October 18, 2024

- Risk sentiment improves on talk of more Chinese stimulus.

- Oil prices remain soft.

- US dollar opens with a mixed tone after uneventful overnight session.

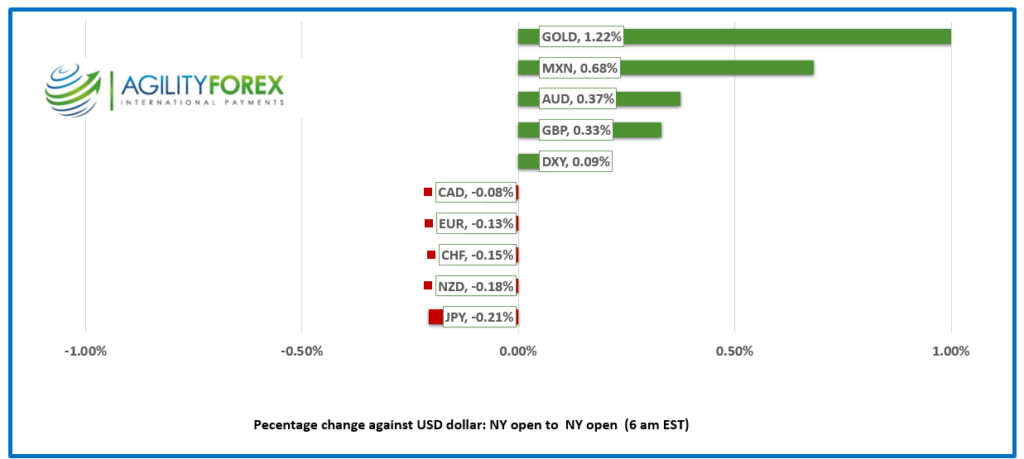

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3793, overnight range 1.3786-1.3800, close 1.3798

USDCAD was ignored overnight but remained near the top of its recent range. The CAD/US 10-year yield spread has widened to 92.1 this morning which means US bonds are even more attractive, and another reason to avoid Canadian dollars. The last time the spread was at this level was in June and USDCAD was trading at 1.3790.

FX traders are ignoring reports that Prime Minister Trudeau is facing a party revolt. Four cabinet ministers have announced that they won’t seek re-election which will lead to an imminent cabinet shuffle. In addition there are many reports of an internal caucus revolt that seeks to force Trudeau to step-down.

WTI oil prices are also underpinning USDCAD even though the day’s of Canada being considered a petrocurrency are numbered. WTI is trading negatively in a 70.14-71.23 range after the odds of a middle east oil supply disruption were lowered. That’s because Israel killed the Hamas terrorist leaders responsible for the Octo 7 2023 attack and the main advocate for prolonging the Hamas war with Israel.

There are no Canadian economic reports today.

USDCAD technicals

The intraday USDCAD are bullish above 1.3770 looking for a break above 1.3850 to extend gains to 1.3900. A move below 1.3750 targets 1.3730.

USDCAD is in a steep uptrend on a daily chart that suggests while prices are above 1.3740 further gains to 1.3900 are likely. A move below 1.3740 risks further losses to 1.3630.

For today, USDCAD support is 1.3750 and 1.3710. Resistance is at 1.3830 and 1.3850.

Today’s Range 1.3740-1.3830

Chart: USDCAD daily

Source: Investing.com

US Dollar Stays Firm

The US dollar is feeling rather frisky with the US dollar index (DXY) rising steadily all week and extending the gains made since September 27. Prices are underpinned by “just-in-case” dollar buying in the event Trump gets elected, in addition to the outlook for upcoming US rate cuts to lag those of other G-10 central banks. China’s latest announcement that the PBoC is considering cutting its Reserve Requirement Ratio (RRR) before year-end has improved risk sentiment in Asia but only modestly as the Chinese economy is being artificially propped up by the government. Gold (XAUUSD) climbed further, in a continuation of the rally that started in July. XAUUSD broke through the 2700 level and reached 2714.07.

“Chirp, Chirp Chirp”

Tier-one actionable US economic data is in short supply today. Not so for Fed officials. Governor Christopher Waller, Atlanta Fed President Raphael Bostic and Cleveland Fed President Neel Kashkari will be offering opinions on US monetary policy today. Meanwhile European bourses are mixed. The UK FTSE 100 is down 0.31% while the French CAC 40 index is up 0.52%. S&P 500 futures are up 15% and the 10-year Treasury yield is 4.10%.

