Source: Pixabay

- BoE hikes rates 0.25%, ECB stays the course

- Meta (Facebook) earnings sink equities overnight

- US dollar firms on safe haven demand

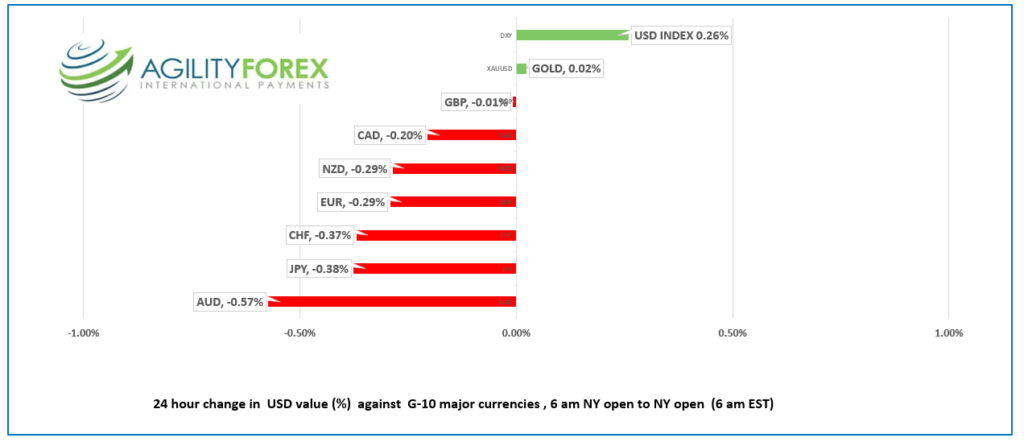

FX at a Glance

Source: IFXA Ltd/RP

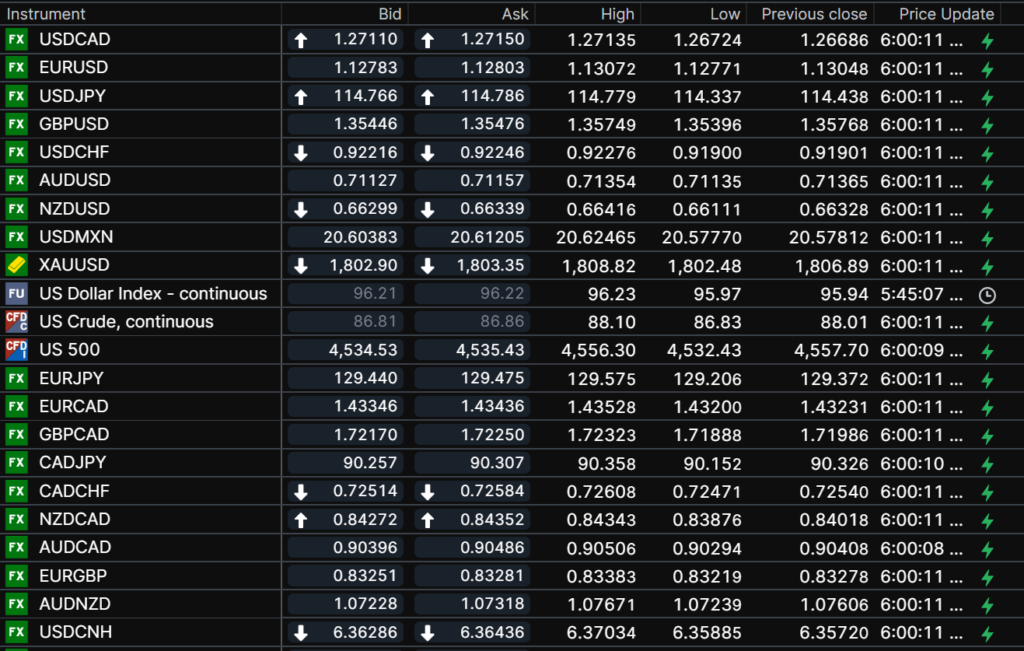

USDCAD Snapshot: Open 1.2711-15, Overnight Range-1.2672-1.2714, previous close 1.2669

USDCAD is the ping-pong ball and risk sentiment is the paddle. USDCAD climbed steadily overnight due to a bout of risk aversion, this time stemming from falling stock market prices. As usual domestic influences are ignored.

