September 13, 2023

- US CPI rises 3.7% y/y, core as expected at 4.3%.

- UK GDP falls 0.5% in July, weighs on GBPUSD.

- US dollar steady ahead of inflation report.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3557-61, overnight range: 1.3548-1.3587, close 1.3555

USDCAD underperformed its G-10 peers overnight due higher oil prices and ahead of today’s US inflation data.

WTI extended its recent rally after the monthly Opec oil report predicted demand would outstrip supply by 3 million barrels per day. WTI has risen nearly 34% since June, and a break above resistance at $94.00 per barrel targets $105.00.

Higher crude prices are a double-edged sword for the Bank of Canada. Inflation is well above its 2.0% target and in a speech on September 7, Governor Tiff Macklem expressed concern that “Overall, the prices of goods and services across the economy are still growing, so underlying inflation remains stubbornly above our target.” He went on to say that “the biggest contribution to the slowing in inflation since its peak last year has been from energy which accounts for two-thirds of the slowdown.”

It would seem that the sharp rise in WTI prices since June will reverse that move.

USDCAD Technicals

The intraday USDCAD technicals are indecisive in the context of a 1.3540-1.3580 range. A topside break will keep the June uptrend intact and suggest further gains to 1.3680-1.3700. A downside drop negates the June uptrend and targets 1.3440 then 1.3360

For today, USDCAD support is at 1.3540 and 1.3490. Resistance is at 1.3590 and 1.3660. Today’s range 1.3530-1.3610

Chart: USDCAD 4 hour

Source: Investing.com

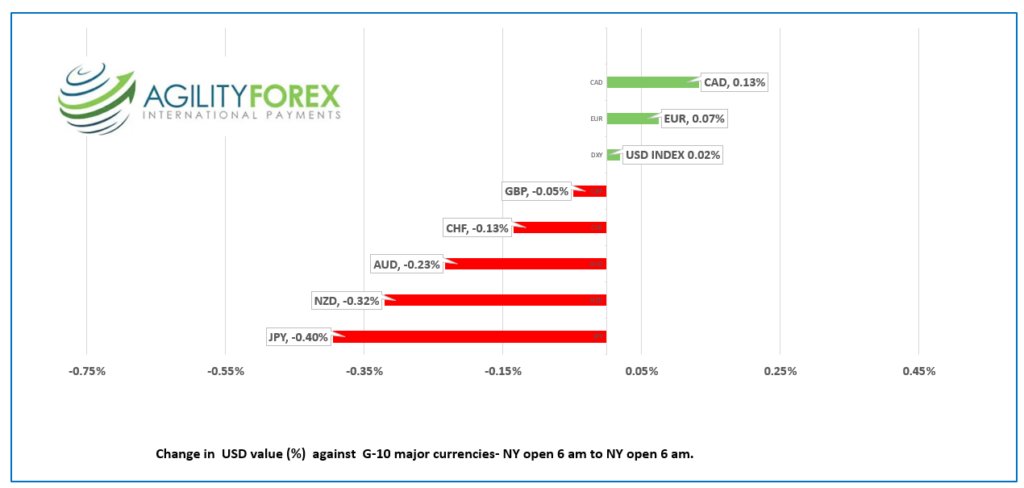

G-10 FX recap

The highly anticipated August inflation report was anti-climatic. You still need a whole lot more spending money more than you did last year but the result was expected. Headline CPI rose 3.7% (forecast 3.6%) while Core CPI was unchanged at 4.3%.

The initial reaction was a higher US dollar, a higher US 10-year Treasury yield, and slightly lower stocks, but those moves were unwound in a blink of an eye.

Oil prices are rising rapidly, and that does not bode well for inflation. Higher oil prices make everything more expensive due to their impact on manufacturing and transportation, and prices may rise further.

EURUSD is trading in a range of 1.0728-1.0765, even after the CPI data. The single currency is getting a modicum of support from a Reuters report saying ECB staff projections (which are released Thursday) estimate 2024 CPI above 3.0%, compared to 2.7% previously. If so, it suggests tomorrow’s ECB meeting will have a hawkish outcome.

GBPUSD traded in a range of 1.2441-1.2502 and is trading with a bearish bias after UK GDP fell 0.5% month-on-month in July, compared to a gain of 0.5% in June. Economists suggest the monthly data is very noisy, but UK growth is slowing. The Bank of England will ignore these results as they are more concerned about wage data, according to ING analysts.

USDJPY rallied in a range of 147.01-147.45 due to the rise in US Treasury yields. August PPI rose 0.3% month-on-month, but the year-over-year numbers dropped to 3.2% from 3.6%. Analysts are predicting that the Bank of Japan will begin tightening by June 2024, and that, coupled with BoJ intervention fears, may limit USDJPY gains.

AUDUSD is at the bottom of its overnight range of 0.6399-0.6424 due to mild risk aversion ahead of today’s US inflation report.

Chart of the Day: WTI oil weekly

Source: Investing.com

Top of Form

Top of Form

FX high, low, open

Source: Investing.com

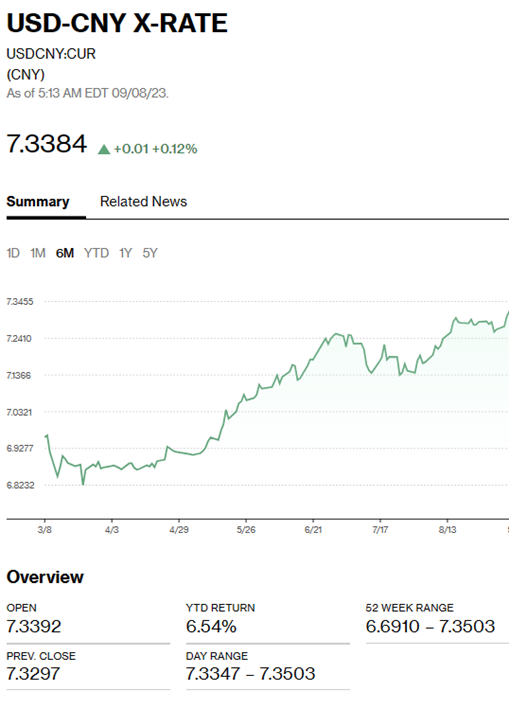

China Snapshot

Bank of China Fix: today 7.1894, expected 7.2783, previous 7.1986

Shanghai Shenzhen CSI 300 fell 0.64% to 3736.65

Chart: USDCNY 1 month

Source: Bloomberg