Source:americanmagazine.org/opinida.com

- US politicians will boycott China Olympics

- Risk sentiment rebounds in delayed reaction to PBoC RRR cut news

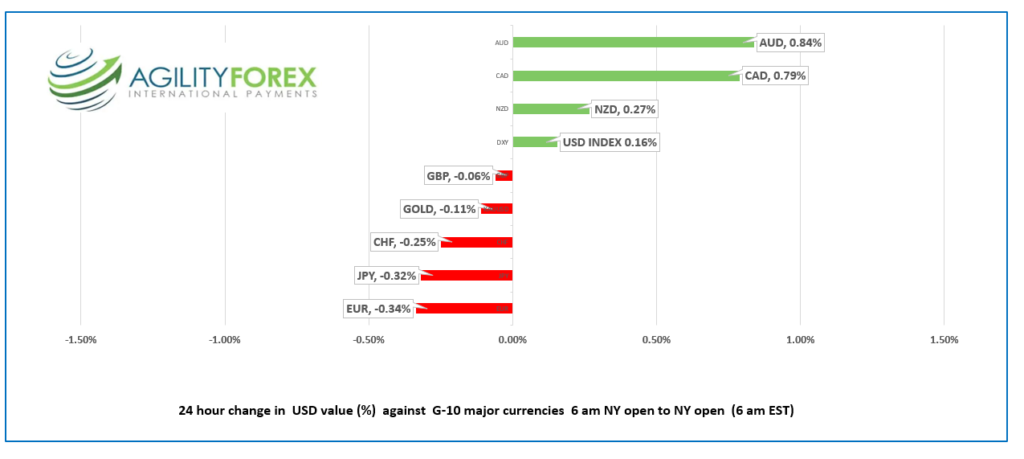

- US dollar opens weaker vs commodity currency bloc, firms vs the rest

FX at a Glance for November

Source: IFXA Ltd/RP

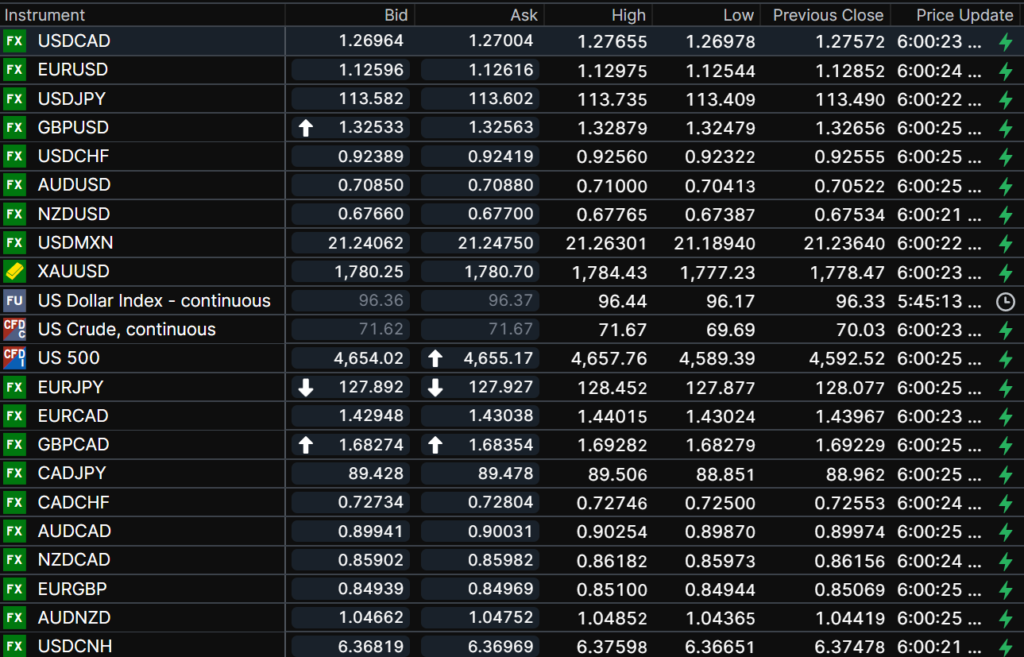

USDCAD Snapshot Open 1.2696-00, Overnight Range 1.2666-1.2766, Previous close 1.2757

USDCAD dropped as risk sentiment improved. Higher Wall Street stock prices and the rebound in WTI prices due to diminished concerns that the Omicron variant will derail global and domestic growth knocked prices lower.

WTI rallied to $71.90/b in NY trading today, from a low of $69.69/b overnight, supported by the Chinese trade report, which also weighed on USDCAD.

Wednesday’s BoC monetary policy may see Governor Tiff Macklem prime the rate hike pump, supported by robust jobs data and soaring inflation numbers.

Technical view: The USDCAD technicals turned bearish with the break below 1.2760, which snapped the base of the uptrend channel from mid-November and set the stage for further losses to 1.2580. However the June uptrend is intact above 1.2410. Fibonacci retracement of the November 16-Dec 3 range suggests support at 1.2670 (50% Fibo level) and 1.2620 (61.8 Fibo level.)