EURUSD

EURUSD is consolidating yesterday’s post-ECB losses in a 1.0825-1.0845 range. The central bank cut rates by 25 bps as expected, and President Christine Lagarde just fell short of declaring outright victory in the fight against inflation. Her press conference was considered dovish, and analysts expect another rate cut at the next meeting, which essentially caps EURUSD at 1.0900.

GBPUSD

GBPUSD popped to 1.3072 from yesterday’s NY close of 1.3011 following stronger-than-expected Retail Sales data, then dropped to 1.3042 in NY. September retail sales rose 0.3% m/m (forecast -0.3%, previous 1.0%) and 3.99% y/y, compared to the forecast for a 3.2% gain. However, Wednesday’s weak services inflation data and the prospects of two more rate cuts capped gains.

USDJPY

USDJPY rallied to 150.29 in early Asian markets following cooler-than-expected inflation numbers. September CPI rose 2.5% y/y compared to 3.0% in August, and CPI ex-fresh food rose 2.4% y/y compared to 2.8% y/y in August. Prices dropped to 149.77 after Vice Finance Minister Atsushi Mimura warned, “At the moment we’re seeing slightly one-sided, sudden moves in the currency market. We’ll keep monitoring the forex market with a high sense of urgency, including any speculative moves.”

AUDUSD and NZDUSD

AUDUSD is trading with a bit of a bid, rising from 0.6694 to 0.6719 due to improved risk sentiment following talk of additional Chinese stimulus. The intraday technicals turned bullish with the move above 0.6690 and are looking to test resistance at 0.6750. NZDUSD is at the top of its 0.6054-0.6074 range due to hopes for more Chinese stimulus.

USDMXN

USDMXN is in the middle of its 19.7343-19.8556 range but trading with a bullish bias. Ongoing concerns about planned judicial reforms in Mexico and the final leg of the US presidential election are underpinning prices. Trump is considered bullish for USDMXN, while Harris is an unknown quantity.

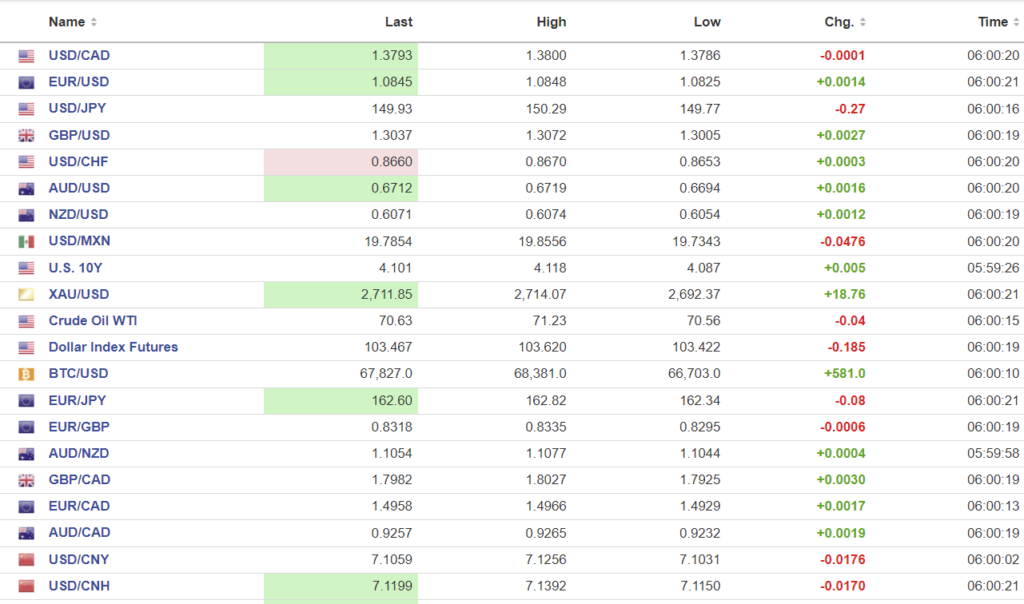

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1274 (prev. 7.1220)

Shanghai Shenzhen CSI 300 rose 3.62% to 3925.23

PBoC Governor Pan Gongsheng said they are considering another cut in the Reserve Requirement Ration (RRR) after somewhat disappointing growth data. Q3 GDP 0.9% q/q (forecast 1.0%, previous 0.7%), Q3 GDP 4.6% y/y (forecast 4.5%, previous 4.7%). The GDP number is the lowest since June 2023. That negative news was offset by the rise In Industrial Production in September to 5.4% y/y (forecast 4.6%, August 4.5%).

Retail Sales rose 3.2% y/y in September (forecast 2.5% August 2.1%) which was a four month peak but mainly due to a government trade-in program for purchases of cars and appliances.

Chart: USDCNY and USDCNH

Source: Investing.com