August 29, 2024

- Q2 GDP (prelim) rise 3% (forecast and previous 2.8% y/y

- US weekly jobless claims may dip 1,000 to 231,000.

- US dollar sell-off stalls.

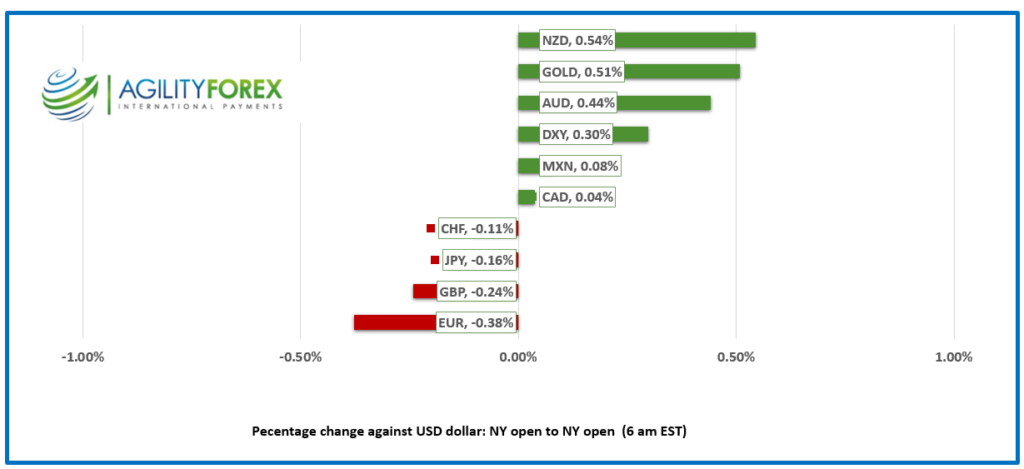

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3456, overnight range 1.3450-1.3483, previous close 1.3480

USDCAD is directionless and rangebound today, and this mornings US economic data dump did not change anything. Expectations for a 50 bps Fed rate cut next month have narrowed the 10-year CAD/US interest rate differential to -73.9 bps (in favor of the US), which is just above the narrowest level seen in the past six months (March 31=-69.6). The drop in spreads, combined with stretched short CAD/long US dollar speculative positioning, is limiting USDCAD gains.

WTI oil prices edged lower, trading in a 74.00-74.83 range, partly due to disappointment from the Energy Information Administration (EIA) report showing a smaller-than-expected crude drawdown (actual -0.844 m/b, forecast -3 m/b). Additionally, UBS’s downgrade of China’s GDP for 2024 reminded traders of the risk of slowing demand from China.

The lack of top-tier Canadian data today suggests another uninspiring trading session, with a bearish USDCAD bias. Canada’s Current Account deficit widened to 8.48 billion from 5.37 billion.

USDCAD technicals

The intraday USDCAD technicals are bearish while trading below 1.3490 and are looking to break support in the 1.3440 zone to extend losses toward 1.3360. A move above 1.3490 suggest a retest of the 1.3580 area.

Longer term, if USDCAD breaks support at 1.3380 it suggests a straight shot to 1.3180, the August 2021 low.

For today, USDCAD support is at 1.3430 and 1.3410. Resistance is at 1.3490 and 1.3520. Today’s Range 1.3430-1.3510.

Chart: USDCAD 4 hour

Source: DailyFX

There Is No Pleasing Some People

Nvidia (NVDA: Nasdaq) shares are down 3% in pre-market trading despite a $30 billion increase in quarterly revenue, translating into a 122% year-over-year jump. This marks the fourth consecutive quarter of triple-digit growth. Yet, these impressive results weren’t enough for traders, and the stock took a hit.

Lots of US Data-Few Traders who Care

This morning’s US data dump was mostly positive but financial markets barely reacted. That may be because it will have little bearing on the September 18 FOMC decision or it may be because many traders have booked off this, the last week of summer. Weekly jobless fell 1,000 to 231,000 while the previous week was revised up by 1,000. Q2 GDP was a tad stronger than expected at 3.0% (forecast 2.8% y/y) but it had little impact as it is stale.

EURUSD

EURUSD is trading negatively in a 1.1072-1.1140 range, currently sitting at 1.1094 in early NY trading. The single currency came under pressure despite improved Economic Sentiment, Consumer Confidence, and Services Sentiment in August. ING economists point out that the devil is in the details—those details suggest that all the improvements were due to a French Olympics boost. Otherwise, the results highlight weak Eurozone manufacturing with high inventories. Additionally, German regional inflation data came in weaker than expected.

