January 5, 2024

- NFP surges 216,000 and cools rate cut fever.

- Canada employment flat-lines-no new jobs.

- US dollar opens with gains overnight and post FOMC.

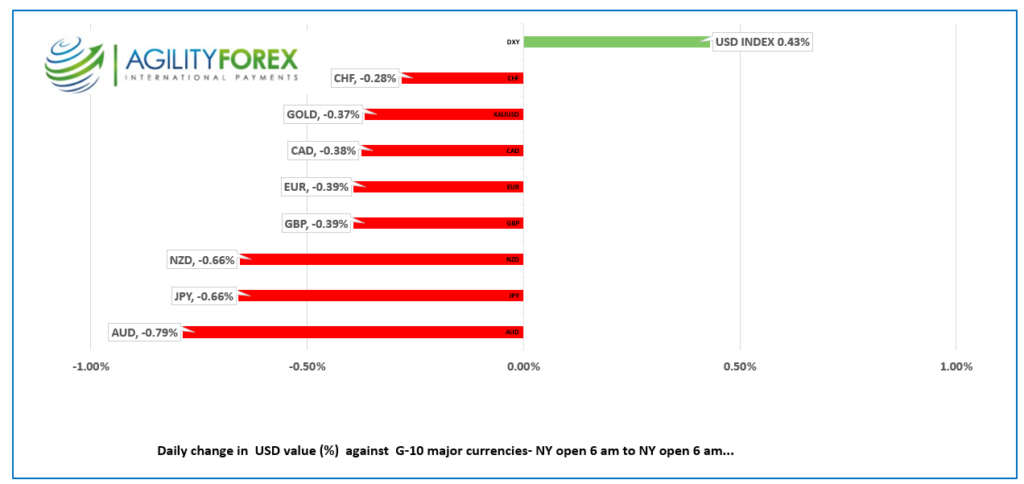

FX at a glance

Source: IFXA

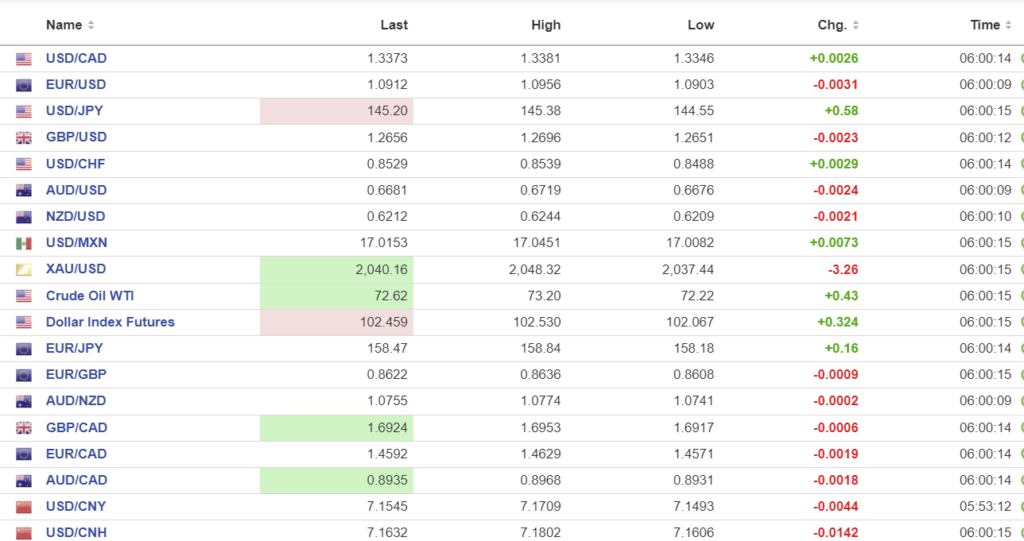

USDCAD Snapshot: open 1.3371-75, overnight range 1.3346-1.3399, close 1.3349.

USDCAD traded in a 1.3317-1.3367 range yesterday and then squeezed out more gains overnight and touching 1.3599 following the Canadian and US employment reports. The US headline jobs number was better than expected while Canada’s number disappointed.

