Photo: pixabay

February 27, 2023

- US Durable Goods Orders slide 4.5% m/m in January (forecast -0.4%)

- Russia and China refuse to sign G-20 Finance Minister communique.

- US dollar opens well-above Friday’s level, but the rally paused overnight.

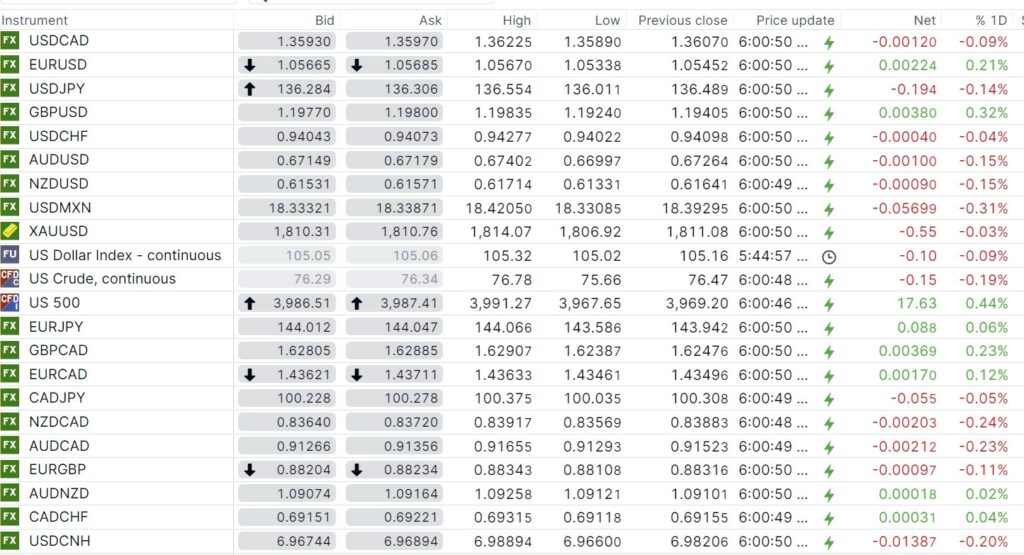

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3593-97, overnight range 1.3572-1.3623, close 1.3607

USDCAD jumped to 1.3660 in the wake of the higher-than-expected US PCE report on Friday, then spent the rest of the day and the overnight session drifting in a 1.3589-1.3622 band. The overnight low was breached following the weaker than expected US Durable Goods Orders data.

USDCAD drifted lower following the higher-than-expected Michigan Consumer Sentiment index which coincided with the S&P 500 index climbing from the day’s low.

WTI oil prices are rangebound, trading in a $75.66-$76.78 range overnight. Goldman Sachs is predicting that Opec will increase production by 1 million b/day in June, and despite that, Brent oil will rise to $100.00/b by year end.

Canada’s Q4 Current Account deficit widened to $10.64 billion from$ 9.4 billion previously.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3560 which is the bottom of the uptrend channel from February 14 and looking to break above the top of the channel and resistance from previous peaks in the 1.3680-1.3700 area. If successful, USDCAD would rally to 1.3850. A break below 1.3550 targets 1.3510, then 1.3440.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3620 and 1.3660.

Today’s range 1.3540-1.3620.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

US Durable Goods Orders fell 4.5% in January which was worse than expected. Traders sold US dollars and S&P 500 futures. The US 10-year yield dropped to 3.918% from 3.977% pre-data.

The G-20 Finance Ministers meeting in India ended with participants failing to issue a group communique. Russia and China refused to condemn Russia for invading Ukraine, resulting in India releasing the “Chair’s Summary.”

US National Security Adviser Jake Sullivan warned China against sending weapons to Russia saying, “I think it would alienate them from a number of countries in the world, including our European allies, and it would put them for square into the center of responsibility for the kinds of war crimes and bombardments of civilians and atrocities that the Russians are committing in Ukraine.”

Global markets continue to digest Friday’s 0.6% rise in US Core PCE in January which was hotter than expected as was the Michigan Consumer Sentiment Index (actual 67 vs January 66.5). Those results suggest higher US rates for longer.

