Photo: ClipartLibrary.com

- Fedspeak predicts sharply higher interest rates

- China’s trade surplus widens

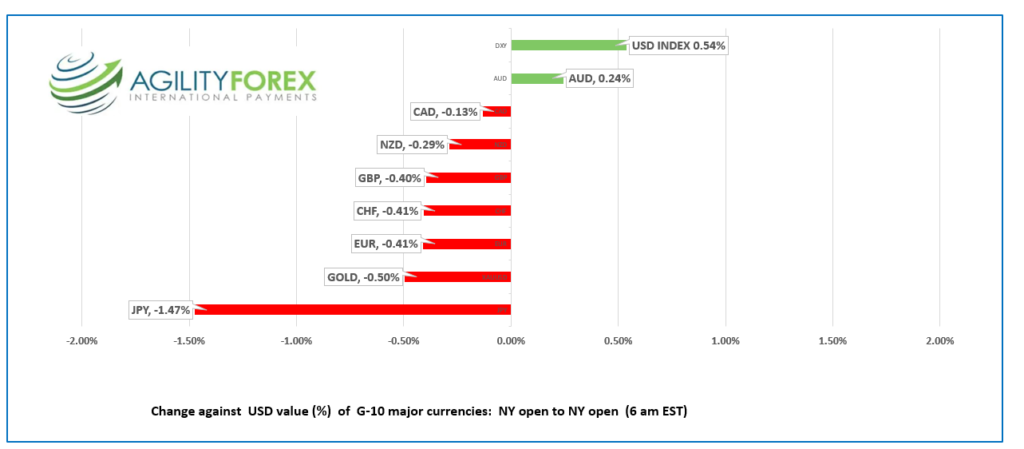

- US dollar opens firm, AUD outperforms

FX at a glance:

Source: IFXA Ltd/RP

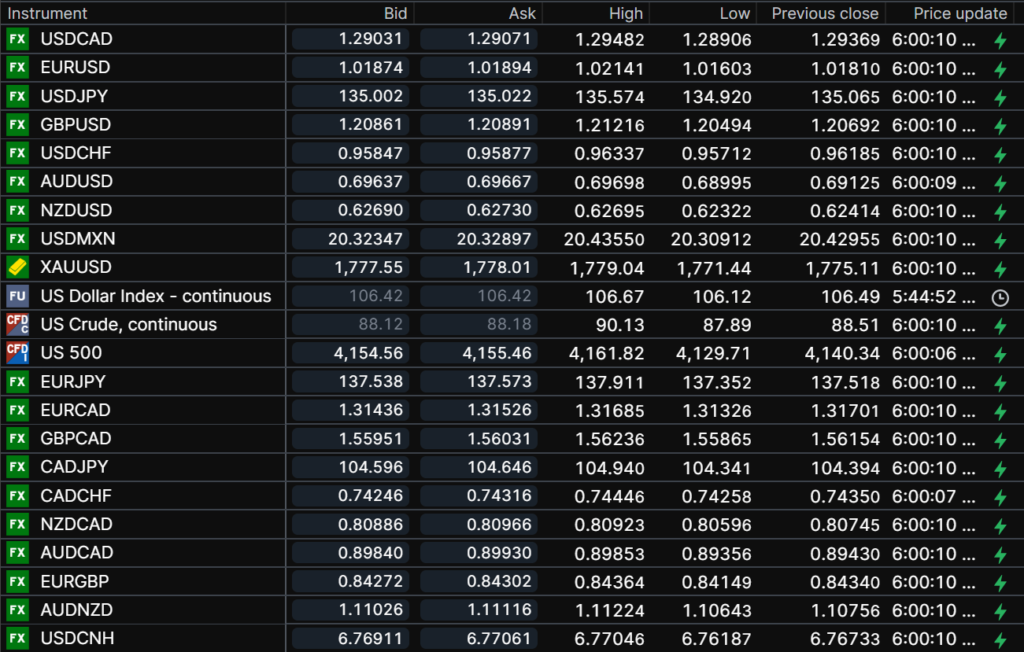

USDCAD Snapshot: open 1.2903-07, overnight range 1.2874-1.2948 close 1.2937

The better than expected US employment report and the worse than expected Canadian jobs data sucker punched USDCAD bears, Friday. However, they are attempting to recover today, helped by rebounding Wall Street futures and USDCAD is inching lower in NY trading

Canada lost 30,600 jobs in July on top of the 43,200 lost in June, which contrasted sharply with the 528,000 gain in the US. USDCAD soared from 1.2876 to 1.2981 and consolidated in a 1.2891-1.2948 range overnight.

The Canadian data suggests that the economy is cooling, however, Canadian employment data is notoriously unreliable. Even so, the data may temper the BoC’s enthusiasm for another jumbo rate hike.

USDCAD also slumped due to falling oil prices. WTI oil continues to probe support in the $86.70/b area, which represents the 38.2% Fibonacci retracement of the April 2020-March 2022 range.

The Canadian data calendar is empty.

USDCAD technical outlook

The intraday USDCAD technicals are bullish following the break above resistance at 1.2890 on Friday. The failure to break above 1.2990 suggests further 1.2890-1.2990 today, with an underlying uptrend while prices are above 1.2850. The price action is just noise inside the 1.2780-1.2980 range which contained prices since July 18.

