May 22, 2024

- Today’s FOMC minutes will be a non-event

- UK inflation numbers boost GBPUSD

- US dollar opens mixed after quiet overnight session.

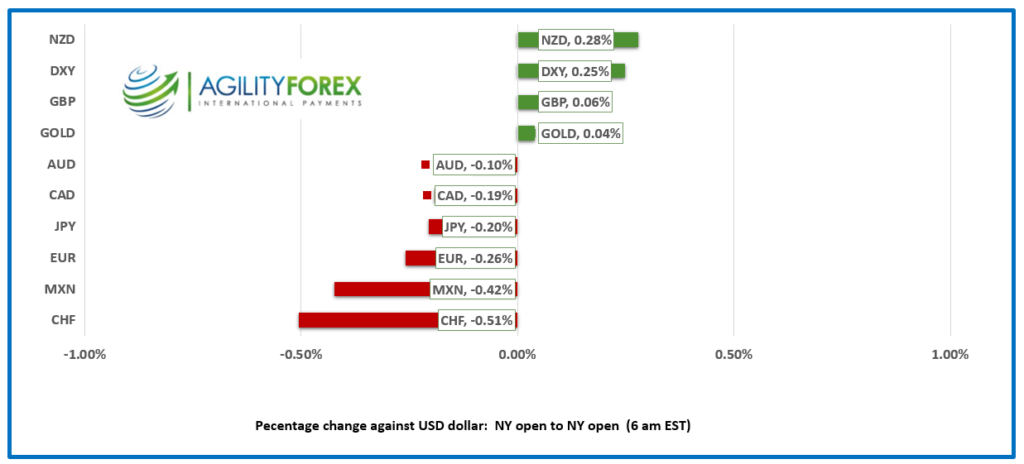

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3657, overnight range 1.3624-1.3669, close 1.3655

USDCAD continues to be underpinned due to yesterday’s tame inflation reading. The Bank of Canada’s CPI-trim (actual 2.9%) and CPI-median (actual 2.6%) inflation measures fell inside the 1-3% inflation target zone. It is the 4th consecutive drop, which suggests it may satisfy BoC policymakers’ desire to see a “sustainable trend lower.”

WTI oil prices dropped from 78.37 to 77.36 before rebounding to 78.09 in NY on the back of the API report showing US crude inventories rose by 2.5 million barrels in the week ending May 17. In addition, the US government is set to sell 1 million barrels of gasoline from its Strategic Petroleum Reserves.

There are no US or Canadian economic reports of note today.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3630 and looking to break above 1.3690 to extend gains to 1.3760. A move below 1.3630 suggests a retest of support at 1.3590.

The daily chart shows a well-entrenched uptrend line at 1.3550 which is guarded by support at 1.3590 which has been the floor for USDCAD since the April 10 BoC meeting when Governor Macklem broadly hinted at a June rate cut.

For today, USDCAD support is at 1.3630 and 1.3590. Resistance is at 1.3690 and 1.3730. Today’s range is 1.3610-1.3710.

Chart: USDCAD 4 hour

Source: DailyFX

Fed officials contradict market interest rate view.

The FOMC is united. Board of Governors and voting member Michael Barr warned that to finish the job on inflation, rates will need to be unchanged for longer than previously expected. Cleveland Fed President Loretta Mester noted that her estimate of the long-run neutral rate may not be as restrictive as she thought. Governor Christopher Waller said that the Fed needs to be confident in the data before they can think about cutting rates. Meanwhile, the CME’s FedWatch tool has a 60% probability of a rate cut in September. The FOMC minutes are due this afternoon. The volume of Fed officials talking about monetary policy since the May 1 meeting makes these minutes stale and of little value.

Equities are mixed

Asian equity indexes closed in negative territory except for the Shanghai Shenzhen CSI 300. Japan’s Nikkei 225 index fell 0.85%, while Australia’s ASX 200 index remained close to unchanged. European bourses are modestly lower, led by a 0.50% fall in the French CAC 40 index. S&P 500 index futures are down 0.17%, with the focus on Nvidia’s quarterly earnings report today.

EURUSD

EURUSD is trading defensively in a 1.0839-1.0864 range, weighed down by EURGBP sales and negative sentiment from China’s proposed tariffs on imported cars with large engines. Mercedes and BMW are most vulnerable, which is a reaction to EU plans to impose tariffs on Chinese electric vehicles.

GBPUSD

GBPUSD rallied in a 1.2705-1.2763 range, bolstered by higher-than-expected UK Services inflation data, which reduces the chances that the Bank of England cuts rates in June. Services inflation was 5.9% (forecast 5.4%) and above the BoE forecast of 5.5%. It wasn’t all bad. Headline CPI rose 2.3% y/y compared to 3.2% in March, which was a tick above the 2.1% expected. The intraday GBPUSD technicals are bullish, looking for further gains to 1.2810 while above 1.2705.

