Source: Pixabay

- China begins Lunar New Year week with soft Manufacturing PMI

- Soft Eurozone Q4 GDP ignored by EURUSD

- CAD poised to end January almost unchanged from Jan.4 opening level

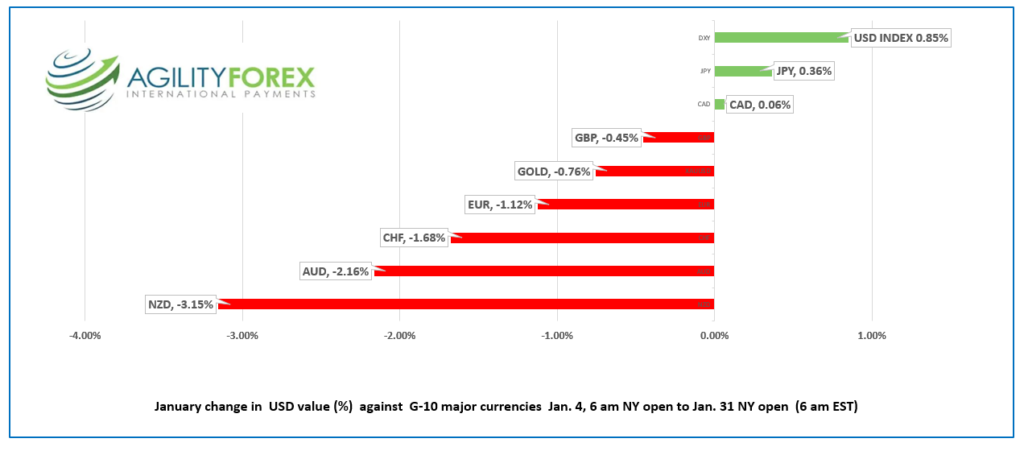

FX at a Glance

Source: IFXA Ltd/RP

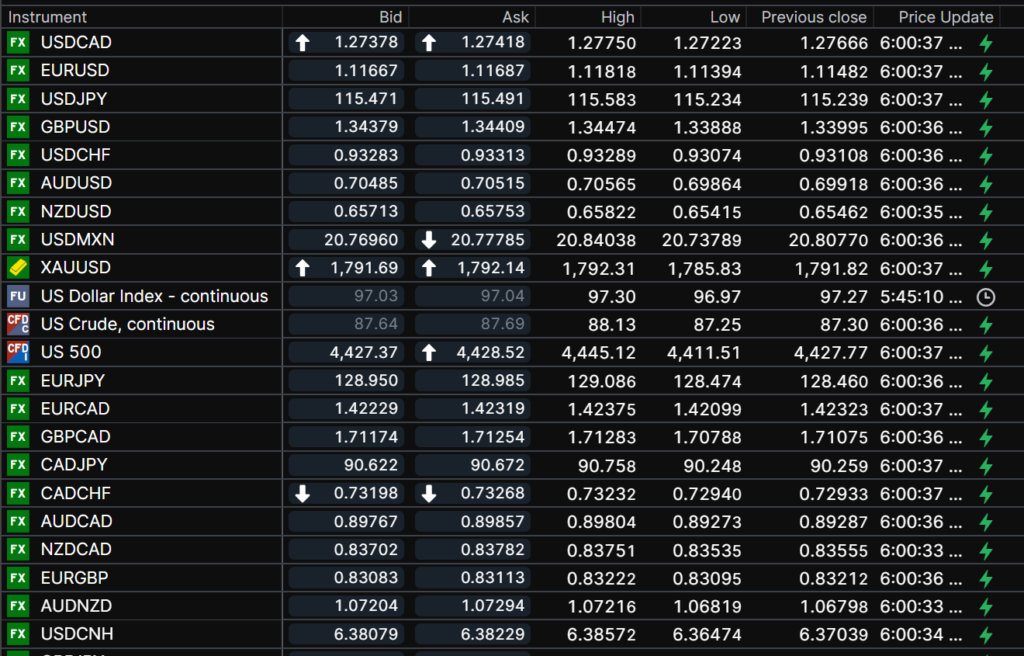

USDCAD Snapshot: Open 1.2738-42, Overnight Range-1.2722-1.2775, previous close 1.2767

USDCAD traded choppily in a 1.2450-1.2805 range in January as prices tracked WTI oil, and the S&P 500, then reacted to the hawkish twist from the Bank of Canada. When the dust settled, USDCAD started today’s NY session, a mere 0.0008 points lower than where it opened on January 4. It is interesting to note, but in the big scheme of things, worthless info.

USDCAD gains were capped overnight by firm oil prices. Expectations that ongoing tensions in the Middle East and with Russia and Ukraine combined with supply constraints has forecasters predicting $100-125.00/barrel in the months ahead.

