March 22, 2024

- Souring risk sentiment lifts US dollar and sinks CNY.

- Canada core Retail Sales rise more than forecast

- US dollar crushes opposition.

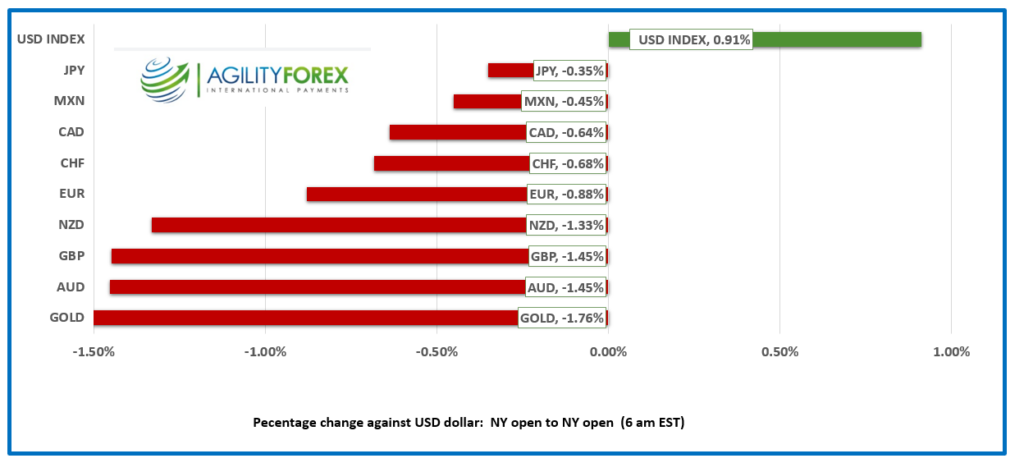

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3571-75, overnight range 1.3519-1.3582, close 1.3533

The loonie was feeling pretty cocky yesterday. The FOMC soothed fears that US rates would remain higher for longer on Wednesday and USDCAD was attempting to smash through support in the 1.3460 area. Then a rate cut in Switzerland and fresh robust US data derailed the USDCAD down move. Traders were spooked as it suggested US interest rate differentials would not narrow as quickly as expected because other G-7 countries would be cutting rates well before the Fed.

Maybe, maybe not. Fed Chair Powell was not ruffled by robust data and sticky inflation. He said the road to lower inflation would be bumpy which suggests yesterday’s data was just another pot-hole and not an abyss.

WTI oil prices traded in a 80.42-81.26 range. The are underpinned by news that India will refuse Russian oil shipped by Sovcomflot tankers due to US sanction fears.

Canada core retail sales (exclude autos, auto parts, gasoline stations and fuel vendors) rose 0.4% in January. The headline number decreased by 0.3%.

USD/CAD Technicals

Flip, flop, and fly. The intraday USDCAD flipped to bullish with the break above 1.3530 overnight and is now targeting 1.3610 and 1.3650. The uptrend line is steep and a move below 1.3540 will shift the focus to 1.3460.

USDCAD is trapped in a 1.3360-1.33660 range and that is unlikely to change until the next Fed meeting, May 1.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3610 and 1.3660. Today’s range is 1.3530-1.3610,

Chart: USDCAD hourly

Source: Investing.com

G-10 FX

The US Dollar Is Back From the Dead

Traders filled in the greenback’s grave following the FOMC meeting that showed policymakers had not changed their view on 2024 rate cuts. They dismissed higher-than-expected CPI results as “hiccups,” and to many, it spelled the demise of the dollar. US interest rate spreads compared to other countries would narrow, making the greenback less attractive.

It sounded good, right up until weekly jobless claims data underscored the strength of the job market, while existing home sales rose 9.5% in February. The US dollar soared across the board, and it is likely to consolidate those gains today unless remarks from Fed Chair Powell give US dollar bears new life.

The US dollar is also being supported after Chinese authorities allowed the yuan to weaken sharply (compared to the fix).

Equity Markets

Asian equity markets closed mixed. The Japanese indices squeezed out small gains, while Hong Kong’s Hang Seng index plunged 2.16%. In Europe, the FTSE 100 index is up 0.81%, the German Dax is posting a 0.12% gain, while the French CAC 40 is down 0.01%. S&P 500 futures are 0.15% higher. The US 10-year Treasury yield has eased down to 4.243% after closing at 4.271% yesterday.

EURUSD

EURUSD is just above support after trading in a 1.08808-1.0869 range overnight. Yesterday’s surprise rate cut by the Swiss National Bank, combined with stronger-than-expected US data, ignited a broad-based US dollar rally. The single currency saw a bit of support after German economic sentiment improved.

GBPUSD

GBPUSD traded in a 1.2575-1.2675 range overnight and is testing the low in New York. The selling pressure is a direct result of dovish comments by Bank of England Governor Andrew Bailey in a Financial Times interview that “rate cuts were in play.” Morgan Stanley now expects that UK rates will fall 1.00% in 2024. Earlier, GfK reported that consumer confidence stalled at -21 in March. UK retail sales, excluding fuel, rose 0.2% in March (forecast -0.1%).

