Photo: Wikimedia

- US Durable Goods unchanged in July

- Fed-speak warns of higher rates

- US dollar retreats, modestly

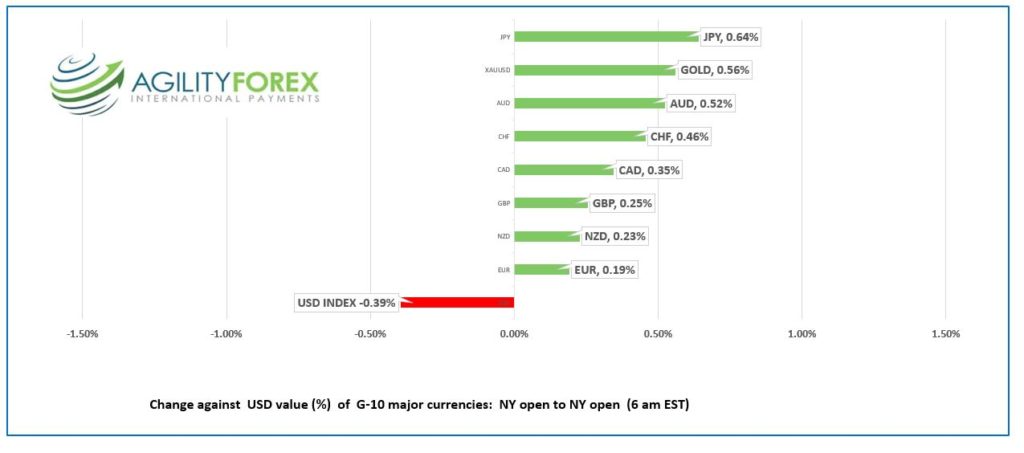

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.2974-78, overnight range 1.2946-1.3000, close 1.2958

It was another slow news day and even pipe dreams were covered like newsworthy events

The CBC trumpeted “Hydrogen alliance formed as Canada Germany sign agreement on exports.” Justin Trudeau and German Chancellor described it as a “joint declaration of intent.” The devil is in the details.

The plan is to convert wind energy from wind turbines that don’t exist, to hydrogen using an expensive new technology, in a plant that doesn’t exist, then export liquified hydrogen to Germany, somehow.

Traders ignored the news because, well, it wasn’t news. It merely an exercise in political theatre, which is what you get when you get a second-rate drama-teacher for a Prime Minister.

WTI oil prices continued to climb from Monday’s low, rising to $95.19/barrel overnight. Prices were supported by talk that Opec would consider cutting production if Iran oil came on stream.

USDCAD tested support in the 1.2940 area yesterday then drifted higher overnight, in tandem with broad US dollar moves. FX traders are awaiting Fed Chair Powell’s speech on Friday, and until then, USDCAD will churn in a 1.2940-1.3050 band.

USDCAD Technical outlook

The hourly and 4-hour USDCAD technicals are bullish above 1.2950, looking for a break above 1.3010 to extend gains to 1.3050. Longer term, the 1.2740-1.3080 range remains intact. A topside break targets 1.3220, while a move below 1.2740 suggests a test of support at 1.2680, then 1.2540.

For today, USDCAD support is at 1.2940 and 1.2910. Resistance is at 1.3010, and 1.3030. Today’s range: 1.2940-1.3030

Chart: USDCAD hourly

Source: Saxo Bank

G-10 FX recap and outlook

The countdown to Fed Chair Powell’s Jackson Hole speech has sapped the lifeblood out of markets. Traders are reacting to second and third-tier data like it is meaningful. Case in point-the US dollar was sold after S&P Global PMI reports were weaker than expected in the US. However, although S&P data is critical in Europe and the UK, in the US, the ISM Manufacturing reports are the benchmark for US activity.

Cleveland Fed President Neel Kashkari reminded markets that “there was no trade off between employment and inflation mandates.” He said the Fed can only relax when they see compelling evidence inflation is heading to 2.0%.

US Durable Goods Order were unchanged in July, while the June results were revised higher to 2.2% from 2.0%.

Source: US Census Bureau

Asian equity indexes closed lower, with China’s Shenzhen CSI 300 dropping 1.89%. Australia’s ASX200 index was the outlier, gaining 0.52%.

European bourses are mixed but not far from unchanged while Wall Street futures are flat. Gold prices slipped while WTI rose, both marginally.

EURUSD is trading defensively in 0.9918-0.9972 range but not getting any benefit from expectations of higher ECB rates. Bloomberg reports traders have priced in a 100% chance that the ECB will raise rates by 100 basis points in October,

GBPUSD is trading at its overnight low of 1.1770 after dropping from 1.1837. The worsening UK economic picture has driven rate hike expectations to 3.5% by year end, double what analysts expected just ten days ago.

