Source: HDClipartall.com

- RBA surprises with smaller than expected rate hike (25 bp vs forecast for 50 bp)

- US 10-year yield extends slide to 3.583% (4.01% on Sept. 28)

- US dollar sharply lower compared to Monday open, but above its worst levels.

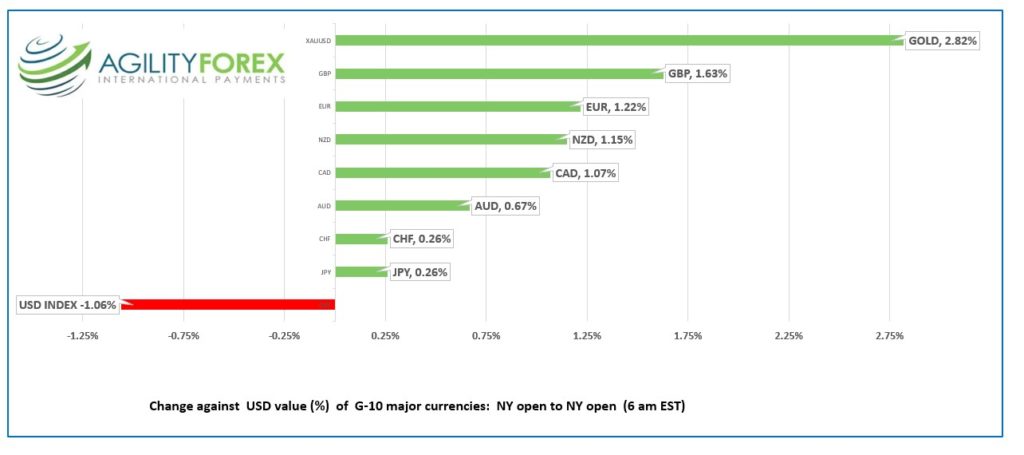

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3634-38, overnight range 1.3570-1.3651, close 1.3623

USDCAD retreated aggressively yesterday as the plunging 10-year Treasury yield sent the S&P 500 index soaring. Stop-losses were triggered on the break below 1.3740 and selling continued overnight until prices found a floor at 1.3570.

USDCAD selling pressures were exacerbated by a 6.0% spike in WTI oil prices. WTI is getting support from talk that Opec will announce a production cut of 1 million barrels/day at Wednesday’s meeting. However, the cut is just symbolic as the cartel has not been able to meet its existing quotas. The oil price rally is more a factor of broad US dollar weakness.

USDCAD may have already seen its bottom for this correction as recent Fed-speak suggests the FOMC will not deviate from its higher interest rate policy.

USDCAD Technical outlook

The intraday technicals turned bearish with the move below 1.3740 and the downtrend on the hourly chart is intact while prices are below 1.3680. A decisive move below 1.3550 would suggest further losses to 1.3320. A move above 1.3740 would argue for further 1.3550-1.3850 consolidation.

For today, USDCAD support is at 1.3550 and 1.3470. Resistance is at 1.3680 and 1.3740. Today’s range: 1.3620-1.3720

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

What goes up does go down. US dollar and bond trader bulls learned that lesson yesterday. The US dollar index (USDX) slid from 112.52 to 110.91 overnight, while the US 10-year Treasury yield dropped from 4.01% last Thursday to 3.575% today.

The sell-off was exacerbated by slightly disappointing ISM Manufacturing data (actual 50.9 vs forecast 52.2). The employment and new orders components dropped into contraction territory and suddenly the narrative switched to “the Fed needs to slow or pivot to avoid a recession.”

The recession angle got more traction than it deserved with a Wall Street Journal headline shouting “U.N. Calls On Fed, Other Central Banks to Halt Interest-Rate Increases.”

Actually, the United Nations Conference on Trade and Development press released didn’t mention the Fed by name. It said, “Central banks in developed economies to revert course and avoid the temptation to try to bring down prices by relying on ever higher interest rates.”

No matter. Traders were extremely long dollars, and bonds and the data, and the headlines sparked a long overdue, profit-taking sell-off.

Fed officials haven’t changed their tune. New York Fed President John Williams claimed that they have not even raised rates to levels that restrict economic growth and said, “My view is we still have a significant ways to go.”

Richmond Fed President Thomas Barkin admitted the Fed worried about “collateral damage to other economies, But in the end, our mandate is to help operate the US economy. So you worry about it most in terms of does it affect the US economy.” He sounds like a guy who ignored the UN report.

Wall Street closed with robust gains and Asian markets followed suit. Japan’s Nikkei 225 index rose 2.96% while Australia’s ASX 200 index rallied 3.76%, getting an added lift from the RBA.

European bourses are soaring with the German Dax gaining 3.07%. US equity futures are extending yesterday’s gains. S&P 500 futures have risen 1.75%.

Gold (XAUUSD) rose from $1660.00 yesterday to $1712.51 today.

EURUSD is trading at the top of its overnight 0.9807-0.9903 range powered by broad US dollar weakness and exacerbated by the triggering of stop losses. EURUSD gains may be limited due to the Eurozone recession which is exacerbated by the war in Ukraine and the energy crisis. Reports that Russia may conduct a “nuclear test” near the Ukraine border aren’t helping matters.

GBPUSD traded in a 1.1282-1.1428 range. Prices peaked in early London trading and slid to 1.1350 in NY. UK Chancellor Kwasi Kwarteng may think the GBPUSD rally, since his tax cut policy reversal, is evidence he is a fiscal genius, but others suggest the rally may be because investors believe both he, and the Prime Minister will soon be toast. The reality is the gains are a classic “short-squeeze” and not likely to last.

USDJPY is a drift in a 144.42-144.90 band. Traders seemed unconcerned when a North Korean missile flew over Japan and landed in the Pacific Ocean. They also ignored Japanese inflation data.

AUDUSD rallied from 0.6452 to 0.6546 when the RBA monetary policy statement was released. The RBA hiked rates 0.25%, surprising many, which lifted stocks and the currency. The US dollar sell-off began fading in Europe and AUDUSD retreated.

Todays US data includes JOLTS job openings and Factory orders.

Chart of the Day: US dollar Index

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: Closed: previous 7.0998

Shanghai Shenzhen CSI 300 closed

NOTE: Chinese markets closed next week for Golden Week.

Chart: USDCNH (offshore) 1 month

Source: Saxo Bank