Source: IFXA/Raymond Peters

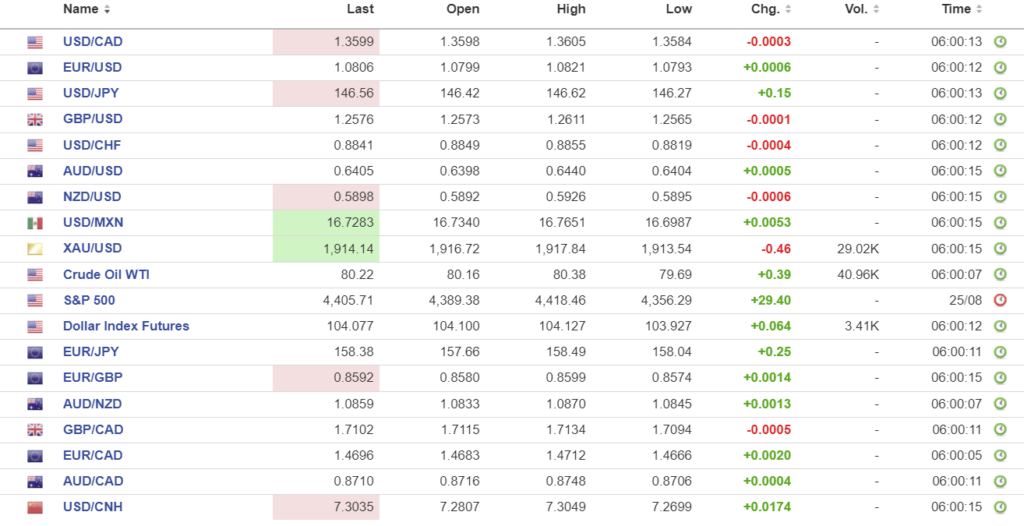

USDCAD Snapshot: open: 1.3597-01, overnight range: 1.3584-1.3607, close 1.3603

USDCAD continues to grind higher due to broad-based US dollar demand against the majors and the prospect for higher US interest rates. USDCAD may also be supported by concerns that Canada GDP will fall sharply in June (forecast -0.2% vs 0.3% in May) as a sharply slowing economy suggests the Bank of Canada will refrain from tightening monetary policy.

Oil prices have retreated from last week’s peak, with WTI trading in a $79.69/b-$8038/b range overnight. Fears that the Chinese economy is far weaker than expected and rising oil production in the US and other regions is limiting gains. Traders are also keeping an eye on Venezuela as the US is reportedly considering easing sanctions on its crude.

The Canadian data calendar is empty.

USDCAD Technicals

The intraday USDCAD technicals are bullish with the uptrend channel from August 1 guiding prices higher, inside a 1.3550-1.3730 channel. A decisive break above 1.3605 targets 1.3670 while a move below 1.3550 suggests further losses to 1.3460.

For today, USDCAD support is at 1.3580 and 1.3540. Resistance is at 1.3640 and 1.3670. Today’s range 1.3570-1.3640.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Traders began their weekend trying to decide if Fed Chair Powell’s Jackson Hole speech was more hawkish than expected, or merely a rehash of previous comments. They are still undecided at the start of this week. UK traders may be more perplexed, as they have taken today off to further evaluate the speech while sitting on a beach. Futures traders are pricing in an 80% chance that the Fed leaves rates unchanged on September 20, but the odds for a rate hike on November 1 are about 60%.

The debate will continue to rage all week, especially around key US data releases such as Q2 GDP, PCE prices, and the nonfarm payrolls on Friday.

Asian equity indexes rallied across the board, led by a 2.73% gain in Japan’s Nikkei 225 index, while Australia’s ASX 200 rose 0.63%. European bourses have gained modestly, and S&P 500 futures are slightly higher.

EURUSD traded in a 1.0793-1.0822 range, deriving a bit of support from higher equity prices, but gains were limited by uncertainty around ECB interest rates. European Central Bank President Christine Lagarde avoided talking about an ECB rate hike or pause in her Jackson Hole speech.

GBPUSD traded quietly in a 1.2565-1.2611 range, with price movements tracking EURUSD moves. The UK was closed for a Bank holiday.

USDJPY traded in a narrow range and is sitting in the middle of its 146.27-146.62 overnight range. Prices continue to be supported by the prospect of higher US interest rates, although the US 10-year Treasury yield remained steady at 4.23%.

AUDUSD continued to consolidate last week’s losses in a 0.6401-0.6440 range. Support from the news of China’s latest stimulus plan has already faded, and AUDUSD is at its session low.

There are no US economic reports of note today.

Top of Form

FX high, low, open

Source: Investing.com

China Snapshot

Bank of China Fix: today 7.1856 previous 7.1883.

Shanghai Shenzhen CSI 300 fell rise 1.17% to 3752.62.

Chinese stocks rose after authorities cut the stamp duty on stock trades from 0.1% to 0.05%, the first cut since 2008. The cut was not a total surprise as such a move has been rumoured for weeks. The rally may not be long lasting. Bloomberg reported that authorities asked some mutual funds to avoid selling equities on a net basis, which is a blatant attempt to manipulate indexes higher.

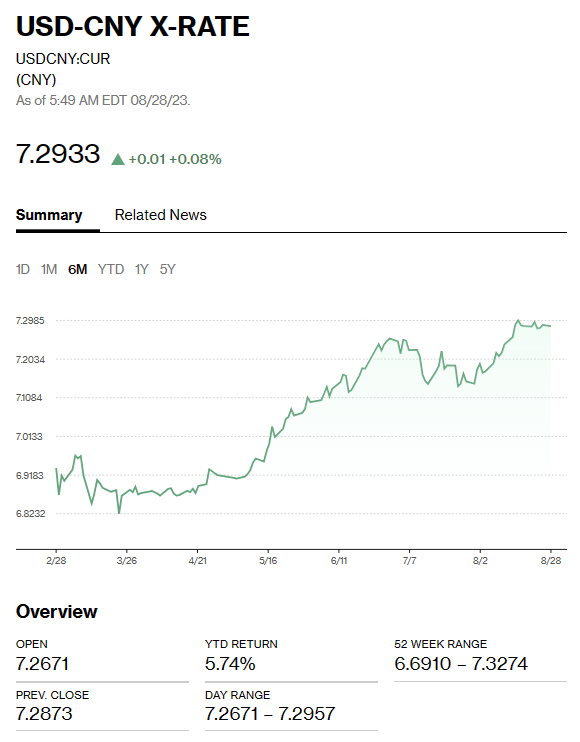

Chart: USDCNY 1 month

Source: Bloomberg