May 31, 2024

- PCE deflator inches lower as expected.

- Canada’s economy lives up to expectations-flat growth.

- US dollar and Trump are licking wounds.

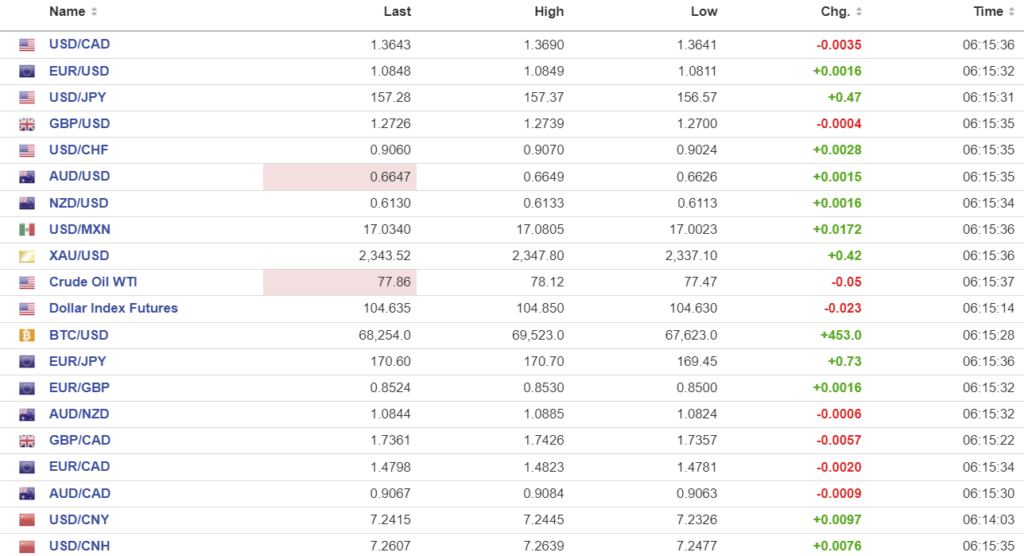

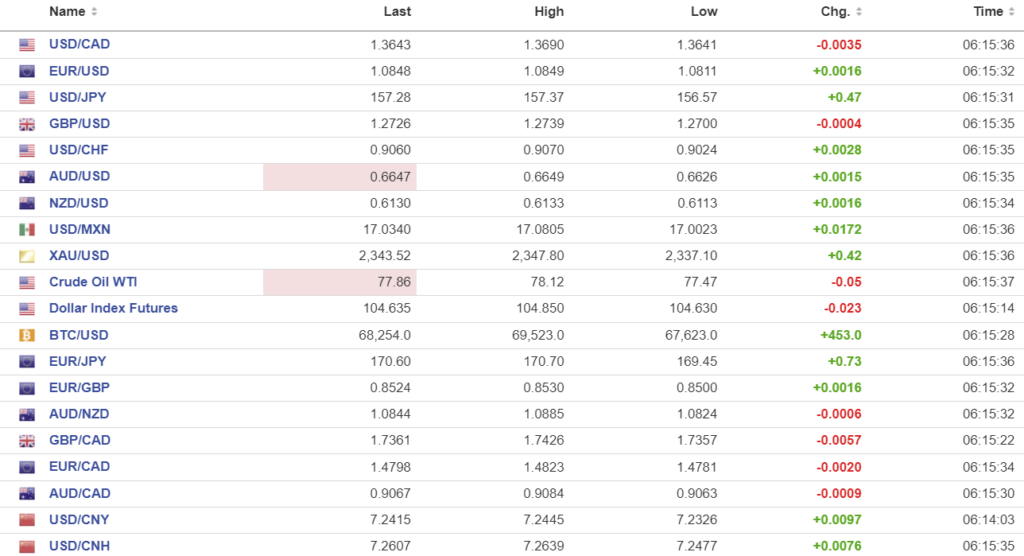

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3646, overnight range 1.3630-1.3690, close 1.3679

