Photo:Bing AI

August 2, 2023

- Fitch downgrades USA to AA Stable

- Risk aversion simmers from Trump indictment, Russia/Ukraine, and Fitch

- USD dollar rallies on safe-haven demand.

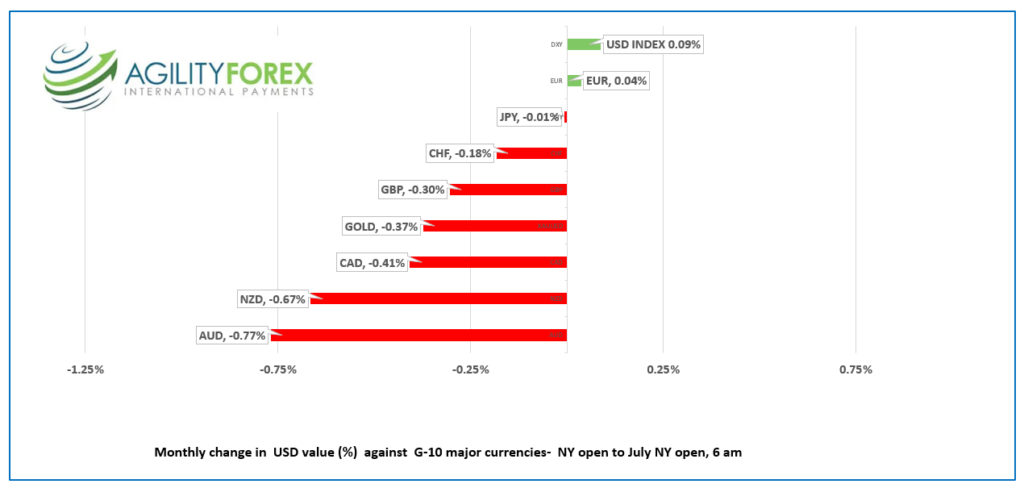

FX at a Glance

Source: IFXA/RP

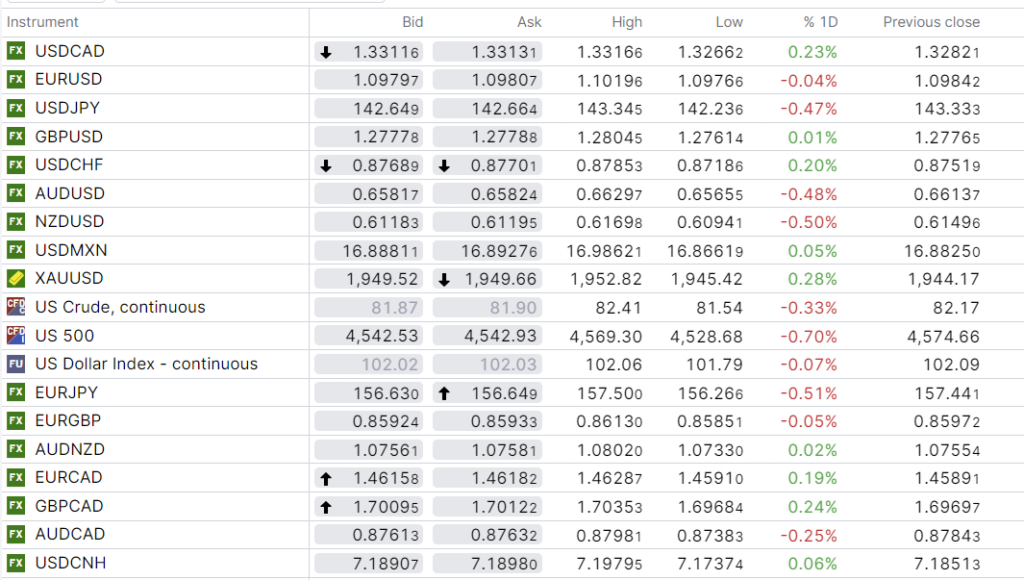

USDCAD Snapshot: open: 1.3310-14, overnight range 1.3266-1.3316, close 1.3282

USDCAD rallied on the heels of the latest bout of risk aversion, which lifted the currency pair above the top of it’s three-week range, but below the downtrend line from June 5. The rally was exacerbated by negative sentiment towards commodity bloc currencies, although higher oil prices let the Canadian dollar outperform against AUD and NZD.

