September 5, 2024

- US ADP jobs fall to 99,000

- US recession risk talk heats up.

- US dollar sinks as bond yields fall.

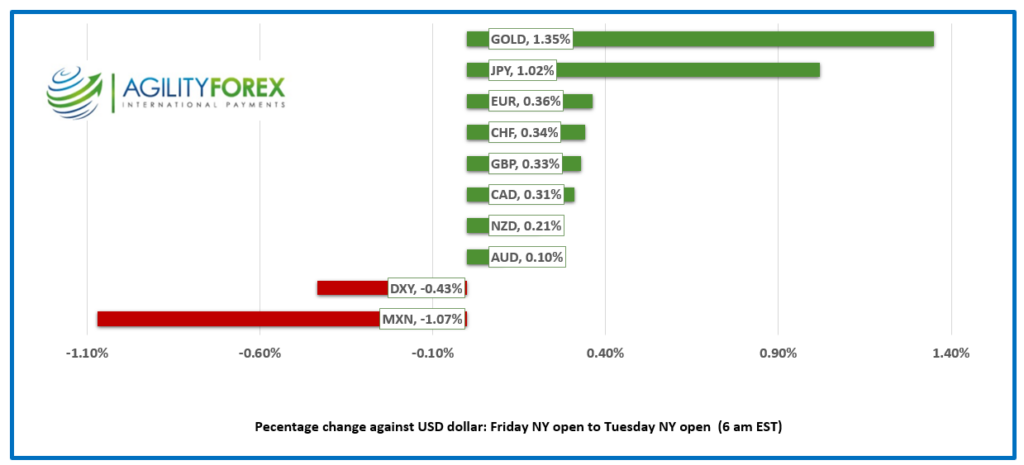

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3514, overnight range 1.3504-1.3517, previous close 1.3507

USDCAD dropped to 1.3500 from 1.3567 yesterday, then spent the overnight session consolidating the losses. The move occurred despite the Bank of Canada cutting the overnight rate by 25 bps to 4.25% and indicating that there was plenty of room for a series of additional rate cuts moving forward. The BoC rate cut was fully priced in but the CAD/US 10 year yield differential widened which undermined USDCAD.

Traders are focused on US employment data and the rising risk of a US recession. A US recession won’t be good news for Canada, due to the close trade relationship between the two countries. The Canadian economy, which is already sluggish will weaken further and it could be exacerbated if a US recession drags other G-10 economies down.

WTI oil dropped yesterday and then traded sideways in a 69.16-70.06 range overnight. Traders fear an oil glut because of Opec’s planned production increase on October 1, and weaker demand from China due to its ongoing economic slowdown. Now Opec is having second thoughts and are reportedly discussing a delay.

USDCAD technicals

The intraday USDCAD technicals are bearish below 1.3550 and looking to chop through support in the 1.3490-1.3500 area to extend losses to the 1.3440-60 support zone. A move above 1.3550 argues for more 1.3500-1.3600 range trading.

Longer term, the support line from the beginning of the year is intact above 1.3490 while Bollinger Bands suggest USDCAD is oversold.

For today, USDCAD support is at 1.3490 and 1.3460. Resistance is at 1.3550 and 1.3600. Today’s Range 1.3490-1.3550.

Chart: USDCAD 4 hour

Jolted by Jobs-Again!

Yesterday’s JOLTS survey delivered a real jolt to markets. Job openings fell to 7.673 million in July, significantly below the 8.1 million expected, with June’s numbers revised down to 7.91 million from 8.18 million. Bonds soared, and for the first time in over two years, the yield curve is no longer inverted. To many, this signals that a U.S. recession may be looming.

Recession fears were reinforced again this morning after ADP Employment change data showed the US only added 99,000 jobs in august, much lower that the 145,000 expected. However, a small dip in the number of jobless claims (actual 227,000 vs forecast 230,00 and previous 232,000) took some of the sting out. Nevertheless, the US 10-year yield fell to 3.73% from 3.77%.

The ISM Services Employment Index and ISM Services PMI data are also slated for release today.

EURUSD

EURUSD is slightly higher, trading in a 1.1075-1.1101 range ahead of today’s U.S. employment data. Traders shrugged off news that Eurozone Retail Sales rose 0.1% m/m in July, as the figure was in line with expectations. Attention is now turning to next week’s ECB monetary policy meeting. A 25 bp rate cut is fully priced in, but markets expect a dovish tone from both the statement and ECB President Christine Lagarde’s press conference.

