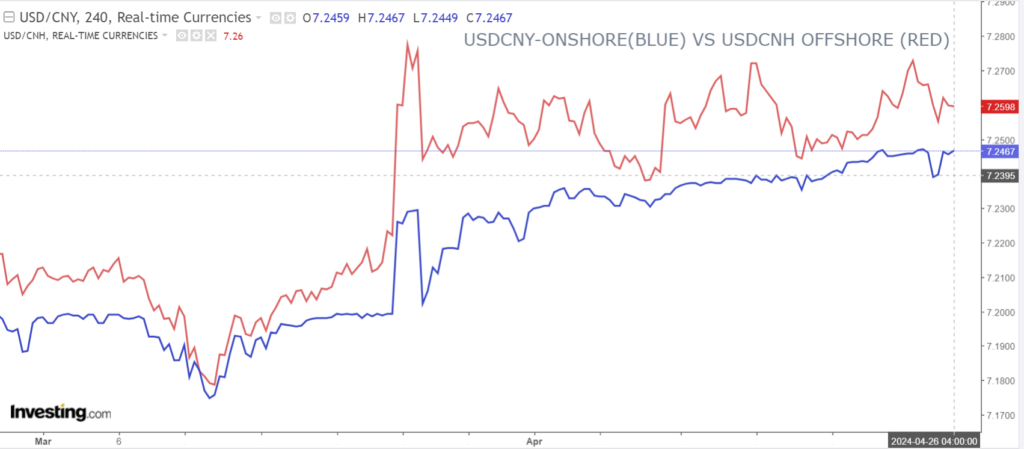

China Snapshot

PBoC fix: 7.1056 forecast 7.2449, (prev. 7.1058).

Shanghai Shenzhen CSI 300 rose 1.53% to 3584.37.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com