November 15, 2019

USDCAD open 1.3248-51 (6:00 am EST) Overnight Range 1.3221-1.3250

The US dollar barely budged when October Retail Sales, Empire State Manufacturing Index, and Import/Export price data was released. None of the reports did anything to move Fed chair Jerome Powell away of his “wait and see” interest rate policy.

The US dollar dropped against the commodity currencies in Asia, recouped those losses in Europe and opened in New York with tiny gains against the majors except CAD and EUR which were unchanged. The US dollar is poised to finish the week on a down note. It posted losses against the G-10 majors except for CAD and AUD, compared to last Friday’s closing levels.

FX Market Snapshot

Change in currency value against the US dollar from NY close Nov 8 to NY open Nov 15

Source: IFXA/Saxo Bank

Hopes for an imminent announcement of a US/China trade deal, lifted equity indices and the commodity bloc currencies, in Asia. That’s because White House Economic Advisor Larry Kudlow said as much on Thursday. He told reporters that the two sides were getting close to an agreement and President Trump “likes what he sees.” A Financial Times article begged to differ, throwing cold water on those hopes. It said the two sides were struggling to complete Phase 1 because of differences of intellectual property rights, agricultural purchases and tariff rollbacks. It quoted “people close to the talks” saying the Americans are frustrated because China is not offering enough concessions.

EURUSD traded quietly, again. The single currency drifted in a 1.1016-28 range, and even Eurozone trade and inflation data couldn’t spark any enthusiasm. The Eurozone trade balance, non-seasonally adjusted, widened to €18.7 billion from €14.7 billion, while October CPI was weaker than expected. (Actual 0.1% vs forecast 0.2%)

GBPUSD trading was almost as quiet as Euro trading. Prices dipsy-doodled in a 1.2829-1.2886 range with traders focused on the UK election.

USDJPY traded with a negative bias overnight and in early New York trading. The sellers were spooked by the escalating violence in the Hong Kong and fears of a heavy-handed response by China. Prices were also weighed down by this week’s drop in 10-year US Treasury yields which dropped from 1.956% on Monday, to 1.846% this morning.

NZDUSD continues to consolidate gains from Wednesday after the RBNZ surprised markets and left interest rates unchanged. Prices were underpinned in Asia after Business NZ PMI was 52.6 in October, compared to 48.4 in September. NZDUSD has recouped all the early Eurozone losses which occurred on the FT story. AUDUSD tracked NZDUSD moves.

Oil prices extended yesterday’s losses after the EIA reported US crude inventories rose 2.219 million barrels last week. The European based International Energy Agency (IEA) predicted that in 2020,non-Opec crude supply would surge by 2.3 million barrels per day, while demand would fall. WTI dropped from $57.67/b yesterday to $56.63 in New York today.

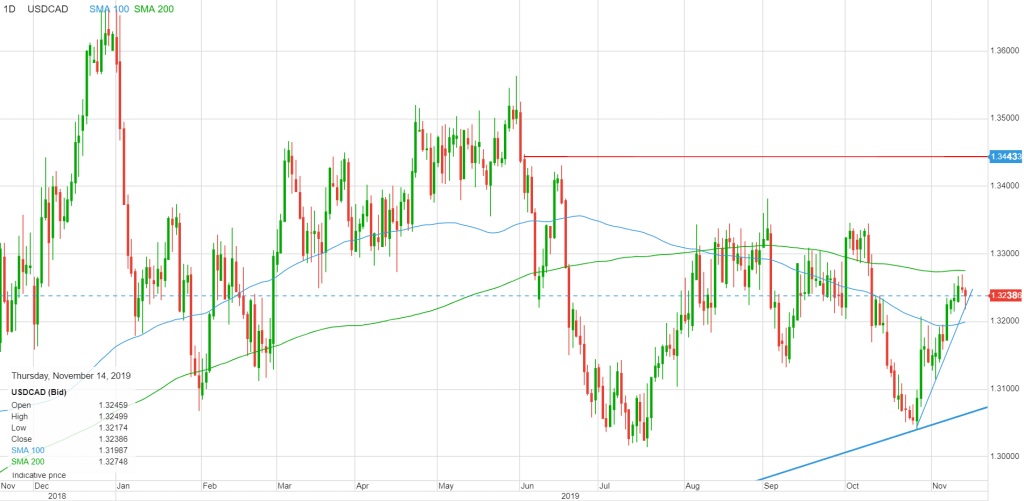

USDCAD tracked the commodity currency bloc moves. Support at 1.3220 was tested, and it held. However, the loss of upward momentum, and the failure to break resistance in the 1.3270-80 area, shifted the focus to the downside. Rising hopes for a US/China trade deal and expectations that the Bank of Canada will leave rates unchanged at its December 4 meeting are weighing on prices.

USDCAD Technical View

The intraday USDCAD technicals are bullish while prices are above 1.3205, a level guarded by support at 1.3220. Resistance is between 1.3270 and 1.3290, with a a topside break targeting 1.3340. Prices continue to bounce between the 100 day and 200 day moving averages. For today, USDCAD support is at 1.3220 and 1.3190. Resistance is at 1.3270 and 1.3290. Today’s Range 1.3220-1.3270

Chart: USDCAD daily with 100 and 200 day moving averages noted

Source: Saxo Bank