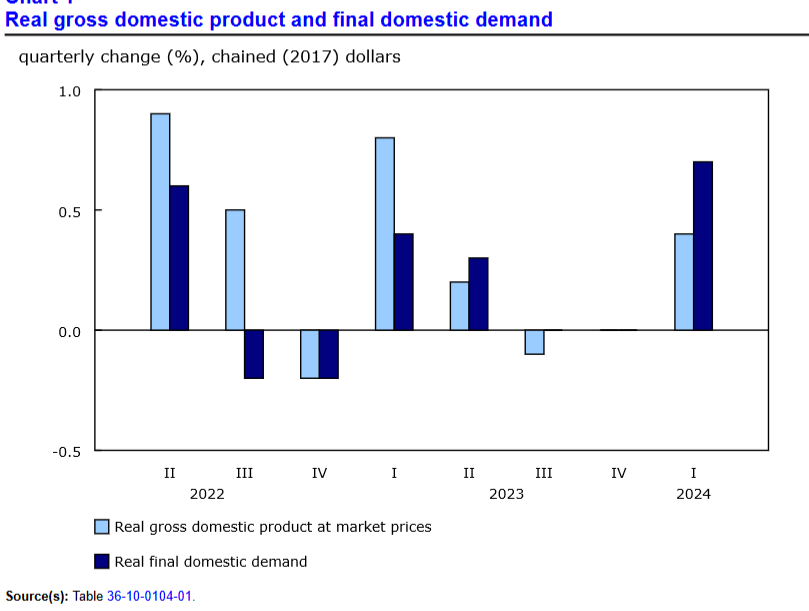

The Canadian economy did not grow in March, which was expected but it rose 0.4% q/q in Q1 and 1.7% y/y. Statistics Canada said, “In the first quarter of 2024, higher household spending on services was the top contributor to the increase in GDP, while slower inventory accumulations moderated overall growth.”

Source: Statistics Canada

USDCAD popped on the news, but the gains were small because the US PCE deflator data was weaker than last month, as expected, and the rally has already been reversed.

WTI oil traded defensively in a 77.47-77.12 range overnight as China’s weak soft PMI data overshadowed the EIA report that US crude inventories fell by 4.15 million barrels last week Things changed after today’s US data and WTI rallied to 78.62. OPEC is expected to announce an extension to production cuts until the end of 2024 on Sunday.

It is also month-end and portfolio rebalancing flows may also be weighing on USDCAD.

USDCAD Technicals

The intraday USDCAD are bearish below 1.3670 and looking for a break of support at 1.3610 to extend losses to 1.3550. A break above 1.3770 puts the focus back on 1.3750.

The longer term technicals are bearish with the downtrend from the middle of April intact while prices are below 1.3730. The January uptrend line is intact above 1.3590.

For today, USDCAD support is in the 1.3590-1.3610 area and 1.3550. Resistance is at 1.3670 and 1.3710. Today’s range is 1.3610-1.3710.

Chart: USDCAD daily

Source: DailyFX

Deflator Deflates Dollar

Financial markets got a more pleasant surprise from today’s data than Donald Trump got from the jury verdict. The former president was convicted on all 34 charges of falsifying business records in the first degree. He was a tad unhappy. Traders were far happier with today’s PCE data, mainly because the results didn’t change anything about the current debate on the timing of the first Fed rate cut. The PCE deflator rose 2.7% year-over-year, unchanged from March while Core PCE rose 2.8% as expected.

Provocation and Escalation?

The US has reportedly supplied Ukraine with weapons capable of striking targets inside Russia and Berlin has agreed to let Ukraine use German-supplied weapons as well. NATO Secretary General Jens Stoltenberg said to the G-7 Foreign Ministers that NATO will play a bigger role in supporting Ukraine. Now, the question is: who will be the 2024 version of 1914’s Archduke Franz Ferdinand?

EURUSD

EURUSD climbed steadily, rising from 1.0811 in Asia to 1.0880, post PCE. Earlier prices were supported by Eurozone HICP data (actual 2.6% year-over-year, forecast 2.5%, previous 2.4%). Today’s data shouldn’t derail the expected June ECB rate cut but does suggest that cut will be of the hawkish variety.

GBPUSD

GBPUSD rose from 1.2700 to 1.2750 after the US data. UK house prices rose 0.4% month-over-month in May and 2.7% year-over-year but the news was not a factor.

USDJPY

USDJPY returned close to yesterday’s peak, rising from 156.57 in Asia to 157.37. That move was erased in the wake of the US PCE report after the 10-year Treasury yield dropped from 4.55% to 4.50%. Japanese data was mixed. April Industrial Production fell 0.1% (forecast 0.9%) but inflation was firm and retail sales were higher than forecast. Tokyo CPI rose 2.2%, as expected, while April Retail Sales rose 2.4% year-over-year (forecast 1.9%). In addition, the Japanese labor market remains tight with the unemployment rate at 2.6%. ING analysts suggest that today’s data supports a BoJ rate hike in July.

AUDUSD and NZDUSD

AUDUSD rallied from 0.6626 to 0.6668 due to broad US dollar weakness. Gains were slowed by the soft Chinese PMI results. NZDUSD tracked AUDUSD gains and rose from 0.6113 to 0.6157. RBNZ Governor is in a bit of a bun fight with a group called the New Zealand Initiative whose members include the four biggest banks. They are particularly annoyed with the RBNZ decision to raise bank capital requirements.

USDMXN

USDMXN is choppy in a 17.0023-17.0805 range and trading but dropped to 16.9190 as the risk of higher for longer US rates eased somewhat. Mexico’s jobless rate was 2.6% in April, up from 2.3% in March.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1111 vs expected 7.2623 (prev. 7.1106)

Shanghai Shenzhen CSI 300 fell 0.40% to 3579.92.

NBS May Manufacturing PMI, 49.5 vs. forecast. 50.4, previous. 50). Non-Manufacturing PMI 51.1 vs. forecast 51.5. previous 51.2.

Chart: USDCNY and USDCNH

Source: Investing.com