Photo: Bing Image Creator

November 1, 2023

- Fed expected to leave rates unchanged.

- Treasury quarterly refunding announcement lower than expected.

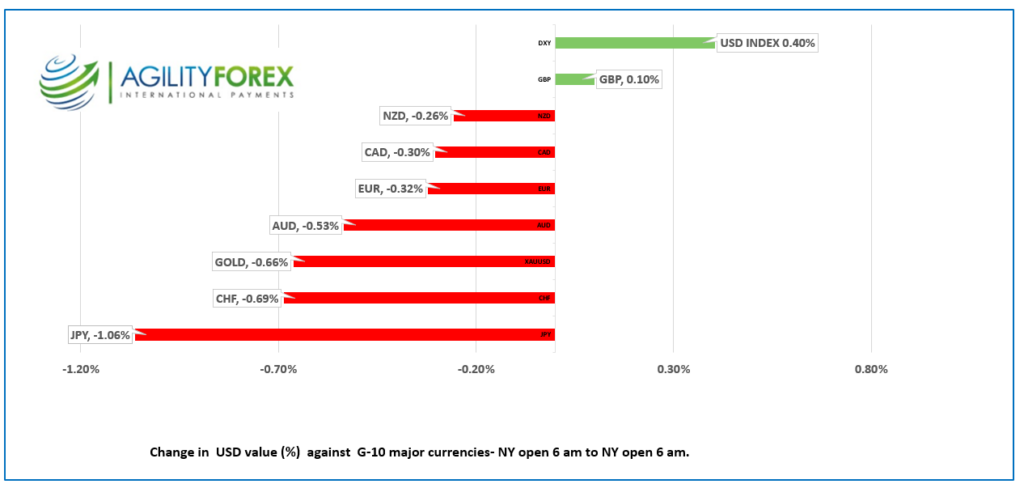

- US dollar opens with gains-JPY drops 1.06% from yesterday’s open.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3885-89, overnight range 1.3864-1.3890, close 1.3877

USDCAD is trading with a bullish bias on the back of broad based US dollar demand. Yesterday’s Canadian GDP data showed no growth, the same as the August data, which doesn’t bode well for the BoC’s forecast of 0.8% growth in Q3. Even worse, the US economy is on a tear which leaves the Fed room to hike rates to fight inflation while the BoC would have a hard time justifying further tightening.

The rise in the US dollar alongside weaker than expected Chinese growth weighed on oil prices. WTI fell from $83.29/b yesterday to $81.03/b overnight before bouncing back to $82.37/b in NY.

The USDCAD direction will be determined by the market reaction to the US Treasury’s quarterly refunding announcement and by Powell’s post-FOMC press conference.

The Canadian data calendar is empty.

USDCAD Technicals:

The intraday USDCAD technicals are bullish above 1.3840, supported by yesterday’s move above 1.3860, and looking for a break above 13905 to extend gains to 1.4000, A break below 1.3810 suggests a test of the October uptrend line at 1.3750.

Longer, term, the USDCAD uptrend channel from July targets 1.3940 while above 1.3570.

For today, USDCAD support at 1.3840 and 1.3810. Resistance at 1.3910 and 1.3940. Today’s expected trading range is 1.3830-1.3930

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The US Treasury quarterly refunding announcement appears to have been received favourably. Analysts were expecting an auction of $114.0 billion, $11.0 billion higher than in July. However, Treasury will only auction $112.0 billion.

The news knocked the 10-year Treasury yield down to 4.863% from 4.901% earlier while the US dollar eased slightly, and S&P 500 futures clawed back some losses. Nothing earth shattering, but not the disaster many feared.

The monthly ADP Employment change report showed the US gained 113,000 jobs in October, below the 150,000 expected.

This afternoon, Fed Chair Powell and his colleagues are expected to leave rates unchanged at 5.50%. However, they will suggest that the risk is still for more rate hikes, a view supported by some recent robust economic data, including higher PCE and strong employment reports. Analysts suggest the Fed can afford to take a break because bond traders, who are driving yields higher, are tightening US rates for them.

The US dollar remains bid and got added support from the latest Caixin China PMI report, which showed the economy stumbled in October. Trading was muted in Europe due to many countries being closed for All Saints’ Day.

EURUSD was steady in a 1.0541-1.0581 range, with traders sidelined ahead of the Fed. The single currency is vulnerable to further losses due to divergent US and Euro area economic growth and interest rate differentials.

GBPUSD mirrored EURUSD activity and drifted in a 1.2123-1.2162 range. GBPUSD gains were capped after Manufacturing PMI was 44.8, compared to September’s reading of 45.2. The UK Guardian quoted Rob Dobson, Director at S&P Global Market Intelligence, who said, “The UK manufacturing downturn continued at the start of the final quarter of the year, meaning the factory sector remains a weight dragging on an economy already skirting with recession.”

USDJPY consolidated yesterday’s gains in a 151.09-151.71 range and is at the bottom of that band in NY trading. The dovish BoJ outcome combined with the rise in US Treasury yields and the risk of a hawkish “hold” from today’s FOMC meeting fueled the rally. Jabbering about USDJPY strength by Finance officials was ignored.

AUDUSD traded in a 0.6318-0.6348 range, supported by a modest rise in the October Manufacturing PMI to 48.2 from 48.0 in September.

ISM Manufacturing PMI, Construction Spending, and JOLTS job turnovers are on tap.

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1778, expected 7.3327, previous 7.179

Shanghai Shenzhen CSI 300 fell 0.04% to 3571.03.

Caixin October Manufacturing PMI drops to 49.5 (forecast 50.8, September 50.6) suggesting that the Chinese economy is struggle to grow.

Chart: USDCNY (onshore) vs USDCNH (offshore) hourly

Source: Investing.com