Photo: HDClipart.com

- GBPUSD sinks as economy shrinks

- Markets and Fed diverge on US rate hike outlook

- US dollar opens mixed-JPY weakest

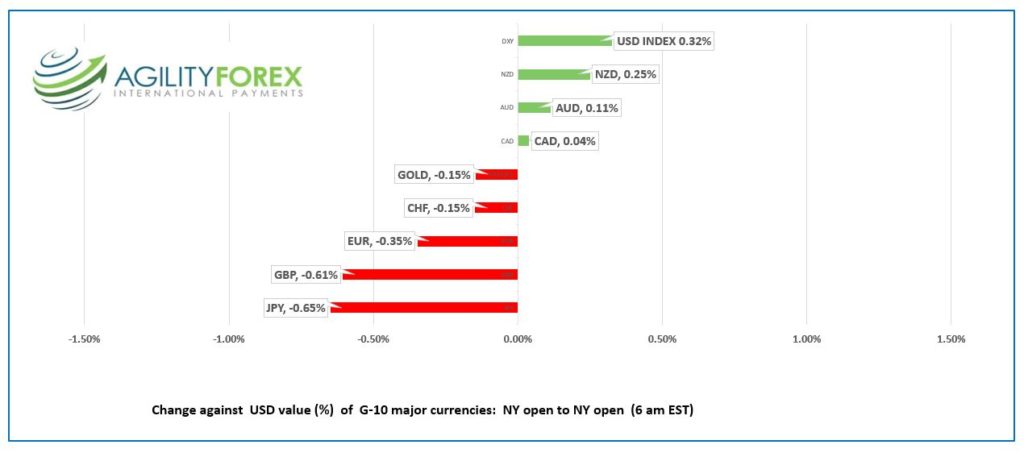

FX at a glance:

Source: IFXA Ltd/RP

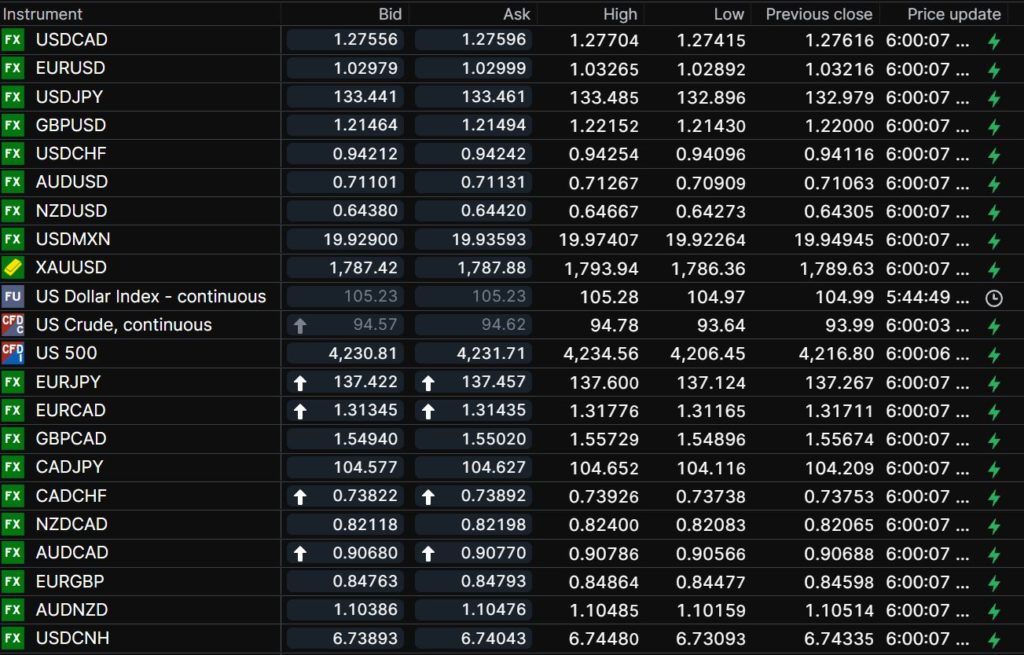

USDCAD Snapshot: open 1.2756-60, overnight range 1.2742-1.2788, close 1.2762

USDCAD tested support in the 1.2720-30 area yesterday, but sellers were beaten back when the S&P 500 index retreated. The currency pair is at the mercy of ever-shifting intraday risk sentiment. Traders will need to wait until Wednesday for some domestic direction, when July CPI is released. It is expected to have dropped from 8.1% to 7.7% due to lower oil prices. The question is “Will it dissuade the BoC from raising rates by 0.75% at the September meeting? The answer is “no.”

WTI oil prices rallied steadily since Tuesday but profit-taking, but mixed Opec and IEA outlooks are weighing on prices this morning. Opec cut its forecast for global oil demand in 2022 by 260,000 b/day, which is really a drop in the barrel as daily production is 100.03 million barrels/day.

The Paris-based International Energy Agency (IEA) begs to differ. They said the heatwave in Europe boosted demand as high prices for natural gas encouraged a switch to oil. The IEA also noted that Western sanctions on Russian oil have barely made a dent into Russia’s production. They said Russia shifted oil exports from Europe to India and China.

The Canadian economic calendar is empty.

