August 19, 2024

- Fed Daly on board for gradual rate cuts.

- Traders looking ahead to Eurozone and Canada inflation data Tuesday.

- US dollar trading with a bearish bias.

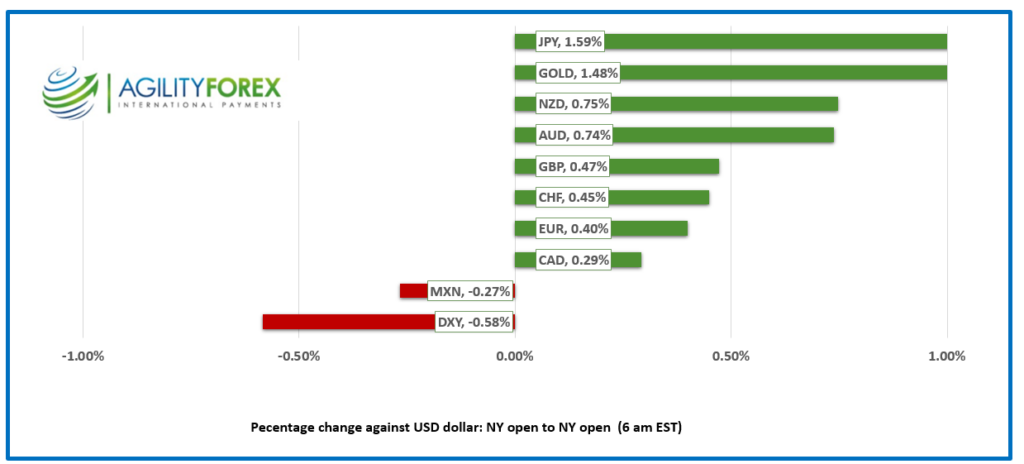

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3681, overnight range 1.3662-1.3685, previous close 1.3679

USDCAD sank under the weight of widespread US selling pressures against the majors. Traders are looking ahead to tomorrow’s release of July inflation data, with expectations of a 2.5% y/y increase compared to 2.7% in June. If the data comes in soft and encourages speculation of another BoC rate cut, USDCAD may find some support, although this will largely depend on the broader US dollar outlook.

The domestic economy faces potential headwinds from a possible rail strike starting Thursday. Canadian Pacific Kansas City Ltd has received a 72-hour strike notice from the Teamsters Union, which could lead to a strike beginning Thursday. CN Rail has also announced plans to lock out workers on the same day. A prolonged strike would disrupt supply chains and could push prices higher.

Oil prices fell from $75.59 to $74.58 after Iran failed to follow through on threats to attack Israel. The presence of the USS Abraham Lincoln battle group within missile range of downtown Tehran may have influenced Iran’s decision.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3740 and looking for a break below 1.3650 to extend losses to 1.3610 and then test 1.3580.

The USDCAD daily chart suggests the longer term trend is still bullish while prices are above 1.3630 which is where the 2024 uptrend line from January comes into play. On the other hand, the 200 day moving average at 1.3590 is an attractive target after the 100-day moving average at 1.3700 gave way.

For today, USDCAD support is at 1.3660 and 1.3640. Resistance is at 1.3710 and 1.3750. Today’s Range 1.3660-1.3730

Chart: USDCAD daily

Source: DailyFX

Quiet Start to Busy Week

Traders returned to their desks Monday morning to find a whole lot of nothing going on—at least in terms of top-tier economic data. That changes tomorrow with the PBoC interest rate decision, the RBA minutes from the August 6 meeting, and inflation data from the Eurozone and Canada. Attention to data may be diverted by this year’s Jackson Hole Symposium, which begins Thursday, against the backdrop of the Democratic National Convention (DNC) in Chicago. The media is rife with comparisons to the 1968 DNC, which was marred by mass demonstrations and violence.

Doves Are Flapping Their Gums

San Francisco Fed President Mary Daly is advocating for a gradual approach to lowering U.S. interest rates, arguing there’s little evidence the economy is heading for a downturn. She stated, “Gradualism is not weak, it’s not slow, it’s not behind, it’s just prudent.” Her colleague, Chicago Fed President Austan Goolsbee, agrees, saying, “You don’t want to tighten any longer than you have to. The reason you’d want to tighten is if you’re afraid the economy is overheating, and this is not what an overheating economy looks like to me.”

