Photo: Wikimedia commons

- Spin doctors working overtime to discount US recession chatter

- Canada GDP unchanged in May but better than expected

- US dollar ends July on weak note, except against EUR

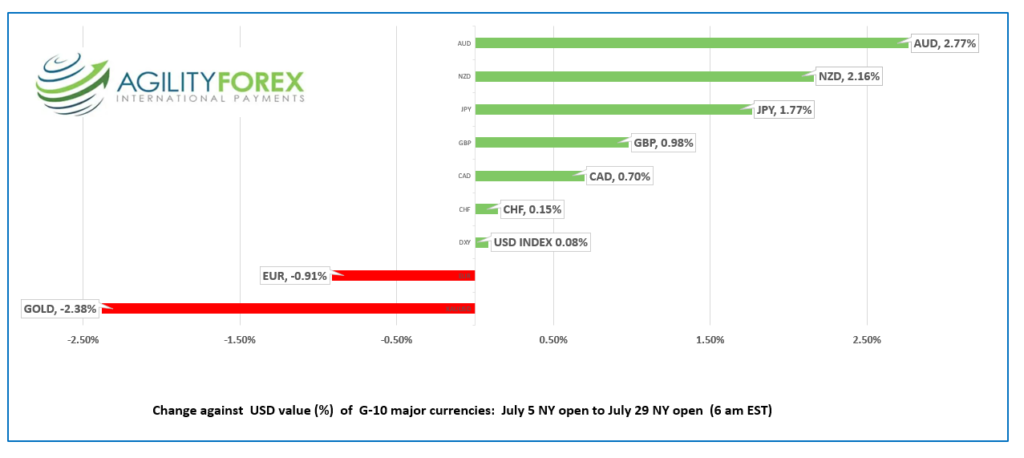

July FX at a glance:

Source: IFXA Ltd/RP

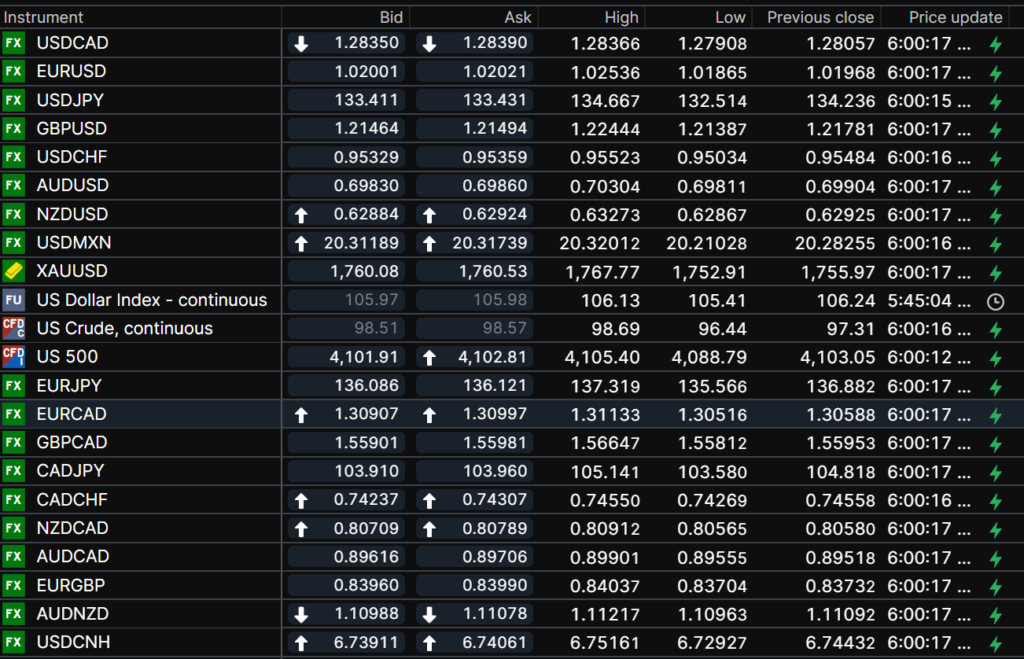

USDCAD Snapshot: open 1.2835-39, overnight range 1.2791-1.2853, close 1.2806

USDCAD does not want to stray too far from the 1.2810 support area, but it may just be a matter of time before the support becomes resistance.