USDJPY traded in a 136.18 -137.03, overnight but prices have slipped to 136.90 in NY despite the US 10-year Treasury yield grinding higher to 3.076% from 3.038% in Europe.

AUDUSD slipped to 0.6883 from 0.6930 due to renewed US dollar demand as Treasury yields inched higher.

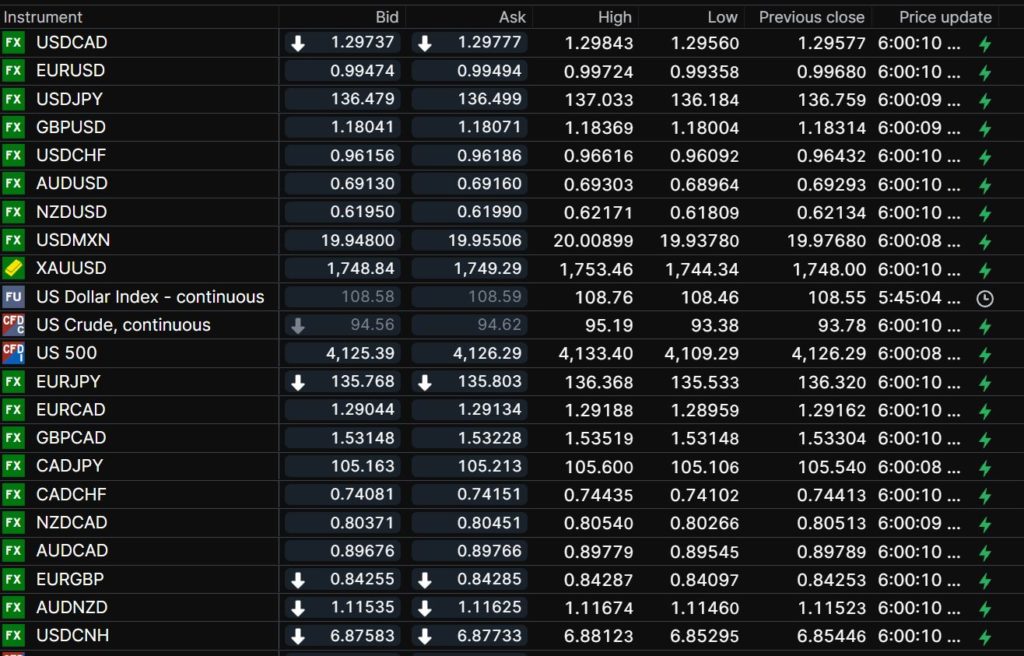

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

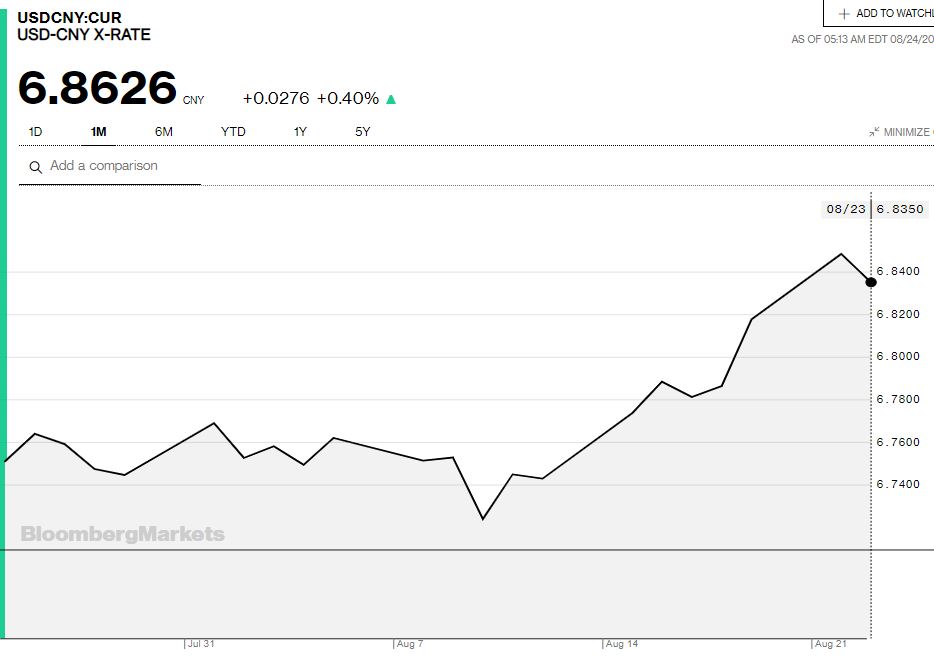

China Snapshot

Today’s Bank of China Fix: 6.8388, previous 6.8523

Shanghai Shenzhen CSI 300 fell 1.89% to 4,082.42

Chart: USDCNY 1 month

Source: Bloomberg