Equity Markets Undecided

Global equity markets are mixed due to a lack of data and rising event risk as the week progresses. Japan’s Topix Index fell by 1.40%, while Australia’s ASX rose 0.12%. European bourses are flitting either side of unchanged, while S&P 500 futures remain steady. The U.S. 10-year Treasury yield is at 3.871%, while gold (XAUUSD) has retreated from Friday’s peak of $2,509.73 to $2,497.53 in New York today.

EURUSD

EURUSD bounced within a 1.1023-1.1050 range and is trading where it closed on Friday. Dovish comments from Fed officials and Iran’s failure to follow through on threats to attack Israel have improved global risk sentiment. However, further gains in EURUSD may be limited if Eurozone data reignites inflation concerns.

GBPUSD

GBPUSD climbed from 1.2938 to 1.29765 before settling at 1.2961 in New York. Sterling is underpinned by broad U.S. dollar weakness and a rise in the Rightmove House Price Index to 0.8% y/y in August, compared to 0.4% in July.

USDJPY

USDJPY experienced volatility, with prices rising to 148.05 at the Asia open before plunging to 145.19 just before Europe opened. Prices have since rallied to 146.41 in New York. The outlook for higher Japanese and lower U.S. interest rates, combined with intervention fears and carry trade unwinding, is roiling markets.

AUDUSD and NZDUSD

AUDUSD rose from 0.6660 to 0.6694, supported by improved risk sentiment. The pair has a lingering bid following last week’s comments by RBA Governor Michelle Bullock, who warned that upside risks to inflation could lead to higher rates. NZDUSD followed AUDUSD, climbing from 0.6043 to 0.6087, with prices getting an added lift from better-than-expected (but still weak) New Zealand Performance of Services Index (PSI) data.

USDMXN

USDMXN is slightly firmer, rising from 18.6052 to 18.6780. The currency is supported by sluggish Mexican economic growth (Q2 0.8% y/y vs Q1 1.1% y/y) and ongoing political concerns.

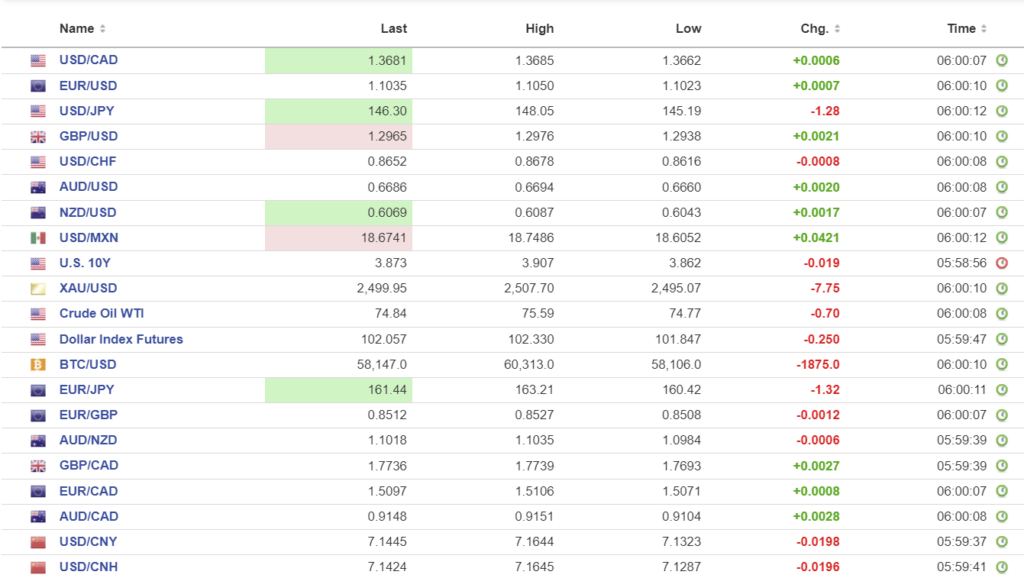

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1415 vs exp. 7.1548 (prev. 7.1464).

Shanghai Shenzhen CSI 300 rose 0.34% to 3356.97

PBoC monetary policy meeting tomorrow.

Chart: USDCNY and USDCNH

Source: Investing.com