WTI oil retreated from its overnight peak of $82.41 and touched $811.54/b before climbing to $81.94 in NY. Oil prices are supported by expectations of demand outstripping supply in the next few months.

There are no domestic economic reports today or Thursday, leaving USDCAD direction dictated by broad US dollar moves.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3300 and looking to break above 1.3330 to target 1.3470. A move below 1.3300 shifts the focus to 1.3260 but only a break below that level negates the upside pressure.

A break above 1.3330 suggests USDCAD will spend some time in a 1.3330-1.3470 range.

For today, USDCAD support is at 1.3260and 1.3220 Resistance is at 1.3330 and 1.3390. Today’s range 1.3260-1.3330

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

ADP reported that private sector jobs rose 324,000 in July, well above the 189,000 expected. In June, ADP reported a similar upside surprise and traders reacted by upwardly revising forecasts for nonfarm payrolls. Oops. NFP came in close to expectations. That suggests the reaction to today’s ADP result will be muted.

Global risk sentiment was on the back-burner but started to simmer yesterday, then bubbled over in Asia and Europe. The cumulative effect of a series of negative headlines ahead of Friday’s US nonfarm payrolls data, in a thin summer market, led to a rash of defensive trading and boosted the Japanese yen and US dollar.

News of Donald Trump’s indictment for “destabilizing lies” about the 2020 election, drone attacks on a Moscow high-rise building housing Russian government ministries, and the Fitch downgrade of US debt combined to rattle traders.

The Fitch downgrade follows on the heels of a similar move by S&P twelve years ago, suggesting the boys and girls at Fitch are a tad late to the party. The Trump indictment is merely a distraction, as it was widely anticipated. The Ukrainian decision to bring the war to Moscow, and Russian Deputy Security Council chairman Dimitri Medvedev’s comments about using nuclear weapons, is a real issue, but to many traders, it’s a case of “not my problem.”

Yesterday’s US data (JOLTS job openings, ISM Manufacturing PMI) indicated that the economy was slowing and supported views that the Fed rate hikes were over.

EURUSD gave up most of Tuesday’s gains, falling from 1.1020 to 1.0970, mainly due to broad safe-haven demand for US dollars. The Eurozone data calendar was light, and traders were content to await Thursday’s Services PMI and PPI data.

GBPUSD chopped around in a 1.2761-1.2805 range, with prices weighed down by the latest bout of risk aversion. The Bank of England is expected to raise rates by 25 bps tomorrow and suggest further rate hikes are likely.

USDJPY fell to 142.24 from 143.35, then rebounded to 142.74 in NY. The market was roiled by more of the same dovish-speak from Bank of Japan officials, higher US Treasury yields, and safe-haven demand for the yen following the Fitch downgrade of the US.

AUDUSD traded negatively in a 0.6566-0.6630 range due to both risk aversion and soft domestic economic data (Construction PMI -9.2, vs 10.6 in May, Industry Index -14.7 vs -11.9 in May).

NZDUSD traded in a 0.6094-0.6170 range after the July employment report suggested that the RBNZ did not need to rush to raise rates. The rise in the unemployment rate from 3.4% to 3.6% suggests the tight labor market is starting to ease.

Today’s US ADP employment report is expected to show a gain of 189,000 jobs compared to 497,000 last month.

FX high, low, previous close

China Snapshot

Bank of China Fix: 7.1368 , forecast 7.1664, previous 7.1283.

Shanghai Shenzhen CSI 300 fell 0.70% to 3969.90.

Chart: USDCNY 6 month

Source: Bloomberg