For today, USDCAD support is at 1.26600 and 1.2620. Resistance is at 1.2710 and 1.2740. Today’s Range 1.2650-1.2720

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

It appears that traders were a tad slow on the uptake following Monday’s news from the Peoples Bank of China. The PBoC said they would cut the primary RRR rate by 0.50 bps on December 15 and increase support for small businesses. Analysts suggest it also means it will support beleaguered property developers, which combined to help lift Asia equity indexes today, as did better than expected Chinese trade data.

Wall Street closed on a positive note helped by diminished fears of another global slowdown from the Omicron variant after experts said it may be highly transmissible but milder than Delta.”

That sentiment continued overnight, and the major Asia equity indexes closed with solid gains, led by a 2.17% rise in Hong Kong’s Hang Seng. European traders joined the party. The major indexes posted significant gains, with the German Dax rising 2.04% and the UK FTSE 100 1.15%. DJIA and S&P 500 futures extended yesterday’s gains, rising 1.03% and 1.35%, respectively. Gold prices are close to unchanged while WTI climbed over 3.0%. The US 10-year Treasury yield drifted to 1.45% from an overnight low of 1.428%.

Traders ignored news that the US government plans to boycott the Beijing Olympics to protest human rights abuses. China didn’t. The Global Times tweeted, “To be honest, Chinese are relieved to hear the news, “because the fewer US officials come, the fewer viruses will be brought in.”

Traders also do not seem concerned about US and EU tensions with Russia over Ukraine.

EURUSD remained under pressure as prices dropped from 1.1298 to 1.1229 in early NY trading. The single currency is weighed down by dovish ECB policies making EURUSD an attractive funding currency for riskier assets. Eurozone data didn’t help. Q3 GDP grew 2.2% q/q in Q3 and the employment change was 2.1% y/y. The German ZEW indicator of Economic Sentiment showed the current outlook worsened.

GBPUSD followed the single currency lower, dropping to 1.3221 from 1.3288 in part due to BoE rate hike forecasts being pushed out until February. On-going Brexit issues and UK coronavirus concerns are also negative factors.

USDJPY tracked US Treasury yields in a 113.41-113.74 range. Prices retreated from the session peak when the 10-year yield eased off its high.

Prices were also boosted by the improved risk-seeking tone which led to the unwinding of some safe-haven yen trades.

AUDUSD rallied from 0.7041 to 0.7102, where it trades in NY following the Reserve Bank of Australia monetary policy meeting. Interest rates were left unchanged at 0.1%, as expected. RBA officials were not overly concerned about the Omicron variant derailing the recovery. However, analysts suggest that the RBA will taper or end its bond purchase program in February due to the strong rebound in economic activity and rising inflation.

US and Canadian trade reports are ahead.

Chart of the Day: EURUSD

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

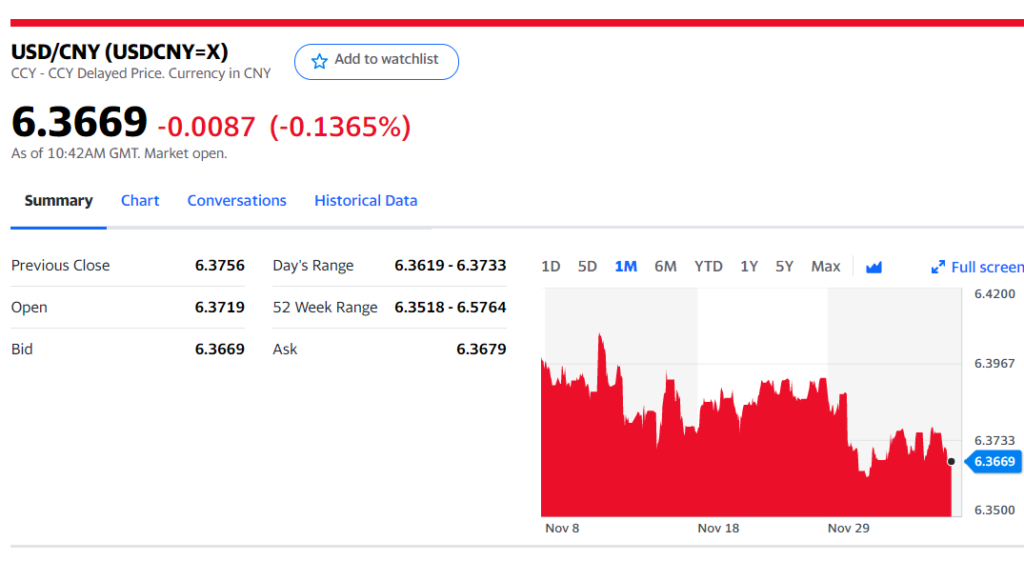

China Snapshot

Today’s Bank of China Fix 6.3738, Previous 6.3702

Shanghai Shenzhen CSI 300 rose 0.60% to 4,922.10

November Trade balance $71.72 billion, compared to October $84.54B

Imports rise 31.4% y/y while Exports rose 22% y/y

PBoC easing measures helps lift property developer shares and global risk sentiment.

Chart: USDCNY 1 month

Source: Yahoo Finance