July 9, 2024

- Markets hoping that Powell adopts a dovish tone to rates.

- French election results put fiscal deficit on center stage.

- US dollar opens little changed from yesterday.

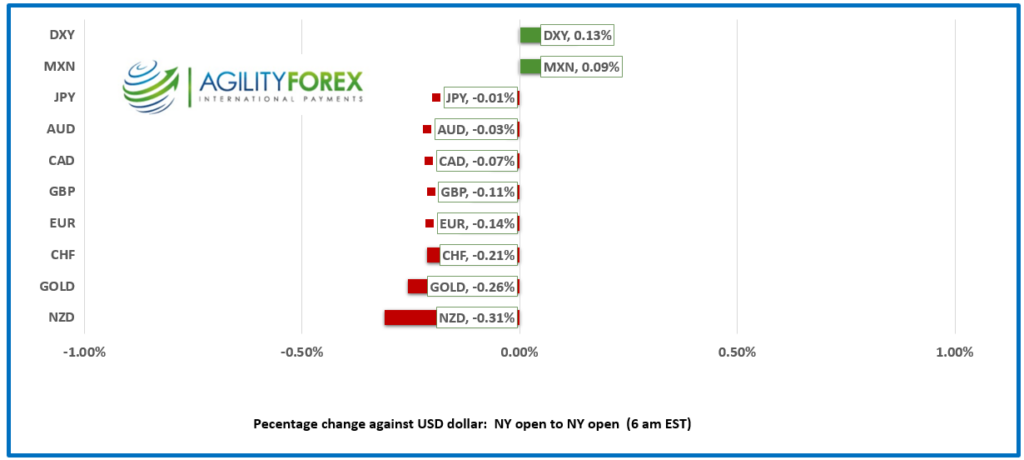

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3641, overnight range 1.3628-1.3648, previous close 1.3637

USDCAD barely budged in a somnolent overnight session. That will change near 10:00 am today, when chunky options expire and the text of Fed Chair Powell’s opening remarks to Congress are released.

Reportedly, there are $2.2 billion of USDCAD 1.3590-1.3600 strikes expiring this morning, which should put a floor under the currency pair until then.

WTI oil prices traded in a 81.69-83.43 range with downside pressure stemming from Hurricane Beryl being demoted to merely Tropical Storm Beryl. Prices are supported by concerns about escalating hostilities between Israel and Hezbollah, but gains are hampered by ongoing fears of reduced demand from China.

USDCAD Technicals

The intraday technicals are neutral. A break above 1.3650 targets 1.3690 while a move below 1.3620 puts 1.3590 in play.

The longer term outlook is unchanged. The price action below the 200-day moving average and the 38.2% Fibonacci retracement level of the January -April range provide a cluster of strong support levels. A decisive breech of this area targets 1.3510.

For today USDCAD support is at 1.3590 and 1.3550. Resistance is at 1.3660 and 1.3690. Today’s range is 1.3590-1.3690

Chart: USDCAD daily

Source: DailyFX

Chairman Brown, Ranking Member Scott, and other members of the Committee

Bond traders think they know what Fed Chair Powell will say to the Senate banking committee, which is why the 10-year Treasury yield has dropped to 4.291% today from 4.44% less than a week ago. They think he will deliver an optimistic outlook on US rates, which is why the odds for a September rate cut are around 77%. It was just over two weeks ago when policymakers downgraded their dot-plot projections to just one rate cut in 2024, so it seems a bit of a stretch for Mr. Powell to pull a U-turn and open the door to easing.

NATO Summit

President Joe Biden opens the three-day NATO summit in Washington followed by a dinner. Reportedly, the meal will be served at 4:00 pm to ensure the President is not late for his 8:00 pm bedtime. Canadian Prime Minister Justin Trudeau will attempt to convince attendees that Canada spending less than 1.49% of GDP on defense is really the equivalent of over 2.0% when you account for climate change spending and LGBTQ and Indigenous rights.

