Overnight Range 1.3066-1.3109

The US dollar popped higher following this mornings better than expected US Retail Sales data and a higher inflation reading. Retail Sales rose 0.4% in January (forecast 0.1%) while Retail Sales-ex autos jumped to 0.8%. (Forecast 0.4%). A big jump in headline CPI for Janauary, (Actual 0.6% vs.forecast 0.3%, m/m, provides additional support to those looking for a March rate hike.

The USDCAD rally following the US data ran into resistance in the 1.3110 area thanks to a big jump in Canadian Manufacturing shipments, which rose 2.3% in December (Forecast 0.1%). That news will put a smile on Bank of Canada Governor Poloz’s face since he has been looking for an export led recovery for a long time.

Overnight, the session was orderly and the US dollar rose., extending Tuesday’s post Yellen speech gains.

Yesterday, Fed Chair Janet Yellen appeard to open the door, slightly, to a March rate hike when she said ““waiting too long to remove accommodation would be unwise, potentially requiring the FOMC to eventually raise rates rapidly, which could risk disrupting financial markets and pushing the economy into recession.” The US dollar rallied.

The Australian dollar defied the trend to a stronger dollar and inched higher, supported by an increase in domestic auto sales and a rise in Asia equities. NZDUSD followed suit. However, the gains for both currency pairs were very modest.

USDJPY ticked higher, rising from 114.24 to 114.54 supported by the rise in Treasury yields that coincided with the slightly improved March rate hike tone.

EURUSD drifted higher in Asia, rising from 1.0565 to 1.0585 just before Europe started trading and renewed EURUSD sellers emerged. EURUSD dropped down to 1.0542 with traders focused on the upcoming US Retail Sales, CPI, and part two of Yellen’s testimony.

EURUSD ignored a miss in the ZEW Economic Sentiment and current Situation survey and managed to hang-on to most of its overnight gains. EURUSD rose from 1.0592 to 1.0632 before pulling back to 1.0542 when New York opened. A wider than expected Eurozone Trade surplus (Actual Dec. 24.5 billion vs. Nov. 22.2 b) didn’t have any impact.

Eurozone data may have been ignored but UK data wasn’t. GBPUSD got spanked when a decline in earnings overshadowed a strong employment report. GBPUSD dropped from 1.2463 to 1.2415.

Oil prices are lower, opening in New York at $52.96/b following yesterday’s API report of a large increase in US crude inventories. The 9.94 million barrel increase follows the 14.2 million barrel increase from the week before which seems to be testing the patience of oil bulls.

The Canadian dollar drifted aimlessly. Firm oil prices and strong domestic data are offset by the prospect of higher US rates.

Overnight Ranges

|

Open |

|||

| 15-Feb-17 |

High |

Low |

|

| USDCAD |

1.3076 |

1.3093 |

1.3066 |

| EURUSD |

1.0553 |

1.0584 |

1.0544 |

| USDJPY |

114.51 |

114.59 |

114.24 |

| GBPUSD |

1.2435 |

1.2474 |

1.2422 |

| USDCHF |

1.0088 |

1.0095 |

1.0059 |

| AUDUSD |

0.7677 |

0.7685 |

0.7655 |

| NZDUSD |

0.7172 |

0.7186 |

0.7156 |

| USDMXN | 20.3064 | 20.3408 |

20.2445 |

| WTI |

52.95 |

53.07 |

52.76 |

| Close 4:00 pm EDT-Open 6:00 am EDT | |||

USDCAD Technical outlook:

The USDCAD technicals are bearish while prices are below 1.3140. Yesterday’s rally from 1.3024 is merely corrective if this level holds. A break above 1.3140 would suggest that a short-term low is in place an point to further gains to 1.3260. A move below 1.3020 and then 1.2990 would lead to additional losses to 1.2880. For today, USDCAD support is at 1.3060, 1.3020 and 1.2990. Resistance is at 1.3110 and 1.3140.

Today’s Range 1.3040-1.3140

Chart: USDCAD 4 hour

Source: Saxo Bank

Source: Saxo Bank

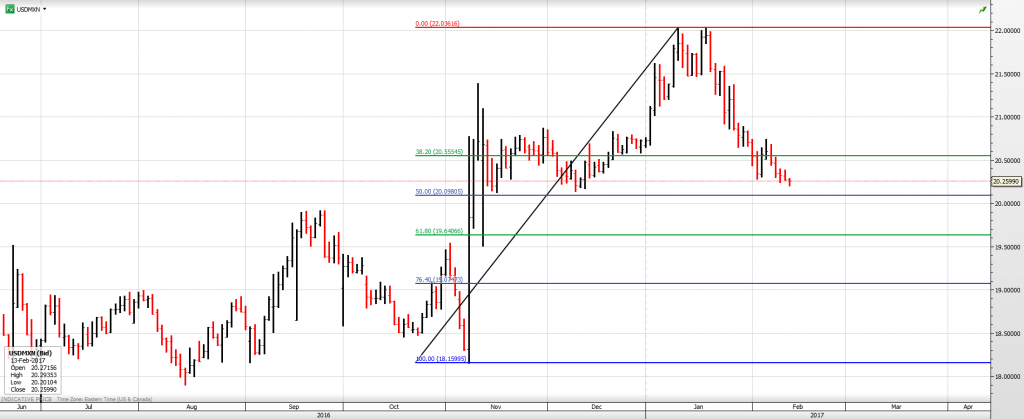

MEXICO

USDMXN broke above 20.2910 yesterday and snapped the downtrend line that had been in place since the middle of January. The rally stalled at 20.4425 but while prices are above 20.3050 the target is 20.5475. A move below 20.3050 will target support at 20.1990.

Chart: USDMXN 4 hour

Source: Saxo Bank

Source: Saxo Bank