February 2, 2024

- Nonfarm payrolls surge to 353,000 (forecast 180,00)

- Soft landing cushioned further by data.

- US dollar erases overnight gains after NFP

FX at a glance-FX market change Pre-NFP (8:29 am) and Post-NFP (9:00 am)

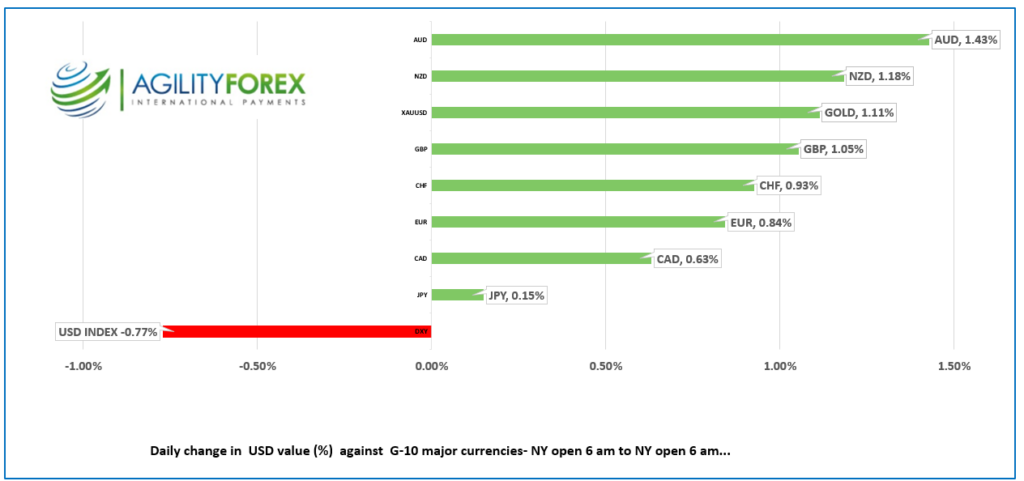

FX at a glance 24 hour change

Source: IFXA

USDCAD Snapshot: open 1.3371-75, overnight range 1.3365-1.3447, close 1.3388.

USDCAD blew its (overnight) top of 1.3389 and spiked to 1.3447 in the wake of the hotter than hot US nonfarm payrolls report. The rally helped to reinforce support in the 1.3360 zone. BoC Governor Macklem’s testimony to the House Finance Committee didn’t provide any fresh insight, and it was ignored by traders. He basically repeated his remarks from last week’s monetary policy meeting.

Oil bulls cannot catch a break. WTI price gains following the Iran proxy attack on a US base in Jordan have faded due to the lack of a US response (so far). US officials are trying to figure out how to punish Iran without causing any offense to the other Middle Eastern countries, which is leaving the ayatollahs laughing in the aisles. WTI dropped from $76.64 yesterday to $73.09 overnight due to talk of a Gaza peace plan.

There are not Canadian economic reports today leaving US data to dictate USDCAD direction.

USDCAD Technicals:

USDCAD remains in an intraday downtrend below 1.3450 which is likely to be tested today following the strong US NFP report. A failure to break above the top suggests further 1.3360-1.3450 range trading. A topside break will lead to a test of the November 1 downtrend line which is intact while prices are below the 1.3500-05 area.

Longer term Fibonacci retracement of the July-November range suggests that the move below 1.3405 (61.8% retracement) puts 1.3270 (78.6%) in play.

For today, USDCAD support is at 1.3360 and 1.3310. Resistance is at 1.3460 and 1.3490. Today’s range is 1.3390-1.3490

Chart: USDCAD 4 HOUR

Source: Daily FX

G-10 FX recap

It’s Groundhog Day. If the rodent sees or doesn’t see its shadow, it means nearly six more weeks until the next FOMC meeting (March 20). It’s also Nonfarm Payrolls Day and traders saw the spectre of unchanged interest rates for longer than previously anticipated. The odds of a rate cut in March dropped to less than 20% (from pre-NFP) of 52%.

Analysts key in on the surge in hourly earnings which jumped to 4.5% compared to the 4.1% expected. Even worse, the December numbers were revised upwards to 4.4% from 4.1%. That’s enough to spook Fed officials into believing that inflation will not be falling as quickly as anticipated. They may even regret removing the line suggesting “rates could rise” from Wednesday’s FOMC statement.

Markets were bummed out. The US dollar surged, and the US 10-year yield spiked to 4.0% from 3.88% pre data. SP500 futures dropped from a gain of 0.62% to 0.38%.

Markets are ignoring geopolitical risks. The White House has signaled a measured response to Iraq’s actions that killed members of the US military in Jordan. There are even rumors that the US would attack an Iranian warship in the Red Sea. Traders merely shrugged and thought, “It sucks to be them.”

Asian equity markets closed with gains led by Australia’s ASX 200, which rose 1.47%, but Chinese indexes sank. European bourses are trading with a bullish bias led by a 0.64% rise in the German Dax.

EURUSD is flopping like a fish on a river bank as it bounces between 1.0790 and 1.0898.rejected losses below 1.0800 due to yesterdays Euro area data and today’s US jobs report. The EUR/USD technicals suggest that a decisive break above 1.0880 will extend gains to 1.1000. while a break of 1.0760 targets 1.0700.

GBPUSD rallied to 1.2772 overnight than plunged to 1.2657 after NFP. Today’s US data supports that BoE view for the need to take a data dependent and cautious approach to monetary policy. incoming data. Traders agree, somewhat, and have lowered the odds of a May rate cut to 50% from 60%.

USDJPY erased earlier gains and surged to 148.07 from 146.24 low overnight. The jump in US Treasury yields triggered the rally.

AUDUSD also gave back its overnight gains and dropped to 0.6532 from a peak of 0.6511.Australian Q4 PPI rose 4.1% q/q from 3.8%

ISM Manufacturing PMI is expected at 49.1 (previous47.1)

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1006, expected 7.1655, previous 7.1049.

Shanghai Shenzhen CSI 300 fell 1.18%% to 3179.63.

Stocks suffered another meltdown before rumoured government intervention shored up prices.

IMF forecasts Chinese 2024 GDP at 4.6% due to ongoing property sector weakness and slowing global demand.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com