USDJPY

USDJPY climbed steadily, rising from 151.26 to 151.87 after yesterday’s US data and higher-than-expected inflation. Japan’s CPI index was 2.8% year-over-year in February compared with 2.2% in January. The news puts a damper on additional rate hikes, at least in the near term.

AUDUSD and NZDUSD

AUDUSD is trading negatively in a 0.6510-0.6577 range due to a mix of broad US dollar strength and ongoing Chinese growth concerns.

NZDUSD is at the bottom of its overnight 0.6003-0.6052 range due to broad US dollar strength. Prices are pressured by AUDUSD demand due to robust Australian employment and weak NZD economic growth. Traders ignored a modest improvement in the NZ trade deficit.

USDMXN

USDMXN has traded erratically in a 16.7178-16.8085 range, roiled by a mix of robust US data and Banxico cutting interest rates by 25 basis points to 11.00%. Banxico said inflation forecasts were almost unchanged, but inflation risks are biased to the upside.

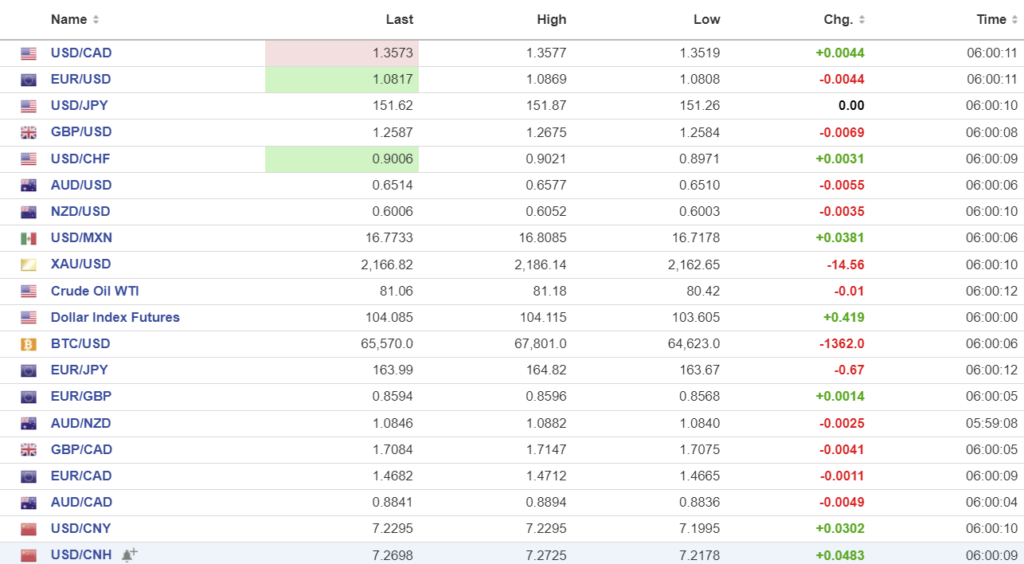

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

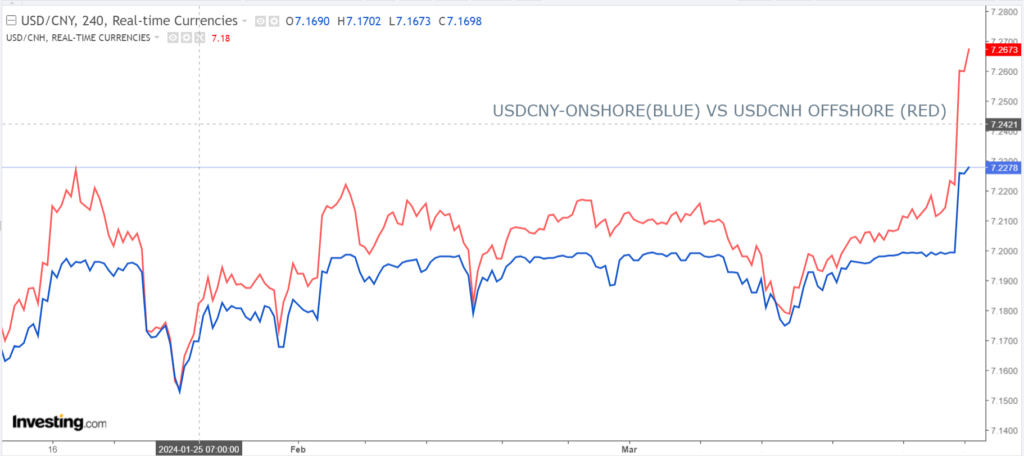

China Snapshot

PBoC fix: 7.1004 vs exp. 7.2147 (prev. 7.0942)).

Shanghai Shenzhen CSI 300 fell 1.01% to 3545.00.

The daily USDCNY fix has no bearing on reality as USDCNY is trading at 7.2294. Chinese officials appear to have given in to bullish USDCNY sentiment and failed to act to slow gains. Thee rally was exacerbated by dovish comments from a PBoC deputy governor yesterday and talk that the US is pondering banning mutual funds from investing in some products that track Chinese indexes.

Chart: USDCNY and USDCNH daily

Source: Investing.com