USDCAD Technical outlook

The USDCAD technicals are bearish with the downtrend from the July 14 peak intact while prices are below 1.2910. There is strong support in the 1.2720-40 area which if broken will extend losses to 1.2670. A move above 1.2830 targets 1.2910.

For today, USDCAD support is in the 1.2740 area, then 1.2705. Resistance is at 1.2790 and 1.2840. Today’s range: 1.2740-1.2820

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The late Steve Jobs had a talent described as a “Reality Distortion Field.” According to Wikipedia, the term was used to describe Mr Job’s ability to convince himself and others to believe almost anything using a mix of charm, charisma, bravado, hyperbole, marketing, appeasement, and persistence.”

Financial markets are experiencing a reality distortion field of their own. Bond and equity traders have decided that small dips in CPI, PPI, and PCE are evidence that inflation has peaked, which will allow the Fed to slow the pace of rate hikes in 2022 and then cut rates in early 2023.

Fed policymakers disagree, complaining that they haven’t seen any convincing evidence of an inflation peak and that “lots more work is needed” before the inflation beast is tamed.

Market sentiment appears to be that the Fed’s inflation outlook was wrong at the start, so why believe them now.

The Japanese Nikkei 225 index surged 2.62% in Asia, while Australia’s ASX 200 fell 0.4%. European bourses opened flat but have eked out modest gains, with the German Dax up 0.55%. Oil and gold prices are modestly lower compared to the NY close.

The US 10-year Treasury yield rose from 2.74% to 2.891% and consolidated the gains in a 2.86-2.888% range overnight.

EURUSD traded defensively in a 1.0272-1.0327 range with the bottom found in NY. Germany’s Economics Minister warned that the second half outlook was considerably worse due to supply disruptions and energy woes. And to rub salt into the wound, the Rhine River is almost unnavigable due to low levels which may disrupt fuel deliveries in the region. EURUSD found support after Industrial Production rose 0.7% m/m in June. The EURUSD technicals are bullish above 1.0200 but need to break above the long-term downtrend line at 1.0450 to avoid retesting the lows.

GBPUSD traded negatively in a 1.2112-1.2215 range, with prices weighed down by fears the UK economy is in a recession. Q2 GDP fell 0.1% q/q compared to 0.8% in Q1. The result was better than expected, but that didn’t help GBPUSD, especially after the National Institute of Economic and Social Research (Niesr) suggested a recession had landed. Traders ignored a host of other economic data (Manufacturing Production, Industrial Production, Total business Investment, Trade Balance), which were better than expected. Nevertheless, the GBPUSD July uptrend is intact above 1.2090.

USDJPY is at the top of its 132.90-133.89 overnight range on the surge in US Treasury yields.

NZDUSD rallied from 0.6427 to 0.6467 after better than expected Business NZ PMI and a jump in the Food Price Index to 2.1% m/m compared to 1.2% in June.

AUDUSD traded in a 0.7087-0.7127 range, with the gains lagging NZDUSD after Australian New Home Sales drooped 13.1% in July.

The Michigan Consumer Sentiment Index (forecast 52.5 vs 51.5 in July) is due today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

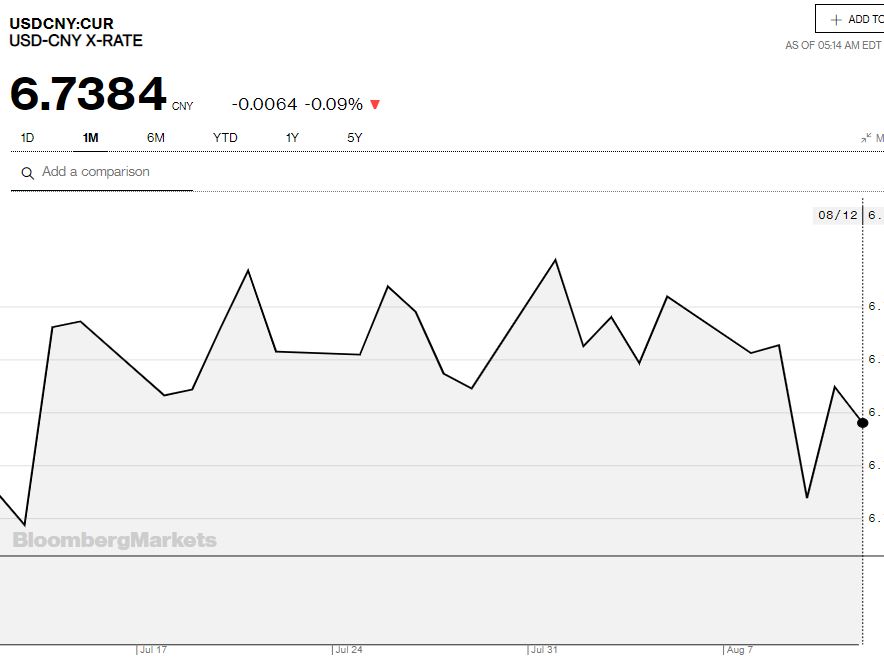

China Snapshot

Today’s Bank of China Fix: 6.7413, previous 6.7324

Shanghai Shenzhen CSI 300 fell 0.06% to 4,191.15

Chart: USDCNY 1 month

Source: Bloomberg