January 12, 2024

- Oil rises after US/UK bomb targets in Yemen.

- US close Monday for MLK Day.

- US dollar firms as risk sentiment sours.

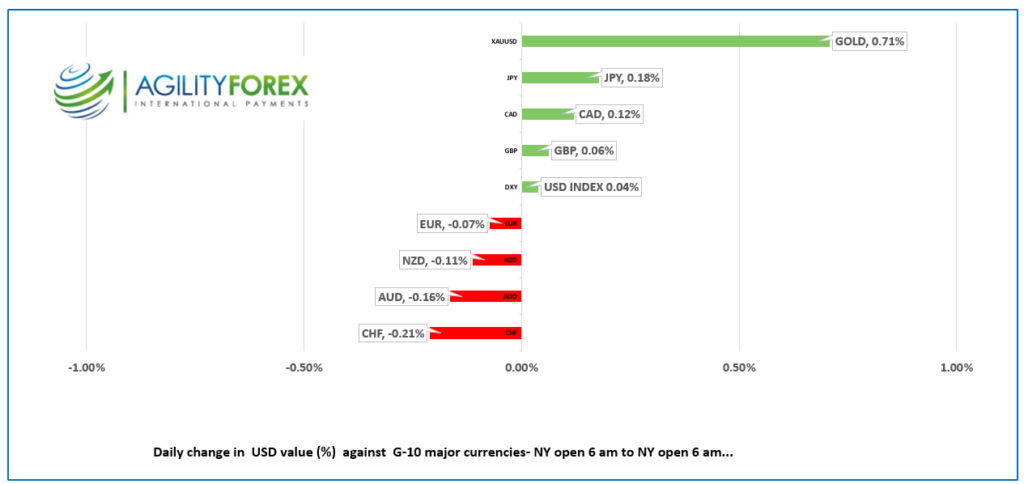

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3356-60, overnight range 1.3348-1.3402, close 1.3395.

Once again, USDCAD is collateral damage when the big boys come out to play. USDCAD rallied and sank in tandem with broad-US dollar moves following the American inflation data. That won’t change today.

USDCAD gains were limited after oil prices rose sharply in response to the US and UK airstrikes on Yemen territory. WTI rose from $71.45/b yesterday to $75.25/b overnight for a gain of 5.3%. Prices have slipped back to $74.67 in NY. Traders are concerned that the joint airstrikes may lead to a widening of the conflict in the Middle East. Russia has complained to the UN that the Yemen strikes are a violation of the UN Charter, and they did it with a straight face.

The Canadian data calendar is empty.

USDCAD Technicals:

The intraday USDCAD technicals are unchanged from Thursday. USDCAD is in an uptrend above 1.3340. but unless 1.3450 breaks, the currency will be rangebound in a 1.3200-1.3450 band. Yesterday’s failure to break above the top suggests a retest of 1.3340 support which if broken could extend losses to 1.3270.

For today, USDCAD support is at 1.3340 and 1.3310. Resistance is at 1.3440 and 1.3480. Todays range 1.3320-1.3420.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Traders suffered whiplash Thursday after the US inflation report provided plenty of fodder for bulls and bears. The immediate reaction was to buy dollars, sell stocks, and drive the yield on the US 10-year Treasury to 4.06% from 3.98%. Then traders decided the data was no big deal and all the moves were reversed just as quickly. That was because they figured the report wouldn’t alter the expected “no change” outcome for the January 31 FOMC meeting as there are two more CPI reports before the Fed meets in March.

Cleveland Fed President Loretta Mester said that the December CPI report showed that there was more work to do to get inflation to the 2.0% target. Then she said, “I think March is probably too early in my estimation for a rate decline because I think we need to see some more evidence.”

US Producer Price Index rose just 1.0% (forecast 1.3% y/y vs 0.9% in November) which suggests yesterday’s higher CPI reading may have been an anomaly.

Risk sentiment took a turn for the worse after the US and UK announced they had bombed targets in Yemen in retaliation for the Houthis attacking Red Sea shipping. The news boosted oil and gold prices.

Asian equities closed mixed. Japan’s Nikkei 225 index rose 1.5% or over 6.0% month-to-date. Australia’s ASX 200 index closed down 0.10%. European bourses opened positively and added to the gains. The French CAC leads the parade higher with a 0.97% gain followed by a 0.78% rise in the German Dax. SP500 futures are less perky and are down 0.14%.

EURUSD traded in a 1.0951-1.0985 range overnight. Prices may gravitate toward the 1.0920-50 area until the 10 am NY option expiry window closes, thanks to $2.7B in strikes rolling off. ECB President Christine Lagarde was optimistic that the worst part of the inflation fight was over and said, “I think that rates, barring any further shocks or unexpected data, will not continue to go up.”

