Photo: Freepik

September 15, 2023

- Risk sentiment improves with Chinese data and RRR cut.

- ECB’s dovish rate hike weighs on EURUSD

- US dollar opens mixed but CAD rally is stalling

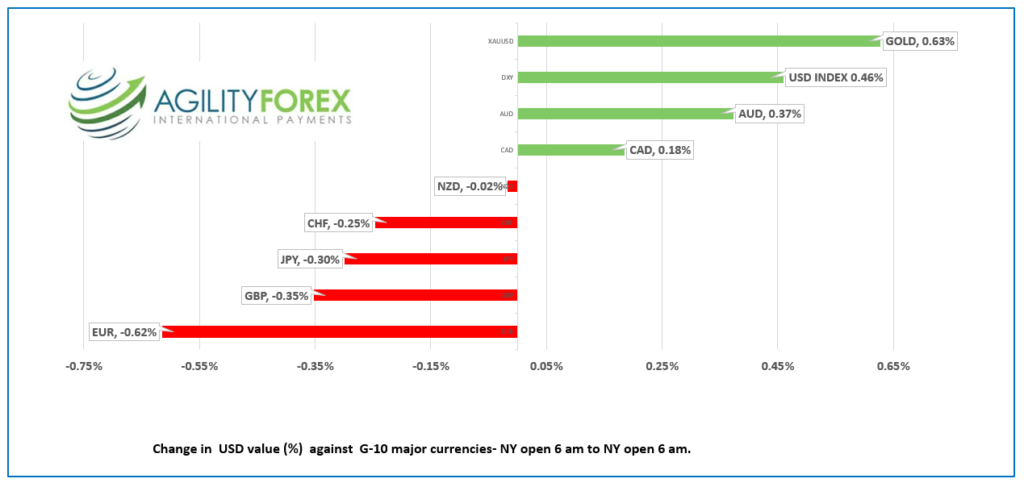

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3505-09, overnight range: 1.3494-1.3518, close 1.3510

USDCAD dropped on the back of improved risk sentiment sparked by the Peoples Bank of China’s latest rate cut and a bit of Chinese economic data that raised hopes that the drop in Chinese economic growth may have found a floor.

Oil traders are hoping that China’s actions increase crude demand and WTI rose to$91.15 from a low of $90.33 overnight. WTI has gained 5.8% since last Friday, and that has pressured USDCAD.

However, USDCAD inched higher in NY trading, coinciding with WTI retracing a large portion of its overnight move. Traders ignored positive results from domestic data. Foreign investment in Canadian securities rose for the fourth month in a row although it was a tad below estimates. Meanwhile Manufactguring Sales increased 1.6% in July and Wholesale sales grew 0.2%.

The focus shifts to the upcoming FOMC meeting on Wednesday September 20. Markets are hoping that the Fed will also leave rates unchanged and hint that they are finished with rate hikes for now.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3550, looking for a decisive break below the 1.3490 to extend losses to 1.3440 and then 1.3360. A break above 1.3580 argues for more 1.3490-1.3660 consolidation.

For today, USDCAD support is at 1.3490 and 1.3460. Resistance is at 1.3560 and 1.3590. Today’s range 1.3490-1.3560

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Traders are feeling rather buzzed, almost as if they paid just ‘two-fifty for a highball, or a buck and a half for a beer.’ Tragically, it isn’t hip to sell drinks at that price in 2023.

The UAW has gone on strike, shutting down assembly plants at GM, Ford, and Stellantis (formerly Chrysler). They appear to have ripped a page out of the Ontario Teachers’ Union playbook, which is to inconvenience as many people as possible while wreaking economic havoc. The only difference is that the UAW is honest with their demands for more money, while teachers claim they only go on strike ‘for the children.’

The ‘quadruple witching hour’ option expiries may disrupt equity markets around 10:00 am and also lead to some FX volatility.

European bourses liked the idea of the end to rate hikes, and the French CAC is leading the parade higher with a 1.56% gain. S&P 500 futures are flat. Traders are cautious as it is quadruple witching day in the equity option market.

EURUSD is bouncing in a 1.0633-1.0669 band. The ECB signaled that yesterday’s 0.25% rate hike, which lifted the overnight rate to 4.0%, could be the final increase for this cycle, pressuring EURUSD. In addition, the robust US PPI and Retail Sales reports underscored the American economic outperformance compared to Europe. The EURUSD technicals are bearish and targeting the 1.0490-1.0500 area.

