February 26, 2024

- Top tier data void today suggests more range trading.

- Key US PCE data due Thursday

- US dollar opens on mixed note.

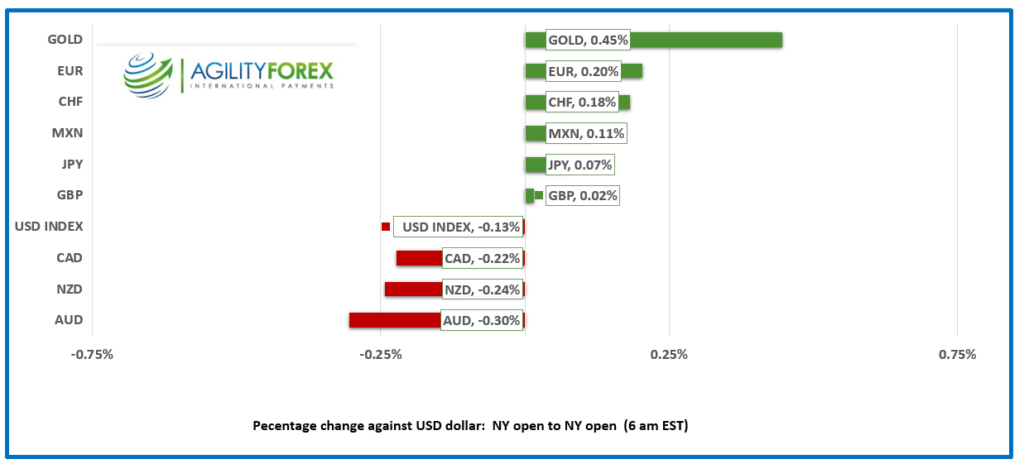

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3516-20, overnight range 1.3496-1.3529, close 1.3515

USDCAD remains rangebound but trading defensively on the back of a widening CAD/US 10 year interest rate spread. Risk sentiment may have also soured a bit after the government plucked $23 billion from the money tree. $20 billion for a pharmacare deal to keep NDP support and a $3 billion pledge to Ukraine. Eventually, someone will have to pay for the largesse.-

USDCAD is not getting any support from oil prices. WTI traded in a $75.84-$76.67 range with prices weighed down by expectations of sluggish demand for all of 2024.

USDCAD direction appears to have shifted from tracking S&P 500 price action to tracking CAD/US yield spreads, and the US is winning.

USDCAD Technicals

The intraday USDCAD technicals are neutral inside a 1.3450-1.3550 range and awaiting for a catalyst to break-out either side of that range. A break above 1.3550 targets 1.3610 then 1.3660 while a move below 1.3450 suggests a test of support at 1.3410, then 1.3360.

For today, USDCAD support is at 1.3470 and 1.3440. Resistance is at 1.3550 and 1.3590. Today’s range is 1.3460-1.3540

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Traders are wearing blinders. They are singularly fixated on the outlook for US interest rates while ignoring a powder-keg of geopolitical risks which, historically, would have injected a note of caution and two-way risk into markets.

Wall Street traders are leading the pack. Nvidia predicted a 233% surge in earnings for Q1 2024 and for a brief moment on Friday, its market cap topped $2.0 trillion, surpassing Alphabet, and making it the 3rd largest company. The news was enough to help lift the DJIA, S&P500 and Nasdaq to record levels.

Meanwhile, momentum has shifted back to Russia in its two-year long war with Ukraine. Ukraine is outgunned, outmanned, and US support is wavering. Iran and North Korea are reportedly shipping missiles and drones to Russia while Ukraine is running out of ammo. Fortunately, Canada’s Justin Trudeau flew to Kyiv and promised CAD $3.0 billion in aid this year. The operative words are promised and this year as he said nothing about “when.”

Israel continues its mission to exterminate Hamas. Palestinians fleeing the war are not getting any help from their Arab cousins. Egypt has built an 8 square mile wall to keep them out.

Houthi rebels continue to disrupt shipping despite being attacked by US and UK forces.

China is continuing its mission to annex the entire South China Sea. Reuters reports that they have built a “barrier” which is inside the Philippines 200 nautical mile exclusive economic zone.

The US Trade Representative’s annual report claims that China is the biggest challenge to the international trading system, suggesting more Trump style tariffs may be in the cards.

And speaking of Trump, he is the defacto Republican nominee for President. Apparently, traders around the world cannot wait for his mild demeanor, and soothing rhetoric to usher in a new era of political decorum and respect, even if the White House moves to San Quentin.

The fan is warmed up and spinning at full power. Beware.

EURUSD rallied from 1.0812 to1.0860 ahead of ECB President Christine Lagarde’s testimony to the EU parliament. She is expected to stick with her hawkish bias. The EURUSD technicals are targeting a break above 1.0810 while support at 1.0810 remains intact.

GBPUSD is modestly bid and has risen to 1.2700 from 1.2658. Traders ignored the latest Goldman Sach forecast that suggests the Bank of England will cut rates five times in 2024.

USDJPY is at the top of its 150.29-150.71 band thanks to the divergent Fed and BoJ interest rate outlooks. The US 10-year Treasury yield remained is 4.25%.