GBPUSD continues to be whipped about like the proverbial red-headed stepchild. Prices have swung between 1.2690-1.2785 since yesterday in a data-fueled frenzy. Prices rallied from the overnight session low of 1.2724 to 1.2785 after news that the UK economy grew more than expected in November, rising 0.3% (forecast 0.2%). However, the fact that the UK economy shrank in the September-November period (-0.2%) took the bloom off the rose.

USDJPY traders’ heads are still spinning after the currency spiked to 146.42 from a low of 145.36, post-CPI, then plunged to close at 145.28. Prices continued to fall to 144.84 in Asia before climbing to 145.24 in NY. The price action is all driven by the outlook for US and Japanese interest rate spreads.

AUDUSD recouped yesterday’s post-CPI losses and traded in a narrow 0.6679-0.6715 range overnight. Gains were limited due to caution ahead of the Taiwan election and China’s reaction to the outcome.

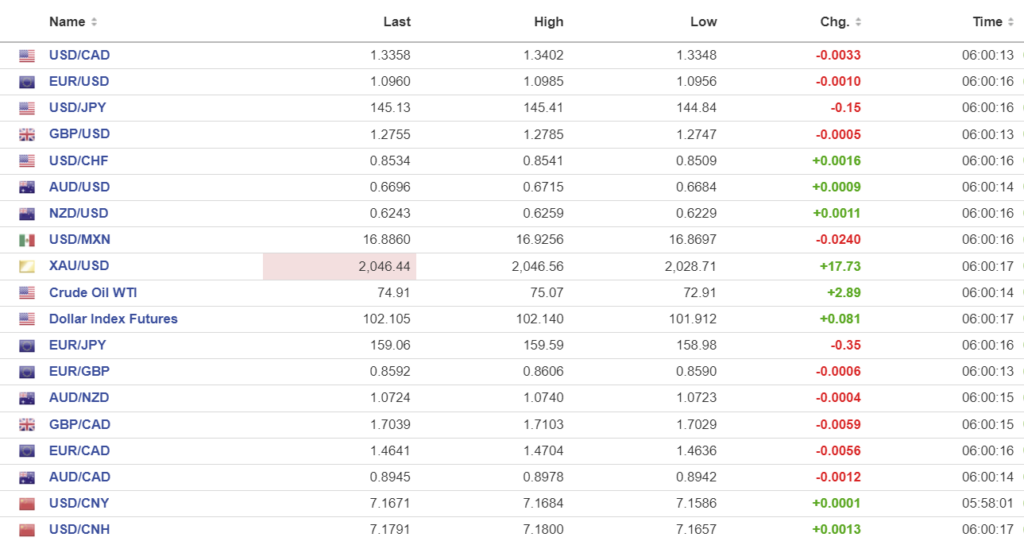

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

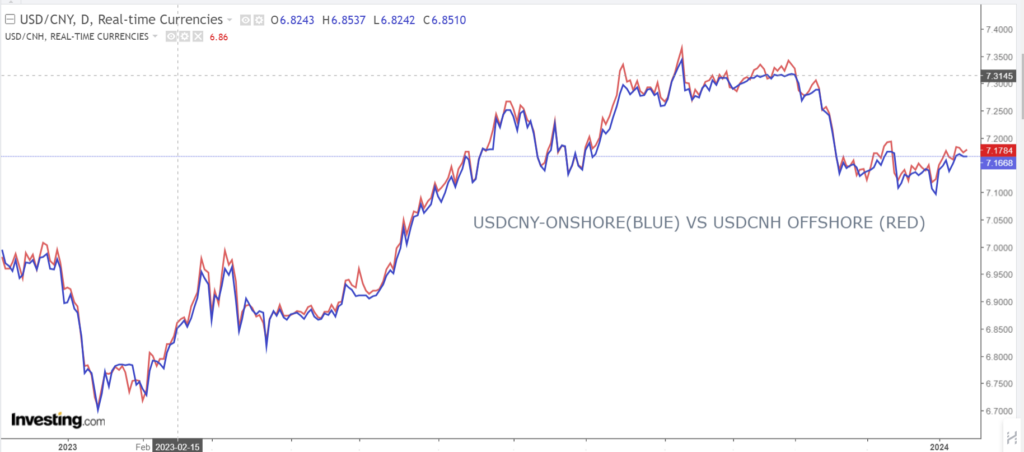

China Snapshot

PBoC fix: today 7.1050, expected 7.1592, previous 7.1087.

Shanghai Shenzhen CSI 300 fell 0.35% to 3284.17.

China December CPI _0.3% y/y, Previous -0.5%. Trade surplus widened to $75.3B from $68.4B in November.

Taiwan election is this weekend which curbed enthusiasm.

Chart: USDCNY and USDCNH 1 year.

Source: Investing.com