EURUSD

EURUSD traded in a 1.0815-1.0833 range. The immediate focus is on Fed Chair Powell’s testimony today, but the prospects of a spend-happy French government have analysts worried that French fiscal restraint will go the way of the guillotine, which was last used in 1977. That’s when Hamida Djandoubi lost his head and entered the history books.

GBPUSD

GBPUSD is trading below yesterday’s 1.2846 peak but has a modest bid, rising from 1.2796 to 1.2821 due to speculation that GBP will outperform the Euro in the wake of the French elections. BRC Retail Sales fell 0.5% in June compared to 0.4% previously.

USDJPY

USDJPY drifted in a 160.74-161.13 range with the focus squarely on Powell’s testimony today. Bloomberg is reporting that BoJ officials are asking banks and securities firms for input into how aggressively it should reduce bond-buying ahead of the July 31 BoJ meeting.

AUDUSD and NZDUSD

AUDUSD traded sideways in a 0.6728-0.6748 range following mixed data. Westpac Consumer Confidence fell 1.1% in July (previous 1.7%), and NAB’s Business Conditions Index dipped to 4 from 6. On the positive side, NAB Business Confidence rose to 4 from an upwardly revised -2 previously. The data was ignored.

NZDUSD traded defensively in a 0.6114-0.6133 range with Powell and the RBNZ in focus today. The RBNZ is universally expected to leave rates unchanged at 5.50%.

USDMXN

USDMXN traded in a 17.9810-18.0590 range. Traders did not seem to be bothered by news that Mexican inflation rose higher than expected in June. (actual 4.98% vs forecast 4.84% y/y and 4.69% y/y previously, June core inflation rose a less than expected 0.22%m/m (forecast 0.24% but it was higher than 0.17% m/m in May.

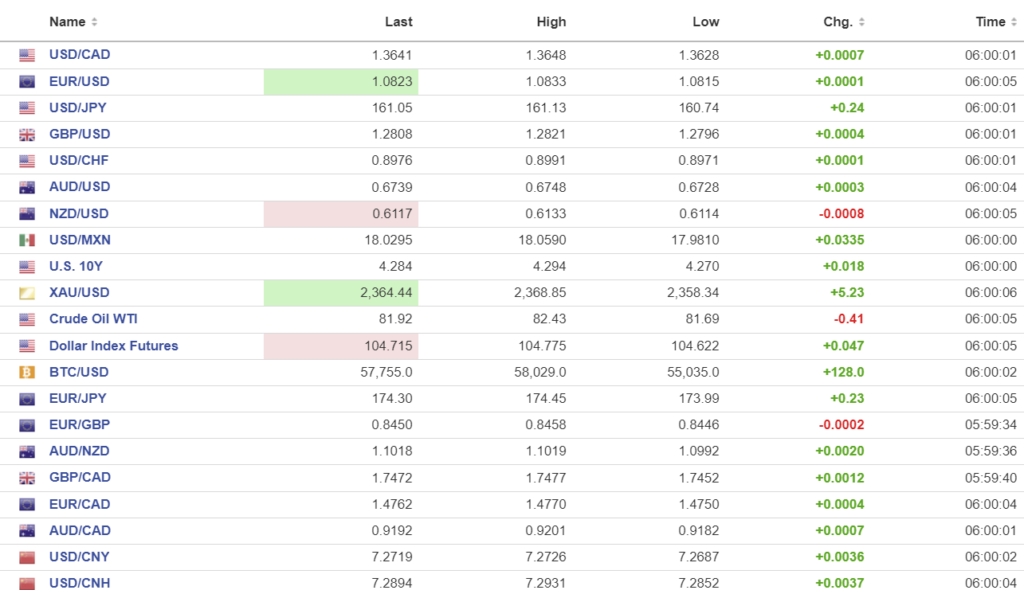

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1310 vs exp. 7.2676 (prev. 7.1286).

Sanghai Shenzhen CSI 300 rises 1.12% to 3439.81

Chart: USDCNY and USDCNH

Source: Investing.com