Photo: Bing AI

October 18, 2023

- China Q3 GDP 4.9% y/y, tops expectations.

- US 2nd tier data and speeches from four Fed officials ahead.

- US dollar drifts lower ahead of Fed Chair Powell’s speech tomorrow.

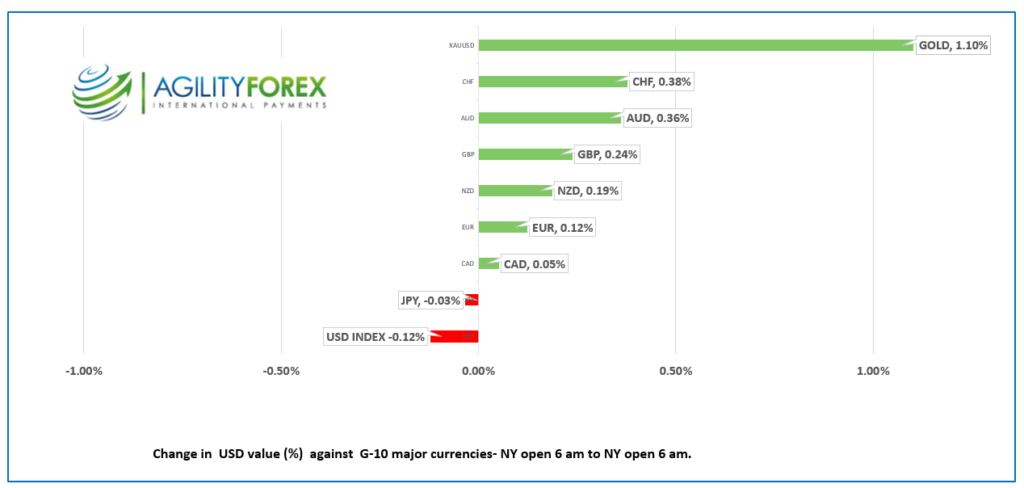

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3623-27, range 1.3617-1.3667, close 1.3651

USDCAD mirrored broad G-10 currency moves yesterday and traded in a similar fashion overnight. Yesterday’s Canadian CPI report provided fodder for bulls and bears. The headline data showed inflation cooling in September but the BoC “super core measure” which excludes shelter from core-CPI firmed to 4.3% y/y on a three-month average. The inflation data will be spun to suit whatever action the BoC decides with many analysts suggesting no action will be taken.

WTI oil prices jumped to $88.57/b from $86.31 due to fears that the Gaza hospital bombing will escalate tensions. Traders ignored the 4.38 million drop in US crude inventories, chalking it up to a correction following two weeks of sizeable increases. Prices retreated back to $87.00/b in NY.

Canada September Housing starts rose 3.9% compared to August.

USDCAD Technicals

The intraday USDCAD technicals flipped from bearish to bullish in NY trading after prices rose above the overnight peak of 1.3655 and snapped the two-week downtrend line with the move above 1.3660. The reality is that the price action is just noise in the context of the 1.3580-1.3700 range which has prevailed for the past week.

Meanwhile the October uptrend line is intact above 1.3610 which guards the July uptrend line which resides at 1.3480.

For today, USDCAD support is at 1.3610 and 1.3580. Resistance is at 1.3670 and 1.3700. Todays Range 1.3620-1.3700

Chart: USDCAD monthly

Source: Investing.com

G-10 FX recap

Yesterday, negative risk sentiment from the war in the Middle East and yesterday’s robust US retail sales data was not enough to completely sour positive vibes from US earnings, which has put some downward pressure on the US dollar. That changed today when earnings from Morgan Stanley (NYSE: MS), JB Hunt (NASDAQ: JBHT) and Citizens Financial (NYSE: CFG) fell short of expectations.

Asian equity markets closed with the Japanese Nikkei 225 index up a mere 0.7%, and Australia’s ASX 200 gaining 0.30%. European bourses are down across the board, partly because the 10-year US Treasury yield is firmer at 4.868%. Gold is enjoying a haven bid and gained over 1.0%, and has risen over 7.5% in 12 days.