AUDUSD is directionless in a 0.6542-0.6568 band although renewed Us and China trade tensions may limit the top side.

NZDUSD traded in a 0.6182-0.6200 range, ahead of Wednesday’s RBNZ monetary policy meeting. The central bank is expected to leave rates unchanged at 5.50% but there is a small risk of a rate hike.

USDMXN is at the bottom of its 17.0823-17.1348 range due to the soft US dollar against the majors. Scotiabank economists are predicting that the Mexican economy will rebound in the first half of this year.

Todays US data includes New Home Sales for January (forecast 0.68 million).

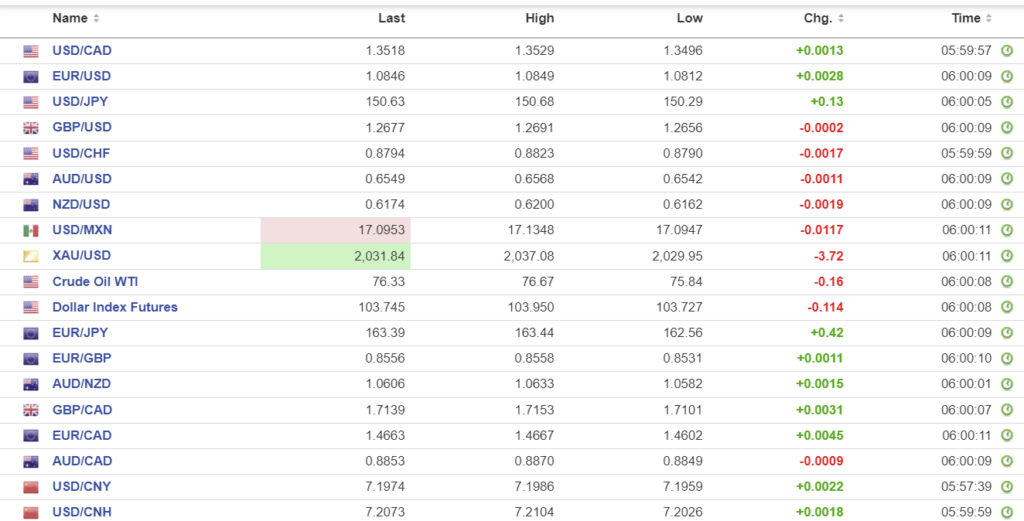

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

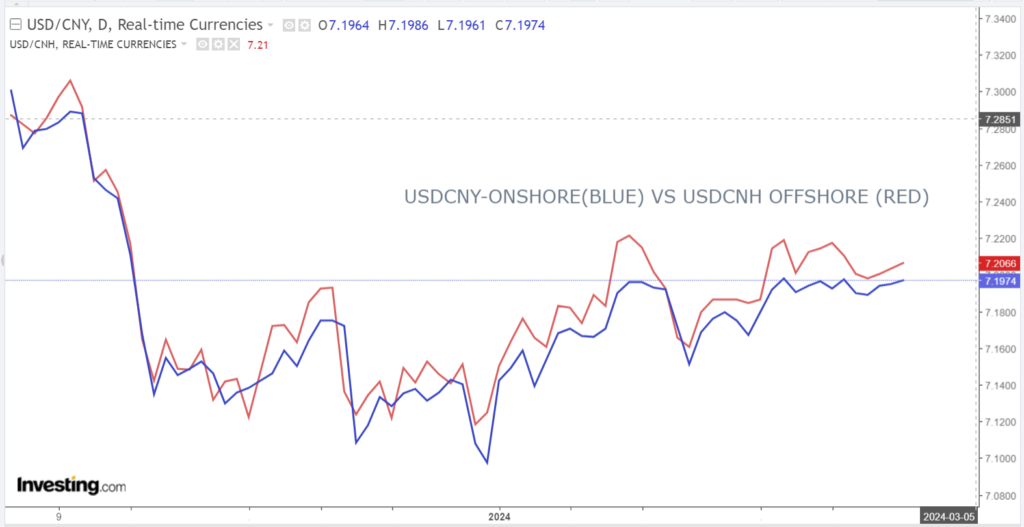

China Snapshot

PBoC fix: closed 7.1080, expected 7.1998, Monday 7.1064

Shanghai Shenzhen CSI 300 fell 1.04% to 3453.36.

Fears on rising US and China trade tensions may have fueled equity losses in mainland indexes. The USTR’s annual report on China’s WTO compliance accuses China of being “the biggest challenge to the international trading system established by the World Trade Organization. It has been 22 years since China acceded to the WTO, and China still embraces a state-directed, non-market approach to the economy and trade, which runs counter to the norms and principles embodied by the WTO. Even more problematic, China’s approach targets industries for global market domination by Chinese companies using an array of constantly evolving non-market policies and practices.”

Chines authorities were apocalyptic. The Ministry of Commerce said “The US does not reflect on and correct its own behaviour, but instead uses smear tactics and blame-shifting methods to cover up its violations and sabotage. This is extremely irresponsible.”

Chart: USDCNY daily and USDCNH

Source: Bloomberg