USDJPY

USDJPY inched higher in a 156.12-156.52 range, partly due to the modestly higher US 10-year Treasury yield, which is at 4.437%. Mixed Japanese economic data and 10-year JGB yields reaching 1.0% helped cap gains. Rising bond yields suggest that the BoJ may raise interest rates, with the odds for a July hike about 60%.

AUDUSD AND NZDUSD

AUDUSD traded uneventfully in a 0.6653-0.6686 range. AUDUSD is underpinned by a steep uptrend channel from April 19, which remains intact while prices are between 0.6630 and 0.6750.

NZDUSD rallied from 0.6090 to 0.6152 after the RBNZ monetary policy report but drifted back to 0.6123 by the NY open. The RBNZ left interest rates unchanged at 5.50%, but its outlook was more hawkish than expected. They do not expect that inflation will reach its 2.0% target until late 2025, early 2026, which will delay rate cuts until August 2026.

USDMXN

USDMXN consolidated yesterday’s gains in a 16.5926-16.6490 range overnight. Traders are cautious ahead of today’s FOMC minutes and Thursday’s Mexican inflation and GDP data. The USDMXN technicals are bearish, with the April 25 downtrend channel intact between 16.3800 and 16.7500.

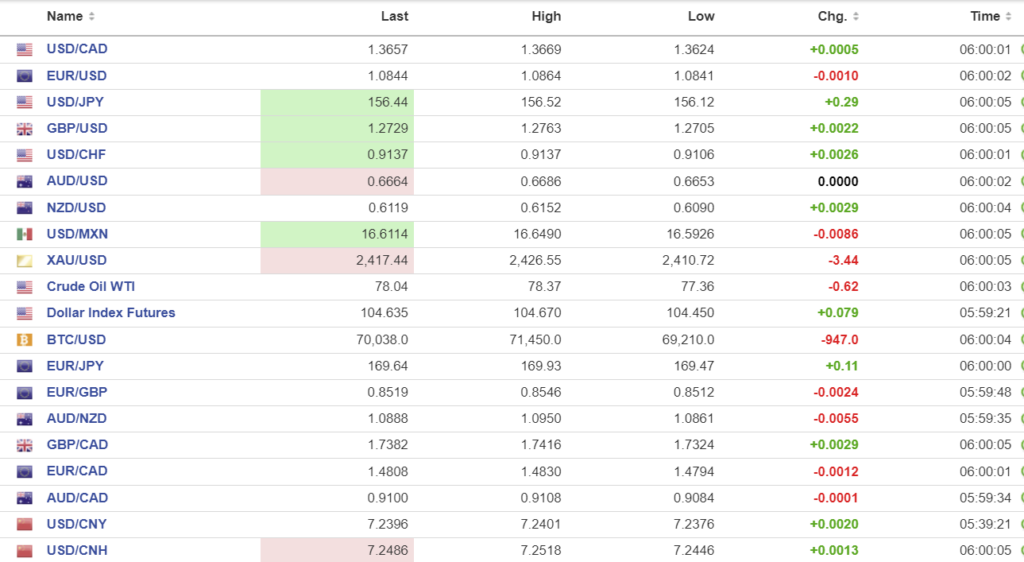

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

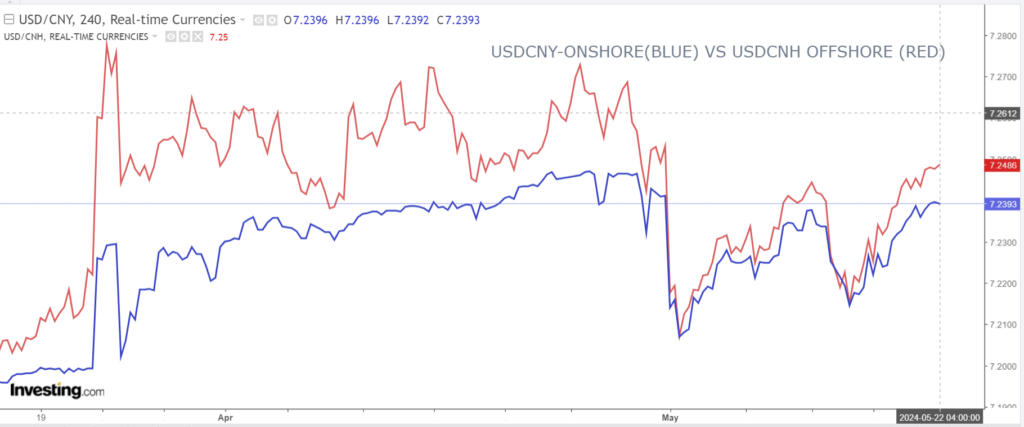

China Snapshot

PBoC fix: 7.1077 vs exp. 7.2376 (prev. 7.1069).

Shanghai Shenzhen CSI 300 rose 0.32% to 3684.45

Bloomberg reports that China is pondering tariffs as high as 25% on imported cars with large engines. It is thought to be aimed directly at EU carmakers (Mercedes, BMW) ahead of the EU releasing details of its probe into Chinese EV subsidies.

Chart: USDCNY and USDCNH

Source: Investing.com