Most disconcerting for Bank of Canada officials is that Average hourly wages jumped to 5.7% y/y from 5.0% in November, which is nearly triple the BoC’s inflation target of 2.0%. The results will not force a rate hike but they do ensure rate cuts will not be happening any time soon.

USDCAD gains quickly faded and prices returned to pre-data levels within 25 minutes.

WTI oil prices churned in a $72.22-$73.20 range. US dollar gains more than offset supply disruption concerns and the risk of further Opec production cuts.

USDCAD Technicals:

The intraday USDCAD technicals are bullish and in a minor uptrend with 1.3300 on the bottom and 1.3410 on the top, which is also resistance from previous tops stretching back to December 14. A move below 1.3300 targets 1.3190 while a move above 1.3430 targets 1.3550.

Longer term, the downtrend line from mid-November comes into play at 1.3430 (4 hour chart).

For today, USDCAD support is at 1.3330 and 1.3290. Resistance is at 1.3410 and 1.3440. Todays range 1.3310-1.3410.

Chart: USDCAD 4 HOUR.

Source: Daily FX

G-10 FX

US Nonfarm payrolls rose by 216,000, average hourly earnings rose by 0.1% to 4.1% y/y while the unemployment rate was unchanged at 3.7% (forecast 3.8%). The news threw cold water on those expecting a rate cut by March, as the data indicates “higher for longer.” The CME FedWatch tool downgraded the odds for a March rate cut to 55% from 75% a week ago and confirming the hawkish bias to Thursday’s data.

Yesterday, the US dollar rallied, stocks fell, and Treasury yields rose following yesterday’s Challenger job cuts, ADP employment and initial jobless claims data. The reports pointed to a fairly healthy labour market which suggested that Fed rate cuts will not be as aggressive as expected. Of course, as Bloomberg’s John Authers pointed out in a column today, data-dependent central banks rely on the data, and the data is suspect. He pointed out that the JOLTS data in particular is suspect due to the ever dwindling number of participants responding to the survey.

Geopolitical tensions may have also contributed to the US dollar’s overnight strength. The US warned Houthi rebels that if attacks on Red Sea shipping continued, the US would strike Houthi strongholds in Yemen. The rebels responded by detonating an unmanned vessel within a couple of miles of commercial and US Navy ships.

EURUSD dropped below its overnight session low and reached 1.0877 in the wake of the jobs data, but quickly reversed the move. EURUSD traded with a negative bias overnight in a 1.0903-1.0956 range and did not garner any support after Eurozone inflation rose to 2.9% from 2.4% y/y in November. The reduction in government subsidies for gas, electricity, and food fueled the gains. In addition, Eurostat reported, “Industrial producer prices fell by 0.3% in the euro area and by 0.2% in the EU, compared with October 2023.” Today’s data suggests that the ECB will not be in any hurry to cut interest rates this quarter.

GBPUSD dropped to 1.2611, post-NFP, after trading in a 1.2651-1.2696 range overnight. Minor support from higher housing price data faded. A former BoE deputy governor and current chair of NatWest Group, Howard Davies, warned that the BoE missed the boat when inflation rose and will probably be too slow to react when it falls.

USDJPY traded with a bid, rising from 144.55 to 145.38 overnight, then spike to 145.98 when the US 10-year Treasury yield spiked to 4.10% after the jobs data from 4.044% where it opened.

AUDUSD dropped to 0.6641 after todays data then recovered just as quickly and is in the middle of its overnight 0.6676-0.6719 range.

US ISM Services PMI is expected at 52.6, compared to 52.7 in November. Factory orders are expected to have risen 2.1% in November, compared to the 3.6% decline in October.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1028,expected 7.1593 previous 7.0997.

Shanghai Shenzhen CSI 300 fell 0.54% to 3329.11.

Bloomberg reports that Zhongzhi Enterprise Group filled for bankruptcy claiming it is insolvent. The so-called “shadow bank” pools savings from individuals to provide loans for real estate, stocks and bonds and to developers.

Chart: USDCNY and USDCNH 4-hour

Source: Investing.com