For today, USDCAD support is at 1.2840 and 1.2810. Resistance is at 1.2890 and 1.2950. Today’s Range 1.2840-1.2910.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Markets continue to digest Friday’s blow-out US employment report (NFP 528,000 vs forecast 250,00), which suggests the US economy can withstand additional, aggressive Fed rate hikes.

Fed Governor Michelle Bowman agrees, saying, “I supported the FOMC’s decision last week to raise the federal funds rate another 75 basis points. My view is that similarly-sized increases should be on the table until we see inflation declining in a consistent, meaningful, and lasting way.” Her colleague, San Francisco Fed President Mary Daly, pointed out that the Fed is “far from done yet.”

Geopolitics has taken a nasty turn. China’s Foreign Minister insists that Taiwan is part of China, ignoring international law and history) and claims is hostile, aggressive military action against Taiwan is merely China conducting routine military exercises in own waters.

Russia is lobbing artillery shells at a Ukraine nuclear plant which has spooked the head of the Atomic Energy Agency and Ukrainians. A de facto nuclear war.

US and Iran nuclear talks are ongoing. US consumers may have embraced NIMBY (not in my Backyard). They are tired of paying $5.00+ for gas and appear willing to tolerate a nuclear-armed Tehran in exchange for cheap oil.

Higher interest rates and geopolitical tensions do not seem to concern global equity traders. Perhaps they agree with the JPM view that equities will rise until the end of 2023.

JPM suggests prices will rise due to: 1) attractive valuations 2) sentiment is overly bearish 3) Fed will become more sensitive to data after September meeting 4) US dollar strength may be peaking 5) strength of balance sheets 6) US house prices are resilient 7) labor market will remain robust 7) earnings will only see a modest pullback 8) consumer cushioned by excess savings 8) global down cycle unlikely to be synchronized as Chinese activity should turn better.

Asian equity markets closed slightly higher except those in China. European bourses are grinding out small gains as are DJIA and S&P500 futures. WTI oil and gold edged lower is, trading at the bottom of its 2.803-2.849% overnight range.

EURUSD traded sideways in a 1.0160-1.0214 range. The early European morning rally was snuffed out by weaker than expected Sentix investor confidence. The single currency remains defensive in anticipation of sharply higher US rates.

GBPUSD traded in a 1.2049-1.2122 range. Sentiment is negative due to political uncertainty, ongoing Brexit issues disrupting trade, fears of higher inflation, and the BoE prediction of a recession before year end.

USDJPY consolidated Friday’s gains in a 134.92-135.97 range. The bounce from Friday’s low was due to the surge in Treasury yields after the NFP data.

However, gains continue to be capped by demand for yen as traders unwind bullish USDJPY positions.

AUDUSD rallied from 0.6900 to 0.6970 after the better than expected Chinese trade data. Traders deliberately ignored veiled threats from Chinese officials suggesting the Australian government mind its own business and not concern themselves with Taiwan.

There are no US economic reports today.

Chart of the Day: WTI oil daily

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

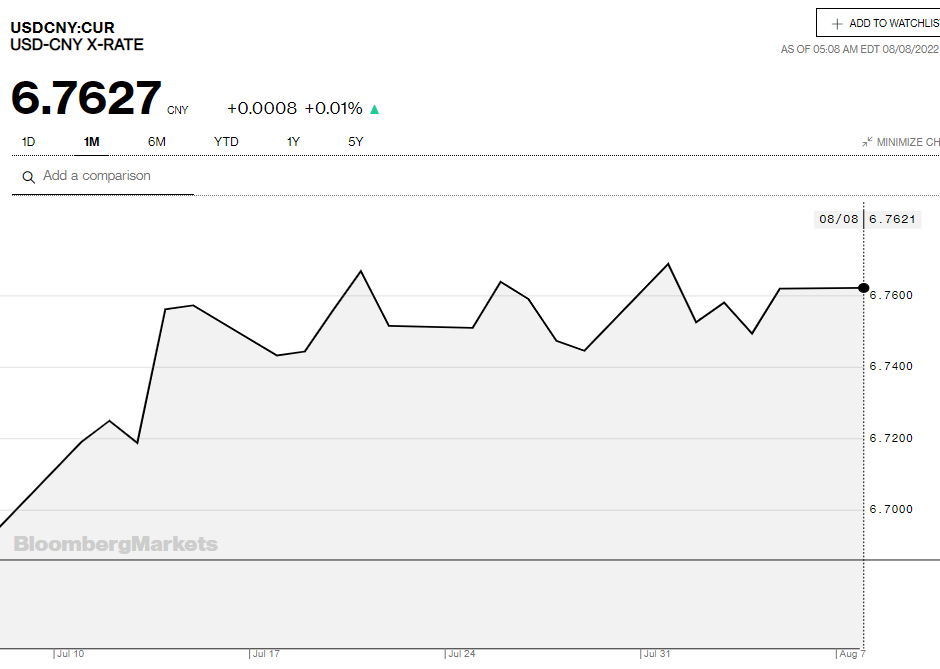

China Snapshot

Today’s Bank of China Fix: 6.7695, previous 6.7405

Shanghai Shenzhen CSI 300 fell 0.21% to 4,148.07

China Trade surplus jumps to $101.26 billion (forecast $90 bio, previous $97.94 bio), powered by 18% rise in exports

Chart: USDCNY 1 month

Source: Bloomberg