Canada’s economy didn’t grow in May but even better, it didn’t contract. GDP rose 0%m/m compared to the forecast for a 0.2% decline. Statistics Canada is predicting June’s GDP will rise 0.1% m/m because output was up in the construction, manufacturing, and accommodation and food services sectors.

USDCAD may also be undermined by steady to firm oil prices. WTI rose to $98.79/barrel from $96.44/b, partly due to the weaker US dollar.

USDCAD is under pressure due to month-end US dollar selling pressure stemming from the stellar S&P 500 gain in July which is up 6.30% since July 5. Those flows will dominate today with Canada May GDP data just being a distraction.

USDCAD technical outlook

The hourly USDCAD technicals are bearish below 1.2890 looking for a decisive break below the 1.2790-1.2810 zone for an eventual test of 1.2500-20 area. A rebound above 1.2890 suggests further consolidation in a 1.2810-1.3000 range. Meanwhile the uptrend line from the May 2021 low is intact above 1.2500.

For today, USDCAD support is at 1.2790 and 1.2760. Resistance is at 1.2850 and 1.2880. Today’s Range 1.2780-1.2870

Chart: USDCAD hourly

Source: Saxo Bank

G-10 FX recap and outlook

The first reading of U.S. Q2 GDP was a surprisingly weak -0.9% y/y which comes on the heels of a 1.6% drop in Q1. Many believe two consecutive quarters of negative growth mean a “technical recession.” Fed Chair Jerome Powell, his colleagues, and the Biden Administration do not agree.

Mr Powell says the economy is not in a recession. “I do not think the U.S. is currently in a recession, and the reason is there are too many areas of the economy that are performing too well.” Treasury Secretary Janet Yellen said, “a recession is a broad weakening of our economy, and that is not what we are seeing right now.” President Biden added his two cents, saying “It can’t be a recession.

The economy is far stronger than it was after the War of 1812, when I was a boy.”

Bond traders read the data as evidence U.S. rate hikes would become rate cuts sooner than expected to ensure the U.S. doesn’t fall into a recession, technical or otherwise. The 10-year Treasury yield plunged from 2.83% yesterday in Europe to close at 2.681% in N.Y.

The drop in Treasury yields combined with rallying stocks spurred U.S. dollar selling which was exacerbated by month-end portfolio rebalancing flows.

Asia equity markets closed mixed, partly due to negative sentiment spilling over from Chinese markets over government interference in tech stocks. Japan’s Nikkei 225 closed nearly unchanged while Australia’s ASX 200 gained 0.80%.

Month-end flows and positive risk sentiment propelled European bourses higher, led by a 1.22% gain in the French CAC index.

Wall Street futures are pointing to a bullish open and the positive sentiment is underpinning oil and gold prices.

EURUSD shrugged off losses ahead of the US GDP data and rallied from 1.0117 to 1.0254 at the European open before dipping to 1.0187. The single currency is trading at 1.0230, bolstered by Eurozone inflation rising to 8.9% y/y and lower U.S. treasury yields.

GBPUSD is trading just below the middle of its 1.2139-1.2244 range with the peak coinciding with the top of the EURUSD range. GBPUSD is underpinned by month end portfolio rebalancing demand, and broad U.S. dollar weakness, while concerns about ongoing U.K. domestic issues are sidelined.

USDJPY extended losses from Wednesday, with prices falling from 137.40 to 132.51 at the European open before bouncing to 133.26 in N.Y., all due to falling U.S. treasury yields.

AUDUSD and NZDUSD are poised to end the month as the top performing major G-10 currencies. Firmer commodity prices support both pairs, as do higher domestic interest rates, although concerns around China growth may limit gains.

Today’s U.S. data includes Fed favourite Core Personal Consumption and Expenditures Index (PCI) along with the Michigan Consumer Sentiment Index and Chicago Purchasing Managers Index.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix 6.7437, previous 6.7411

Shanghai Shenzhen CSI 300 fell 1.32% to 4,170.10

Chinese stock markets suffer due to concerns around Alibaba. Billionaire Jack Ma is giving up control of Ant Group which many belief is at the behest of heavy-handed Chinese authorities (Xi Jinping, perhaps) who believe Mr Ma got too powerful.

Chart: USDCNY 1 month

Source: Bloomberg