EURUSD traded quietly and is at the bottom of its 1.0557-1.0595 range. Eurozone final HICP was as expected at 0.3% m/m and 4.3% y/y and had little impact on trading. The EURUSD technicals are bearish below 1.0620, looking for a move to 1.0400.

GBPUSD rose from 1.2184 at the NY close to 1.2212 in Europe after September UK inflation rose more than expected (actual monthly CPI 0.5% m/m forecast 0.4%, actual annual 6.7% forecast 6.5%, and Core-CPI 6.1% vs forecast 6.0%). PPI and the Retail Price index were also higher than forecast. Despite the rise in inflation, many economists are saying that the increase isn’t enough to cause the Bank of England to raise interest rates. The intraday GBPUSD technicals are bullish above 1.2170, looking for a break above 1.2230 to target 1.2320. A move below 1.2170 will extend losses to 1.2110.

USDJPY drifted in a 149.50-149.75 band with prices supported by expectations that the Fed keeps rates “higher for longer,” while the risk of Bank of Japan intervention above 150.00 limits gains.

AUDUSD traded with a bit of a bid, rising from 0.6351 to 0.6393, following stronger than expected Chinese data and broad-based, but minor US dollar selling pressure. RBA Governor Michelle Bullock said, “What we are observing is that monetary policy is starting to bite. We are seeing a slowdown in consumption.” She also noted commented on sticky inflation saying, “The problem is that we’ve got shock after shock after shock, and the more that keeps inflation elevated, even if it’s a supply shock, the more people adjust their thinking, the more entrenched inflation is likely to become, so that’s the challenge.”

Today Fed policymakers Christopher Waller, John Williams, Michelle Bowman, and Lisa Cook are talking.

FX high, low, open

China Snapshot

Bank of China Fix: today 7.1795, expected 7.3079, previous 7.1796.

Shanghai Shenzhen CSI 300 fell 0.77% to 3610.58.

China Q3 GDP 1.3% q/q (forecast 1.0%), 4.9% y/y (forecast 4.4%)

September Retail Sails 5.6% (forecast 4.9%) Industrial Production 4.5% (forecast 4.3%)

All Chines data releases should be prefaced by the words “Once upon a time… as it is mostly fairy-tale wishes by policymakers.

”Soren Aandahl, a noted short-seller of Hong Kong listed stocks via Blue Orca Capital LLC described China as “a completer black hole of investment information.” The State limits investor access to basic corporate metrics and has a penchant for arrest business leaders it doesn’t like.

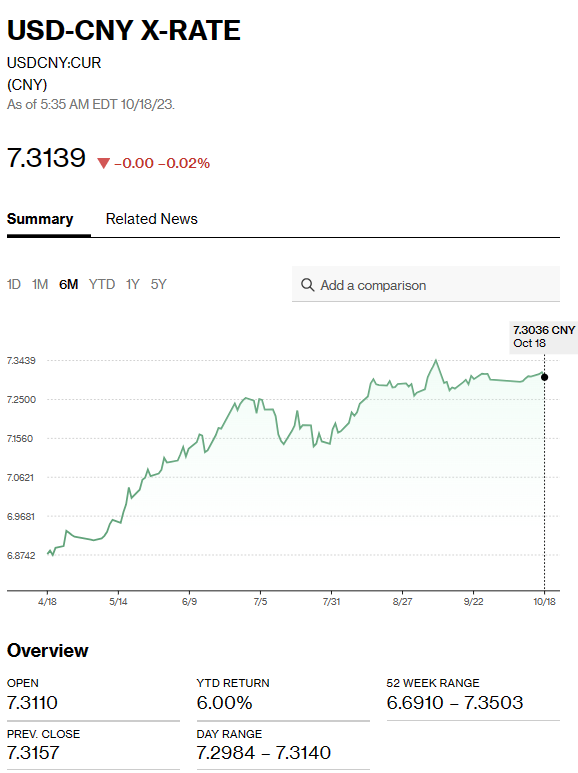

Chart: USDCNY 6 month

Source: Bloomberg