BoC Governor Tiff Macklem repeated the comments he made at the Monetary Policy Press conference when he addressed the Standing Senate Committee on Banking, Trade and Commerce yesterday. He said the country no longer needed pandemic emergency measures. He predicted a rising path for Canadian rates, and that the BoC was committed to controlling inflation.

Those comments are at least as aggressive as remarks from various Fed policymakers but ignored. Nevertheless, firm oil prices and an aggressive BoC should counteract US dollar demand from the Fed rate hike outlook.

WTI oil prices touched $89.70/b yesterday, underpinned by Opec refusing to increase its previously announced 400,000 b/day production increase in March. In addition, EIA weekly inventories fell by 1.04 million barrels. The gains did not last and WTI dropped to $86.84 in early NY trading.

Today, USDCAD direction will be determined by the reactions to the ECB meeting and Wall Street performance.

Technical view: The intraday USDCAD technicals are bullish above 1.2660, looking for a break above 1.2690 to extend gains to 1.2860. A decisive move below 1.2620 (100 day moving average targets 1.2508, 200 day moving average.

For today, USDCAD support is at 1.2660 and 1.2620. Resistance is at 1.2750 and 1.2810. Today’s Range 1.2660-1.2760

Chart USDCAD daily-one year

Source: Saxo Bank

G-10 FX recap and outlook

Winter-weary Canadian’s got contradictory results from weather-forecasting rodents. In Ontario Wiarton, Willie didn’t see his shadow, which means six more weeks of winter. It’s an early spring for New York as Punxsutawney Phil saw his shadow.

Interestingly, 3 in 5 Americans believe the rodent forecast, which, coincidently, is the same number of anti-vaxxers who believe the Covid vaccines are a government program to control their mind.

Equity trades in Asia and Europe couldn’t care less about the meteorologic abilities of rodents but were seriously disappointed by Meta (FB: Nasdaq) results. FB dropped 20.5% in overnight markets, which soured sentiment in Asia and Europe. The Nikkei 225 closed down 1.06%, and European bourses are in negative territory. S&P 500 and DIA futures are down 1.21% and 0.43%, respectively (6:45 am). Oil and gold are trading lower in part because the US 10-year Treasury yield climbed to 1.77% from 1.75% in early Asia.

US weekly jobless claims were 238,000, a drop of 23,000 in the week ending January 28 and US Non-farm Productivity growth rose 6.6% in Q4

EURUSD retraced earlier gains ahead of the ECB monetary policy meeting then recouped those losses after the ECB statement. The ECB said it confirmed the decisions made in December and is sticking to its plan to leave the deposit rate at negative 0.5%. However, EURUSD bulls saw a glimmer of home from a tweak in the message. The dumped “in either direction from the sentence “the council stood ready to adjust all its instruments.”

GBPUSD surged from 1.3540 in Asia to 1.3624 in early New York after the Bank of England did what was expected and hiked rates 0.25%. The move was blamed on inflation which they expect to rise to 7.0% before retreating to 2.0%. Governor Bailey’s remarks are just beginning.

USDJPY climbed on the back of higher US Treasury yields, rising from 114.34 to 114.84. BoJ Deputy Governor Masazumi Wakatabe’s comment that it was “too early” to tighten rates was ignored.

AUDUSD and NZDUSD retreated due to the poor risk sentiment. Australia Services PMI was a tad better than expected.

Chart of the Day: US Dollar Index (USDX)

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

China Snapshot

Today’s Bank of China Fix 6.3746, previous 6.3746-Close

Shanghai Shenzhen CSI 300 closed

Chinese New Year-January 31 to February 15.

Chart: USDCNH (offshore yuan) hourly

Source: Saxo Bank