GBPUSD

GBPUSD is trading defensively in a 1.3155-1.3227 range after peaking at 1.3264 on Wednesday. Concerns that the new UK government will raise capital gains taxes, combined with the government’s bleak assessment of the economy, are weighing on sterling. GBPUSD is in a minor downtrend on the hourly chart while prices remain below 1.3230.

USDJPY

USDJPY traded quietly in a 144.22-144.87 range then spiked to 145.35 after the US data which lifted the US 10-year Treasury yield from 3.824% to 3.865%. Typhoon Shanshan made landfall and could reach Tokyo by the weekend.

AUDUSD and NZDUSD

AUDUSD recovered yesterday’s losses, rallying from 0.6781 to 0.6825, supported by better-than-expected CPI data yesterday. Traders ignored disappointing Q2 Private Capital Expenditure data (actual -2.2%, forecast 1.0%, previous 1.9%).

NZDUSD rallied from 0.6241 to 0.6299 following a surge in the ANZ Business Confidence Index from 27.1 to 50.6, along with a jump in the Activity Outlook Index to 37.1% from 16.3%.

USDMXN

USDMXN gave back some of yesterday’s gains, dropping to 19.5683 from 19.7100. The relentless peso selling saw a bit of a reprieve after comments by a policymaker on Tuesday, stating that authorities would not rush an overhaul of the judiciary system. USDMXN is underpinned by carry-trade unwinding and bullish technicals, suggesting the uptrend remains intact above 18.9000.

Bitcoin (BTCUSD)

BTCUSD continues to hover around the 60,000 level, trading in a 58,085-60,333 band overnight. Volumes are light ahead of the US Labour Day weekend.

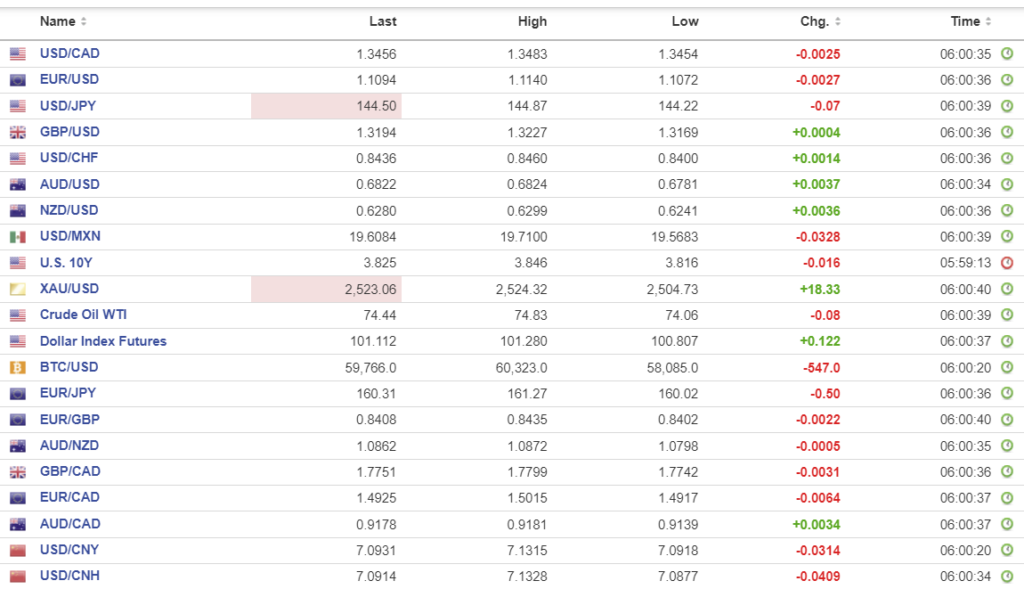

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1299 vs exp. 7.1297 (prev. 7.1216)

Shanghai Shenzhen CSI 300 fell 0.27% to 3277.68

Economists from UBS, Nomura, and JPMorgan Chase do not believe China will meet Xi Jinping’s 5.0% y/y GDP growth target. UBS just cut its forecast to 4.6% from 4.9% earlier and just 4.0% in 2025. A key factor is is ongoing real estate downturn.

Chart: USDCNY and USDCNH

Source: Investing.com