Fed voting member Phillip Jefferson agrees. He said, “The ongoing imbalance between the supply and demand for labor, combined with the large share of labor costs in the services sector, suggests that high inflation may come down only slowly.”

EURUSD traded narrowly in a 1.0534-1.0574 range. Euro area Economic Sentiment, Industrial Confidence and Services sentiment were modestly weaker in February. Traders are more focused on Thursday inflation data.

GBPUSD climbed from 1.1924 in Asia to 1.2013 in NY. Sterling is underpinned by reports that the EU and UK are close to a new agreement on the Northern Ireland Protocol. The intraday GBPUSD technicals are bullish above 1.1940, looking for a break above 1.2000 to extend gains to 1.2050.

USDJPY consolidated Friday’s post-PCE gains and traded in a 136.01-136.55 range. Prices retreated to the overnight session low following the soft Durable Goods Orders data, and the subsequent drop in the US 10-year Treasury yield. The downside may be limited as Bank of Japan Governor nominee Kazuo Ueda is not as hawkish as once thought. He said it was appropriate to continue monetary easing.

AUDUSD consolidated Friday’s losses in a 0.6700-0.6740 range. Lower commodity prices and concerns that China’s post-pandemic economic rebound is less robust than expected are weighing on prices.

NZDUSD traded in a 0.6133-0.6174 range. Q4 Retail Sales fell 1.35% q/q compared to the forecast for a 1.7% gain. ASB Bank said soaring living costs and RBNZ rate hike warnings weighed on the data.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

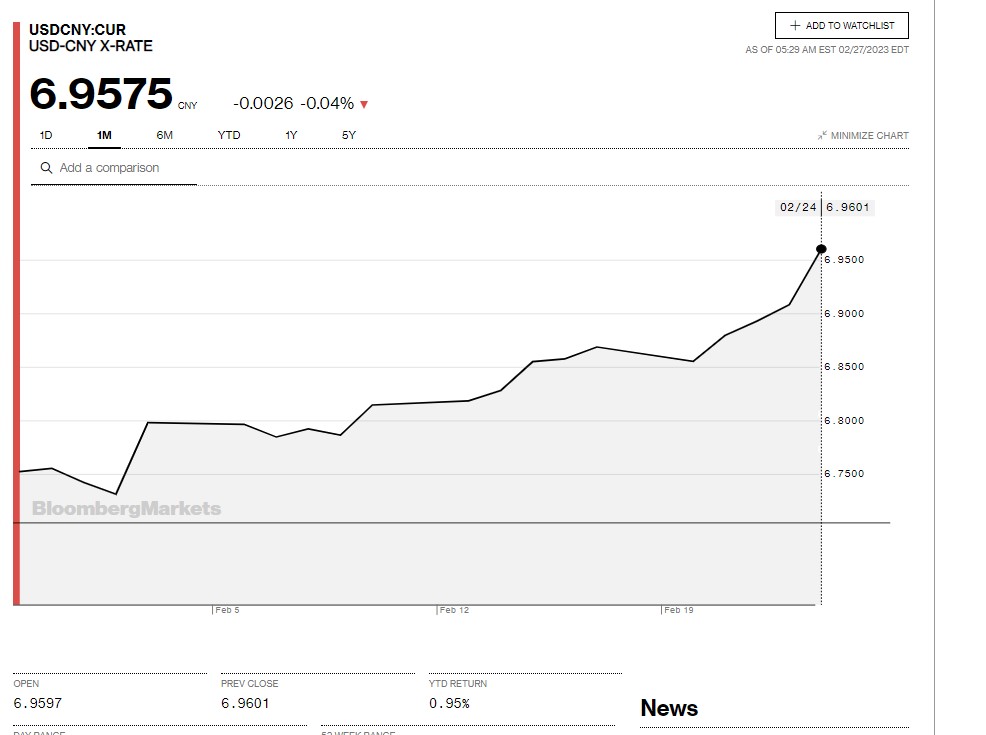

China Snapshot

Bank of China Fix: 6.9572, Previous: 6.8942

Shanghai Shenzhen CSI 300 fell 0.42% to 4043.84.

Chart: USDCNY 1 month

Source: Bloomberg