USDCAD support due to month-end demand for dollars will dissipate and leave prices vulnerable to a drop toward 1.2650, which suggests selling rallies near the 11:00 am fixing time.

Canada Raw Material (actual -2.9% vs forecast 0.6% m/m) and Industrial Product (actual 0.7% vs 0.8%/mm) price data were lower than expected.

Technical view: The intraday USDCAD technicals are bullish above 1.2710 looking for a move above resistance in the 1.2790-1.2800 area. A decisive break above 1.2810 puts 1.3000 in play whjile a move below 1.2710 risks further losses to 1.2630.

For today, USDCAD support is at 1.2710 and 1.2660. Resistance is at 1.2810 and 1.2850. Today’s Range 1.2720-1.2820

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The final trading day of January started with a fizzle in many Asian markets as the Lunar New Year festivities began. European markets fared better as stocks traded firmer ahead of this week’s ECB and BoE monetary policy meetings. S&P 500 futures flipped to negative in early NY trading.

The US called a meeting of the UN Security Council for today over Russia’s actions toward Ukraine. It is rather pointless as Russia can veto any statement and as of Tuesday, Russia assumes the presidency of the council.

EURUSD traded in a 1.1139-1.1193 range. Eurozone Q4 GDP was a tick lower than forecast but close enough to be a non-issue. Prices are weighed down by concerns the ECB will continue to be out of step with most of the G-10 central banks as it ignores inflation and leave rates unchanged. EURUSD technicals are bearish below 1.1190 looking for a break of 1.1100 to target 1.1000.

GBPUSD traded with a bit of a bid, rising from 1.3389 to 1.3447. Prime Minister Boris Johnson and his government continue to try and explain their actions for ignoring the strict Covid rules and measures imposed across the country. The long-waited Sue Gray report into the governments partying has been delivered to 10 Downing Street with copies placed in all washroom stalls. The Bank of England is widely expected to raise interest rates 0.25% on Thursday.

USDJPY traded sideways in a 115.23-115.58 range with prices underpinned by rising US Treasury yields with safe-haven demand for yen limiting gains.

AUDUSD rallied right from the start, climbing to 0.7057 from 0.6986 ahead of Tuesday’s RBA monetary policy meeting. The RBA is expected to leave rates unchanged, but policy may take a hawkish turn due to employment gains and rising inflation. NZDUSD rallied as well but lagged the AUDUSD move.

The Chicago PMI index is expected to dip to 61.7 from 63.1.

Chart of the Day: EURUSD daily

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

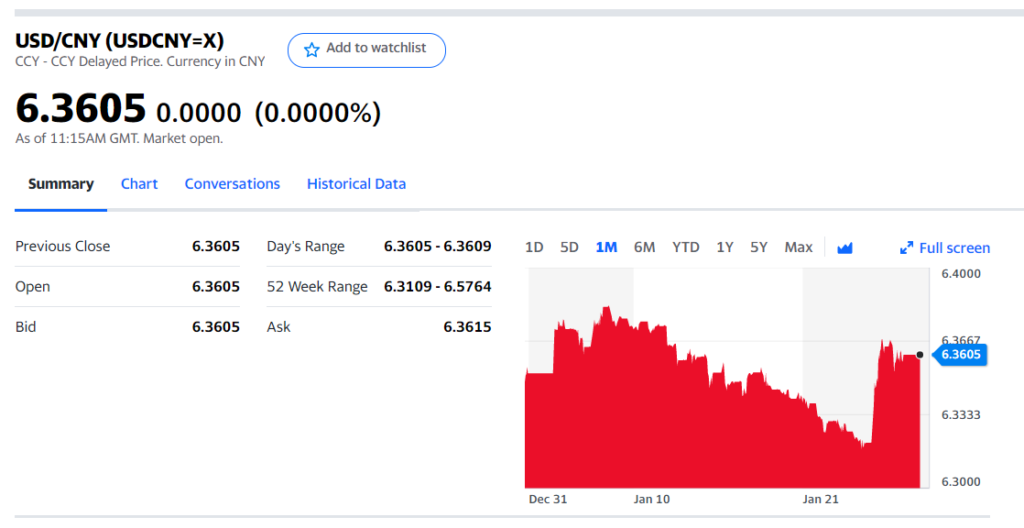

China Snapshot

Today’s Bank of China Fix 6.3746, previous 6.3746-Close

Shanghai Shenzhen CSI 300 closed

Chinese New Year-January 31 to February 15.

Caixin January Manufacturing PMI 49.1 (forecast 50.4, December 50.9)

Chart: USDCNY 1 month

Source: Yahoo Finance