GBPUSD is at the bottom of its 1.2391-1.2447 range. As analysts expect a dovish rate hike from the Bank of England next week, the GBPUSD technicals are bearish below 1.2540 and looking for a break of 1.2390 to extend losses to 1.2280.

USDJPY is at the top of its 147.34-147.96 trading range due to the US 10-year Treasury yield climbing to 4.32% after closing at 4.29% yesterday. Prices are also supported after Japanese officials suggested that BoJ Governor Ueda’s comments last weekend were taken out of context.

AUDUSD gave back all of its overnight gains and is trading in a 0.6430-0.6474 range but still supported by the latest Chinese data and PBoC rate cut.

US Capacity Utilization, NY Empire State Manufacturing PMI, Industrial Production, and Michigan Consumer Sentiment data are ahead.

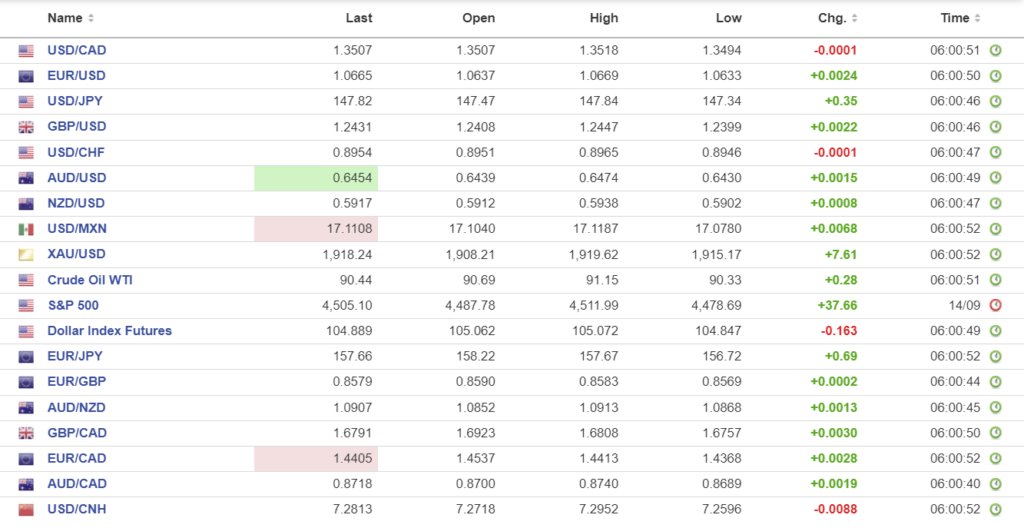

FX high, low, open

Source: Investing.com

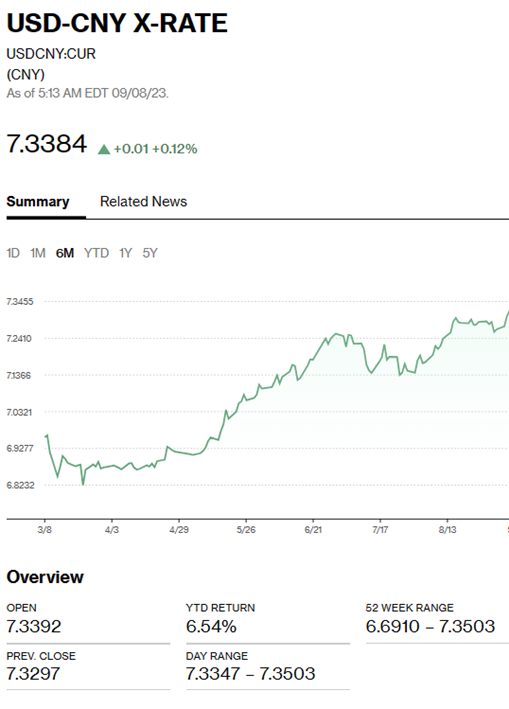

China Snapshot

Bank of China Fix: today 7.1786, expected 7.2849, previous 7.1874.

Shanghai Shenzhen CSI 300 fell 0.66% to 3708.78.

PBoC cut Reserve Requirement Ratio (RRR) for all banks by 0.25% yesterday effective today.

August Industrial Production 4.5% y/y (forecast 3.9%, July 3.7%)

August Retail Sales 4.6% y/y (forecast 3.0%, July 2.5% y/y)

Chart: USDCNY 1 month

Source: Bloomberg