GBPUSD

GBPUSD is choppy, fluctuating within a 1.3137-1.3172 range, with downward pressure driven by expectations that the Bank of England will accelerate the pace of rate cuts. The BoE Decision Maker Panel predicted a 3.5% rise in prices over the coming year, down from 3.7% last month, suggesting inflation is moving in the right direction.

USDJPY

USDJPY extended yesterday’s losses, trading in a 143.05-143.91 range, after the U.S. dollar was hit hard when the JOLTS report showed vacancies dropping to their lowest level since the pandemic. The decline in the U.S. 10-year Treasury yield to 3.75% from 3.84% added momentum to the move.

AUDUSD and NZDUSD

AUDUSD traded in a narrow 0.6714-0.6734 range, showing little reaction to the release of Australia’s trade balance (actual 6.009b, forecast 5.15b, previous 5.42b) or comments from RBA Governor Bullock. She reiterated that it’s premature to discuss rate cuts and didn’t foresee the RBA cutting rates in the near term.

NZDUSD traded quietly in a 0.6179-0.6209 band, supported by broad-based bearish sentiment towards the U.S. dollar.

USDMXN

USDMXN was bid, rising from 19.9237 to 20.0550 before settling around 20.0268 in New York. Traders and the U.S. government are uneasy with Mexico’s judicial reforms, which will allow judges to be elected, among other controversial changes. The bill passed the lower house yesterday. Short-term technicals suggest the break above 20.000 paves the way for further gains, potentially targeting 22.0000.

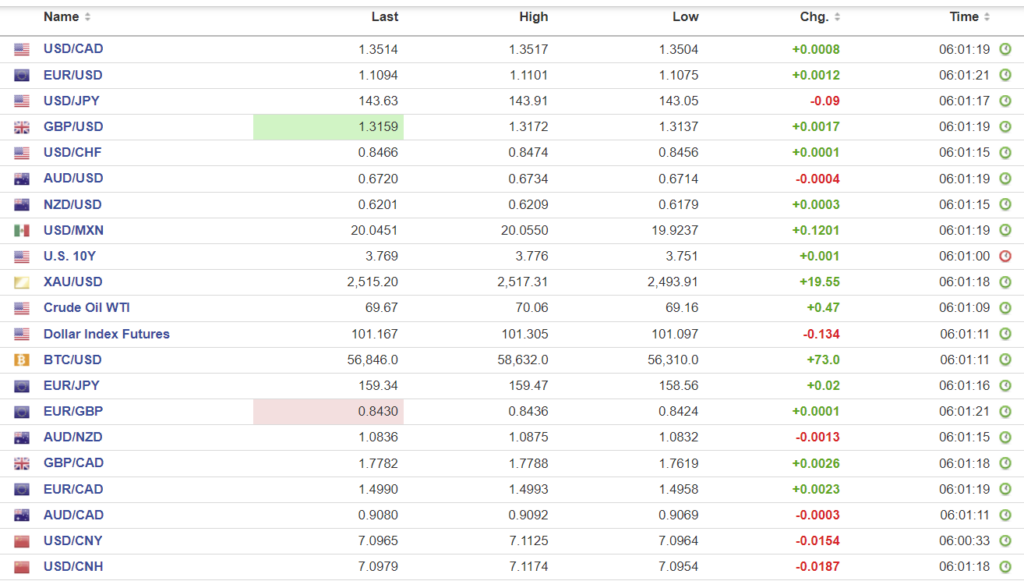

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0989 vs exp. 7.1010 (prev. 7.1148).

Shanghai Shenzhen CSI 300 rose 0.17% to 3257.76

Parts of Southern China, and Hong Kong are bracing for Super Typhoon Yagi

Goldman Sachs is prediction a 25 bp cut in RRR rate in September and a further 10 bps in the fourth quarter. PBoC Head of Monetary Policy Zou Lan, kind of agrees with the Goldman forecast. He said there’s still space for more cuts considering the average reserve requirement ratio for financial institutions is at about 7%.

Meanwhile, JPMorgan cuts Chinese stocks from overweight to neutral due to the possibility or renewed US China tariff wars.

Chart: USDCNY and USDCNH

Source: Investing.com